Albion Park, nestled in the Illawarra region of New South Wales, is a well-established suburb that blends suburban comfort with coastal proximity. For owners of a free standing home here, understanding what drives your home insurance premium — and whether you're paying a fair price — can make a meaningful difference to your household budget. This article breaks down a real home and contents insurance quote for a four-bedroom property in Albion Park (postcode 2527) and puts the numbers in context.

---

Is This Quote Fair?

The quote in question comes in at $3,282 per year (or $315 per month) for combined home and contents cover, with a building sum insured of $950,000 and contents valued at $50,000. Both the building and contents excesses are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

According to suburb-level data for Albion Park (2527), the average annual premium in this postcode sits at $1,690, with a median of $1,636. That means this quote is nearly double the local average. Even at the 75th percentile — meaning 75% of quotes in the area are cheaper — the benchmark is just $2,172 per year. This quote clears that mark by over $1,100.

That said, context matters. Several property-specific factors (explored below) can legitimately push a premium above the suburb norm, and a higher building sum insured of $950,000 is a significant driver here.

---

How Albion Park Compares

To put this quote in broader perspective, here's how Albion Park stacks up against NSW and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Albion Park (2527) | $1,690/yr | $1,636/yr |

| LGA (Kiama) | $3,332/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW average premium is extraordinarily high at $9,528 — this is heavily skewed by high-risk and high-value properties across the state, so the median of $3,770 is a more reliable reference point. Against that median, this quote of $3,282 is actually slightly below the NSW midpoint, which reframes the picture somewhat.

At the LGA level, the Kiama local government area (which includes Albion Park) has an average premium of $3,332 — very close to this quote. So while the property owner is paying well above the suburb average, they're broadly in line with what others across the wider LGA are paying.

Nationally, the median sits at $2,764, making this quote about 19% above the national midpoint — elevated, but not dramatically so given the property's characteristics.

---

Property Features That Affect Your Premium

Several features of this property have a direct bearing on what insurers charge:

