If you own a four-bedroom free standing home in Cameron Park, NSW 2285, you're probably wondering whether your building insurance premium is reasonable — or whether you're quietly paying too much. This article breaks down a real building-only insurance quote for a property in this suburb and benchmarks it against local, state, and national data so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question sits at $2,288 per year (or roughly $201 per month) for building-only cover on a four-bedroom, two-bathroom free standing home, with a building sum insured of $675,000 and a $5,000 excess.

Our price rating for this quote? Cheap — below average.

That's genuinely good news for the homeowner. Based on comparison data across Cameron Park, the suburb average premium sits at $4,012 per year, and the median is $3,769 per year. This quote comes in well beneath the suburb's 25th percentile of $2,665 — meaning it's cheaper than at least 75% of comparable quotes we've seen in the area. That's a strong result.

To put it plainly: if you're paying $2,288 a year for building cover in Cameron Park, you're doing significantly better than most of your neighbours.

---

How Cameron Park Compares

Understanding where Cameron Park sits in the broader insurance landscape helps put this quote in full context.

| Benchmark | Premium |

|---|---|

| This quote | $2,288/yr |

| Cameron Park suburb average | $4,012/yr |

| Cameron Park suburb median | $3,769/yr |

| Cameron Park 25th percentile | $2,665/yr |

| Newcastle LGA average | $3,835/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. The NSW state average of $9,528 is dramatically higher than what's being paid in Cameron Park — though it's worth noting that NSW averages are heavily skewed by high-risk and high-value properties in coastal, flood-prone, or bushfire-affected areas. The NSW median of $3,770 is a more useful comparison point, and this quote still comes in well below that figure.

Against the national median of $2,764, this quote is competitive — sitting about $476 below that benchmark. The national average of $5,347 is again skewed upward by extreme premiums in disaster-prone regions, so the median is the more meaningful figure for most homeowners.

Within the Newcastle LGA, the average is $3,835 — and this quote beats that comfortably. Cameron Park is a well-established, predominantly residential suburb in the Lake Macquarie area, and its risk profile appears to be reflected in relatively moderate insurance pricing compared to many other NSW postcodes.

