If you own a free standing home in Aeroglen, QLD 4870, you already know that insuring a property in Cairns' northern suburbs comes with its own set of challenges. From tropical weather events to the ever-present threat of cyclones, home insurance in this part of Queensland is a serious financial consideration. This article breaks down a real building-only insurance quote for a 3-bedroom, 1-bathroom weatherboard home in Aeroglen — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question sits at $23,012 per year (or $2,205/month) for building-only cover on a property insured for $450,000, with a building excess of $5,000. Our price rating for this quote is EXPENSIVE — above average when benchmarked against comparable properties.

To put that in perspective:

- The QLD state average premium is $9,129/yr, and the median is $3,903/yr

- The national average is $5,347/yr, with a national median of $2,764/yr

- The Cairns LGA average is $12,404/yr

This quote is roughly 2.5× the Cairns LGA average and more than 4× the Queensland state median. Even accounting for the elevated risk profile of this particular property, that's a significant premium — and one worth scrutinising before accepting.

That said, "expensive" doesn't necessarily mean "wrong." Several features of this home push it firmly into a higher-risk bracket, and insurers price accordingly. The key question is whether you're getting the right cover at the most competitive rate available — and that's where comparison becomes essential.

---

How Aeroglen Compares

While there isn't enough suburb-level data to give a precise Aeroglen-specific average, we can contextualise this quote against broader benchmarks.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $23,012 |

| Cairns LGA Average | $12,404 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

Aeroglen sits within the Cairns LGA, which already commands one of the highest average premiums in Queensland — itself well above the national average. The region's exposure to tropical cyclones, heavy rainfall, and flooding means insurers load premiums significantly compared to southern states.

Even within Cairns, however, this quote is notably above the LGA average. That gap is largely explained by the specific characteristics of the property itself, which we'll unpack below.

---

Property Features That Affect Your Premium

Several attributes of this home are working together to push the premium higher. Understanding them can help you have a more informed conversation with insurers.

Cyclone Risk Area

This is the single biggest driver. Aeroglen falls within a designated cyclone risk zone, and insurers apply substantial loadings to properties in Far North Queensland. Structural damage from cyclonic winds is one of the most costly claims categories in Australia, and premiums in these areas reflect that exposure.

