Aeroglen is a quiet residential suburb nestled just south of Cairns Airport in Far North Queensland — and like much of the region, home insurance here comes with its own set of considerations. This analysis looks at a real home and contents insurance quote for a 2-bedroom, 1-bathroom free standing home in Aeroglen (postcode 4870), breaking down whether the premium is fair, how it stacks up against state and national benchmarks, and what property features are driving the cost.

---

Is This Quote Fair?

The annual premium for this property came in at $6,933 per year (or $664/month), covering a building sum insured of $448,000 and contents valued at $50,000, each with a $1,000 excess.

Our pricing model rates this quote as CHEAP — below average for the area. That's a meaningful result, particularly given that Aeroglen sits within the Cairns local government area, which is one of the more expensive insurance markets in Queensland due to its tropical climate and cyclone exposure.

To put it plainly: if you've received this quote, you're doing better than most of your neighbours. That said, "cheap" is relative — $6,933 a year is still a significant household expense, and it's always worth understanding why you're paying what you're paying.

---

How Aeroglen Compares

There's no suburb-level pricing data available specifically for Aeroglen, but we can draw meaningful comparisons using Queensland state data and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| LGA (Cairns) | $12,404/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| This Quote | $6,933/yr | — |

A few things stand out here:

- This quote is 44% below the Cairns LGA average of $12,404/yr — a substantial saving in one of Queensland's priciest insurance markets.

- It sits 24% below the Queensland state average of $9,129/yr.

- It is, however, 29% above the national average of $5,347/yr — a reminder that Far North Queensland carries genuine risk premiums compared to much of Australia.

- Compared to the national median of $2,764/yr, this quote is more than double — but that's to be expected for a cyclone-prone region with elevated rebuilding costs.

The gap between the QLD median ($3,903) and this quote ($6,933) is also worth noting. The median can be skewed by lower-value properties or those with minimal contents cover, so a well-insured property in a high-risk zone will naturally sit above it.

For more localised data as it becomes available, keep an eye on the Aeroglen suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium — some pushing it up, others potentially keeping it in check.

🌀 Cyclone Risk Area

This is the single biggest factor. Aeroglen falls within a designated cyclone risk zone, which significantly increases the likelihood of storm and wind damage claims. Insurers price this risk heavily, and it's the primary reason Cairns-area premiums are so much higher than the national average.