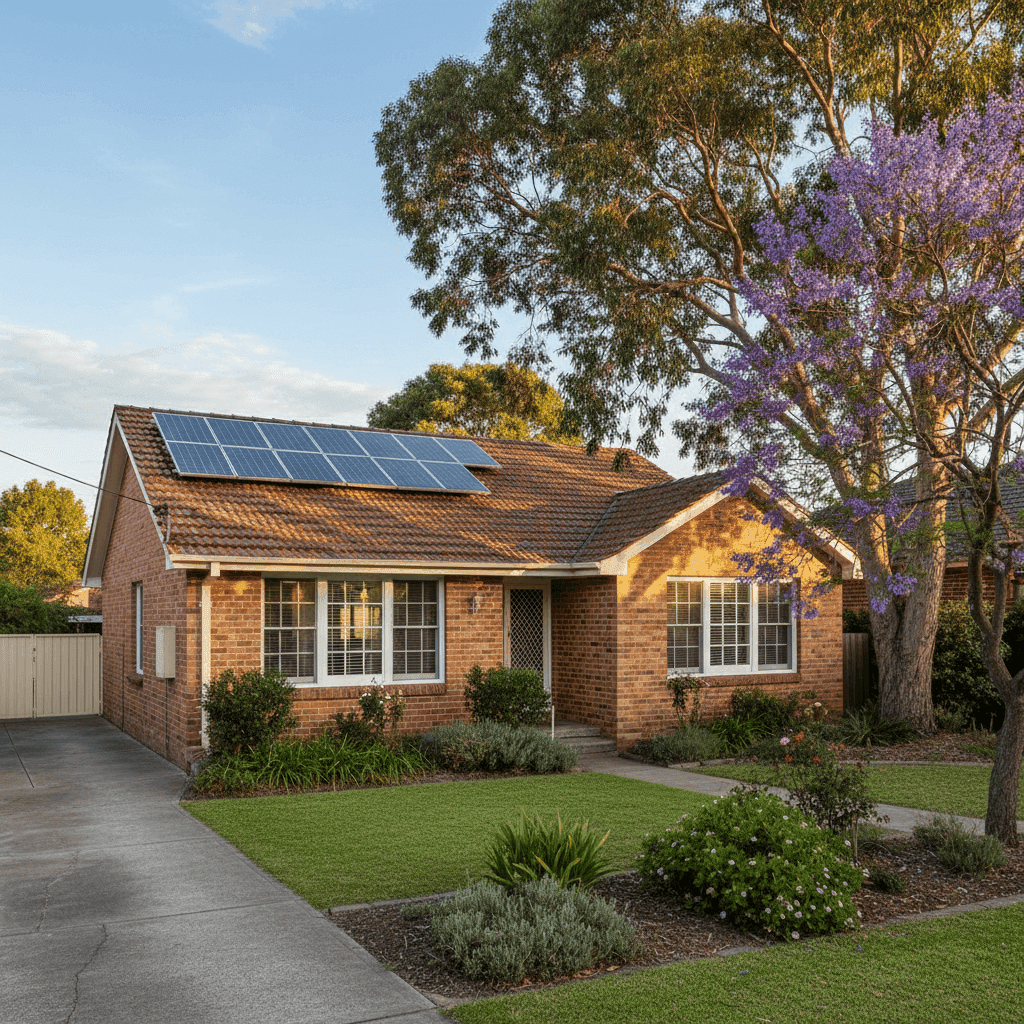

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire, wind, and structural stress, which can help moderate premiums compared to timber-framed or clad homes. This is a genuine plus for this property.

Tiled Roof Terracotta or concrete tiles are considered durable and low-risk by most insurers. They hold up well in storms and don't carry the fire risk associated with some other materials. Another tick in the right column.

Stump Foundation Homes on stumps (also known as pier or post foundations) can be more susceptible to certain types of damage — including subsidence and pest-related issues — compared to slab foundations. Insurers may price this in, particularly for older properties. Built in 1998, this home is now over 25 years old, which can also nudge premiums upward as ageing materials and systems become more relevant.

Solar Panels Solar panels are an increasingly common feature but they do add to the replacement cost of a home. If the building sum insured accounts for their reinstallation value, this contributes to the higher coverage amount — and therefore a higher premium.

Ducted Climate Control Ducted air conditioning systems are expensive to replace and add to the overall rebuild cost. At 235 sqm with above-average fittings quality, this is a well-appointed home, and insurers will factor the cost of reinstating quality fixtures into the premium.

Above-Average Fittings Quality This is arguably one of the more significant premium drivers. Above-average fittings — think stone benchtops, quality cabinetry, premium flooring and fixtures — substantially increase the cost to rebuild or repair, and insurers price accordingly.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common liability risk factor. Albion Park is also not classified as a cyclone risk area, which keeps wind-event pricing more moderate than you'd see in parts of Queensland or northern WA.

---

Tips for Homeowners in Albion Park

1. Review Your Building Sum Insured At $950,000, the building sum insured is substantial. It's worth getting an independent building replacement cost estimate (not market value) to confirm this figure is accurate — neither over- nor under-insured. Tools like a quantity surveyor report or an online calculator can help. Over-insuring means paying more premium than necessary.

2. Compare Multiple Quotes The suburb data is based on 39 quotes, which shows real variation in what insurers charge for similar properties. Premiums for the same home can differ by thousands of dollars between providers. Getting a fresh quote through CoverClub takes minutes and can surface significantly cheaper options.

3. Consider Your Excess Level Both excesses here are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, this is often a smart trade-off.

4. Bundle and Ask About Discounts Many insurers offer discounts for bundling home and contents cover (already done here), as well as loyalty discounts, security system discounts, or incentives for paying annually rather than monthly. It's always worth asking — or switching to a provider with better base pricing.

---

Ready to Find a Better Deal?

If you're a homeowner in Albion Park or anywhere else in NSW, it pays to shop around. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly what you're getting for your money. Start your comparison at CoverClub and find out whether your current policy is still the best fit for your home.