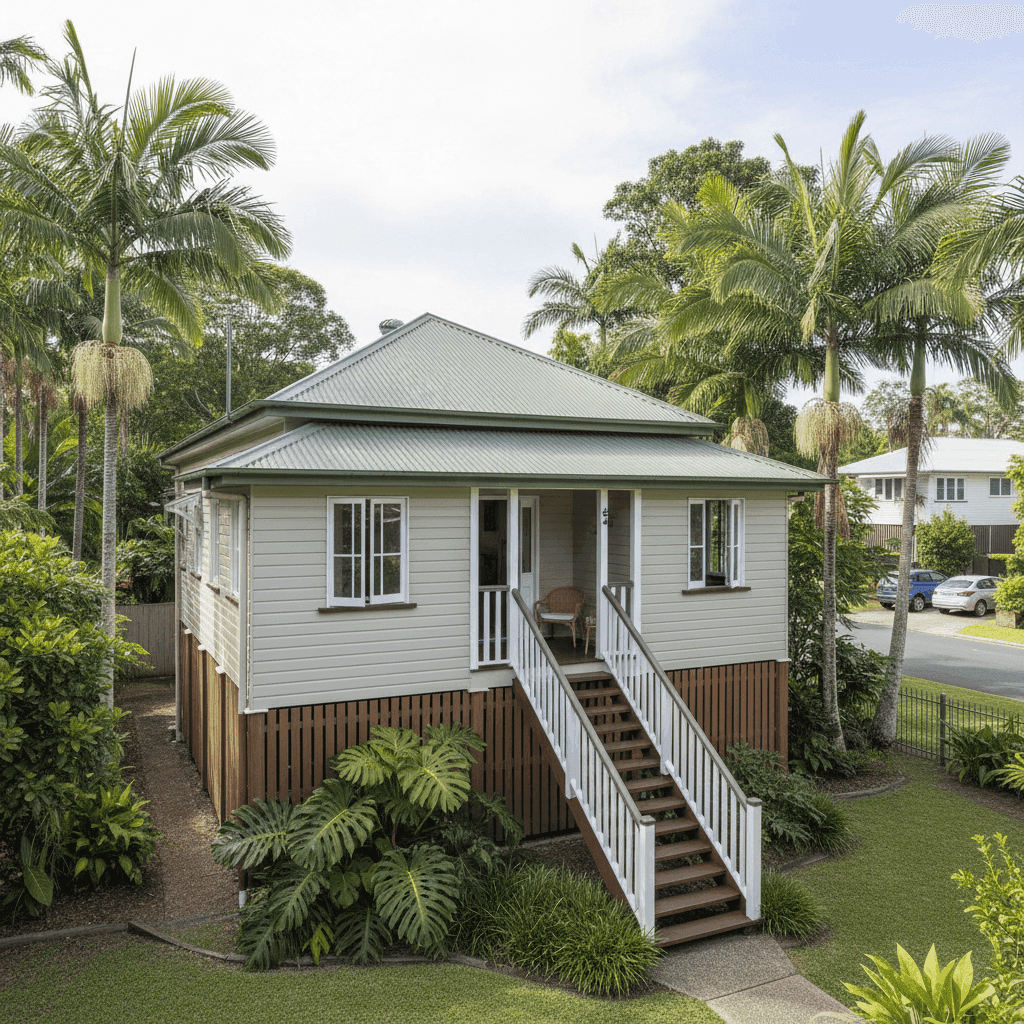

Weatherboard Timber Walls

Weatherboard wood construction is considered higher risk than brick or rendered masonry. Timber is more vulnerable to wind damage, moisture ingress, and termite activity — all of which are elevated concerns in a tropical climate like Cairns. Many insurers apply a loading for non-masonry external walls.

Elevated on Stumps

The home is elevated by at least 1 metre on stumps — a classic Queenslander design. While elevation can actually reduce flood risk in some scenarios, stump foundations introduce their own considerations: subfloor maintenance, stump deterioration, and the structural dynamics of an elevated building during high-wind events. Insurers assess this carefully in cyclone-prone areas.

Steel/Colorbond Roof

A Colorbond steel roof is generally viewed positively by insurers — it's durable, fire-resistant, and performs reasonably well in wind events compared to tiled roofs. This feature may be moderating the premium slightly, even if other factors are pushing it up.

Construction Year: 1975

At approximately 50 years old, this home predates modern building codes introduced after Cyclone Tracy (1974) and subsequent updates. Older homes in Far North Queensland are scrutinised more carefully by underwriters, as they may not meet current cyclone-resilience standards without documented upgrades.

Timber/Laminate Flooring & Ducted Climate Control

Ducted air conditioning adds to the sum insured and replacement cost, as it's an expensive system to repair or replace. Timber and laminate flooring also carries a higher replacement cost than concrete slab, contributing to the $450,000 building sum insured.

---

Tips for Homeowners in Aeroglen

1. Review Your Sum Insured Carefully

At $450,000 for a 130 sqm home, the building sum insured works out to roughly $3,460/sqm — on the higher end for standard construction. It's worth using an independent building cost calculator to verify this figure. Being over-insured costs you in premiums; being under-insured can cost you far more at claim time.

2. Consider a Higher Excess to Reduce Your Premium

This policy carries a $5,000 building excess. Some insurers offer further premium reductions if you opt for an even higher voluntary excess. If you have the financial buffer to absorb a larger out-of-pocket cost in a claim, this can be a meaningful way to reduce your annual outlay.

3. Document Cyclone-Resilience Upgrades

If the property has had roof strapping, tie-downs, or other structural reinforcements added since construction, document these thoroughly. Some insurers will reduce premiums for homes that demonstrably exceed the minimum standards for cyclone resistance. Ask your insurer directly whether any improvements qualify for a discount.

4. Compare Quotes Every Year

The insurance market in North Queensland is competitive — but only if you engage with it. Loyalty rarely pays in insurance, and the gap between the best and worst quotes for a property like this can be thousands of dollars annually. Use a comparison platform like CoverClub to benchmark your renewal offer before you accept it.

---

Get a Better Deal on Your Home Insurance

A premium of over $23,000 a year is a significant household expense — and it's not something you should accept without shopping around. Whether you're renewing an existing policy or insuring a new purchase, comparing quotes from multiple insurers is the single most effective thing you can do to manage your costs.

Start comparing home insurance quotes at CoverClub — it's free, fast, and could save you thousands.