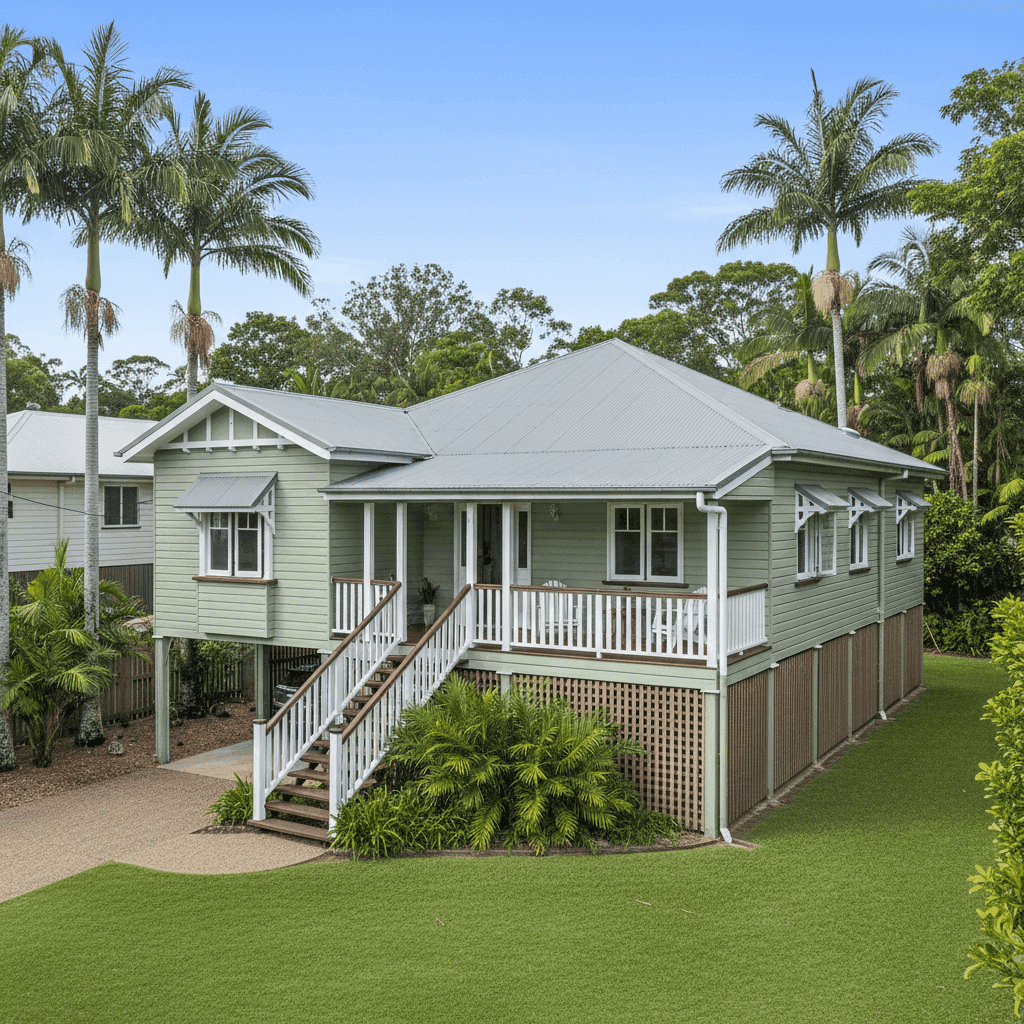

🏠 Elevated Construction (Poles/Stumps)

The home is elevated by at least 1 metre on a pole or stump foundation — a classic Queenslander design feature. This is actually a positive for flood resilience, as it reduces the risk of inundation during heavy rainfall events. However, elevated homes can also be more vulnerable to wind uplift during cyclones, which insurers factor into their assessments.

🪵 Weatherboard Timber Walls

Weatherboard wood is a common external wall material in older Queensland homes, but it carries a higher fire and storm damage risk compared to brick or concrete. Timber homes can also be more costly to repair or replace, which influences the building sum insured and the premium accordingly.

🏗️ Construction Year: 1950

At over 70 years old, this home predates modern building codes — including those introduced after Cyclone Tracy in 1974 and subsequent updates to cyclone-resistant construction standards. Older homes are generally considered higher risk by insurers, as they may lack the structural reinforcements required of newer builds.

🔩 Steel/Colorbond Roof

On the positive side, a steel Colorbond roof is considered relatively durable and performs well in high-wind conditions compared to older corrugated iron or tiled roofs. This may help moderate the premium slightly.

📐 Building Size: 105 sqm

At 105 square metres, this is a modest-sized home. A smaller footprint generally means a lower replacement cost, which can help keep the building sum insured — and therefore the premium — more manageable.

🛋️ Standard Fittings, No Pool or Solar

Standard-quality fittings, no swimming pool, and no solar panels all contribute to a more straightforward risk profile. High-end fixtures, pools, and solar systems each add complexity and cost to a claim, so their absence is a mild premium-moderating factor.

---

Tips for Homeowners in Aeroglen

1. Review Your Building Sum Insured Annually

Construction costs in Far North Queensland have risen sharply in recent years. Make sure your $448,000 building sum insured still reflects what it would actually cost to rebuild your home — not just its market value. Underinsurance is a common and costly mistake, especially after a major weather event when builders are in high demand.

2. Harden Your Home Against Cyclones

Many insurers offer discounts or more competitive premiums for homes that have been cyclone-rated or retrofitted with storm-resistant features. Consider a cyclone inspection, installing cyclone shutters, or reinforcing roof connections. The Queensland Government's Resilient Homes Fund may also offer assistance for eligible properties.

3. Understand Your Excess Before You Claim

Both the building and contents excess on this policy sit at $1,000. In cyclone-prone areas, some policies include a separate, higher cyclone excess — make sure you read the Product Disclosure Statement (PDS) carefully so there are no surprises at claim time.

4. Compare Quotes Every Year

Even if you're happy with your current premium, the insurance market shifts constantly. Insurers reprice risk regularly, and a policy that was competitive last year may not be the best option today. Use a comparison tool like CoverClub to check what else is available without the legwork of contacting multiple insurers individually.

---

Find a Better Deal with CoverClub

Whether you're a long-time Aeroglen local or new to the area, comparing home and contents insurance quotes is one of the smartest financial moves you can make. Premiums in the Cairns region can vary enormously between insurers — sometimes by thousands of dollars for equivalent cover. Get a quote through CoverClub to see how your current policy stacks up and whether there's a better deal waiting for you.