---

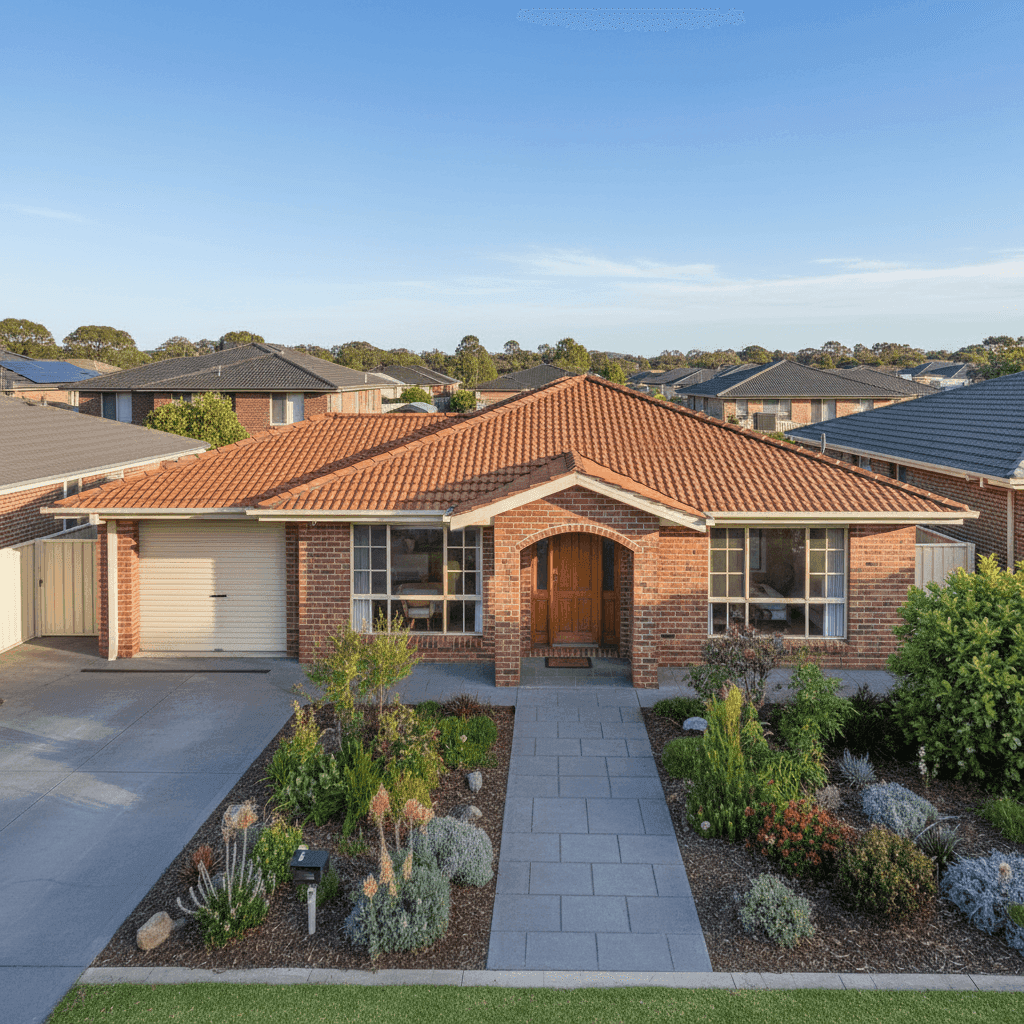

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour when it comes to insurance pricing.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to weatherboard or lightweight cladding, which can translate to lower premiums.

Tiled roofing is similarly well-regarded. Tiles are durable, fire-resistant, and less susceptible to storm damage than some alternative materials — all factors that reduce the likelihood of a claim.

Built in 2007, the property is relatively modern without being brand new. Homes of this vintage typically have compliant electrical wiring, plumbing, and structural standards, which reduces the risk of age-related defects that might otherwise push up a premium.

Stump foundations are worth noting. While stumps are common in certain parts of Australia, they can introduce some risk of movement or pest intrusion over time. However, in a well-maintained home, this is unlikely to significantly affect pricing.

Timber and laminate flooring is a neutral factor for most insurers in a building-only policy, since contents cover is not included here.

The absence of a pool, solar panels, and ducted climate control keeps the risk profile clean. Each of those features can add complexity (and cost) to a policy, so their absence here likely contributes to the competitive premium.

At 214 square metres, this is a comfortably sized family home, and the $675,000 sum insured reflects a reasonable rebuild cost for a property of this size and construction quality in the current market.

---

Tips for Homeowners in Cameron Park

Whether you're reviewing an existing policy or shopping for a new one, here are a few practical steps to make sure you're getting the best value.

1. Review your sum insured regularly. Building costs have risen significantly in recent years due to labour shortages and material price increases. Make sure your sum insured reflects current rebuild costs — not what it cost to build five or ten years ago. Underinsurance is one of the most common (and costly) mistakes homeowners make.

2. Consider your excess carefully. This quote carries a $5,000 building excess. A higher excess typically lowers your annual premium, but it also means you'll pay more out of pocket if you ever need to make a claim. Think about what you could comfortably afford in an emergency before locking in a high excess.

3. Don't auto-renew without comparing. Even if your current premium looks competitive, insurers regularly adjust their pricing. What's cheap today might not be cheap next year. Use a comparison tool like CoverClub at renewal time to make sure you're still getting a fair deal.

4. Check what's actually covered. Building-only cover protects the structure of your home but not your belongings. If you have significant contents — furniture, appliances, clothing, electronics — it's worth considering whether a combined building and contents policy makes more sense for your situation.

---

Compare Your Own Quote

Curious how your home insurance stacks up? CoverClub makes it easy to compare building and contents insurance quotes across Australia's leading insurers — all in one place. Whether you're in Cameron Park or anywhere else in NSW, you can get a quote in minutes and see exactly where your premium sits relative to your suburb, your state, and the national average. Don't pay more than you need to.