If you own a free standing home in Albion Park Rail, NSW 2527, you already know this part of the Illawarra region offers a relaxed lifestyle — but what does it cost to properly protect your property? This article breaks down a real home and contents insurance quote for a six-bedroom, three-bathroom home in the suburb, compares it against local and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $5,547 per year (or $525 per month) for combined home and contents insurance, covering a building sum insured of $1,210,000 and contents valued at $270,000. Both the building and contents excess are set at $500.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in perspective: the suburb average premium in Albion Park Rail sits at just $2,290 per year, and the median is even lower at $1,752. This quote is more than double the suburb median, which is a significant gap worth understanding before simply accepting the price.

That said, context matters. This is a large property — 389 square metres with six bedrooms — and the building sum insured of $1.21 million reflects a substantial replacement cost. Larger, higher-value homes naturally attract higher premiums, and a direct comparison with the suburb average (which likely includes a wide range of smaller properties) may not be entirely apples-to-apples.

---

How Albion Park Rail Compares

Here's how this quote stacks up across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,547 |

| Suburb Average (Albion Park Rail) | $2,290 |

| Suburb Median | $1,752 |

| Suburb 25th Percentile | $1,134 |

| Suburb 75th Percentile | $3,123 |

| LGA Average (Kiama) | $3,332 |

| NSW Average | $9,528 |

| NSW Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. While the quote is well above the Albion Park Rail suburb average and even the 75th percentile of $3,123, it sits remarkably close to the national average of $5,347 — just $200 above it. And compared to the NSW state average of $9,528, this quote is actually quite reasonable.

The Kiama LGA average of $3,332 also provides useful local context — this quote runs about 66% above the LGA average, again reflecting the size and value of the property rather than any obvious pricing anomaly.

The suburb sample size of 29 quotes is relatively modest, which means the local averages may not fully capture the range of larger or higher-value homes in the area. Homeowners with comparable properties should weigh the suburb data accordingly.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated:

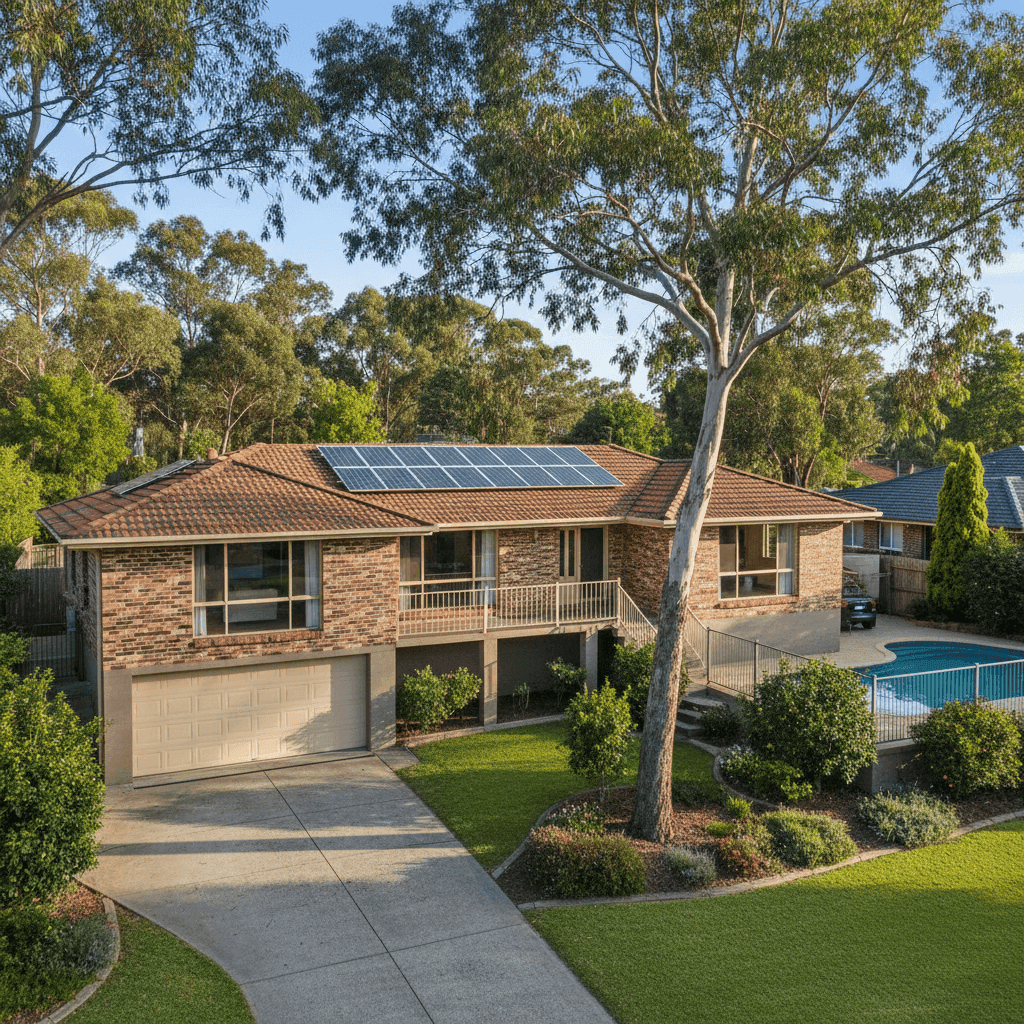

Size and sum insured: At 389 square metres with six bedrooms and three bathrooms, this is a large home by any measure. The $1.21 million building sum insured is substantial, and insurers price premiums proportionally to the replacement cost they're underwriting.

Brick veneer construction with tiled roof: Brick veneer walls and a tiled roof are generally viewed favourably by insurers. Both materials offer solid fire resistance and durability compared to alternatives like weatherboard or metal roofing. This construction profile typically contributes to more competitive premiums.

Stump foundation and timber/laminate flooring: The property sits on stumps and is elevated by less than one metre. While this style of construction is common in older NSW homes (built in 1990 in this case), it can introduce some additional risk considerations around subfloor moisture and storm damage. Timber and laminate flooring can also be more susceptible to water damage than concrete slab alternatives.

Swimming pool: A pool adds to the replacement cost of the property and introduces additional liability considerations, both of which can nudge premiums upward.

Solar panels: Solar panels are an increasingly common feature on Australian homes, but they do add to the insured value of the building. Ensuring your sum insured accounts for the replacement cost of your solar system is important — and it's a factor insurers price into the premium.

Ducted climate control: Ducted air conditioning systems are a high-value fixture that contributes to the overall building replacement cost. Like solar, it's an asset worth confirming is adequately covered under your policy.

No cyclone risk: Albion Park Rail is not classified as a cyclone risk area, which removes one of the more significant premium loading factors that affect properties in northern Queensland and parts of WA. This is a meaningful advantage for homeowners in this region.

---

Tips for Homeowners in Albion Park Rail

1. Review your sum insured carefully A building sum insured of $1.21 million is significant. Make sure this figure accurately reflects the cost to rebuild your home from scratch — not its market value. Underinsuring can leave you badly exposed after a major claim, while overinsuring means you're paying for cover you'll never use. Tools like the Cordell Sum Sure calculator can help you estimate an accurate rebuild cost.

2. Shop around — the market varies widely With suburb premiums ranging from $1,134 at the 25th percentile to $3,123 at the 75th percentile, there's clearly significant variation in what insurers will charge for similar properties in Albion Park Rail. Getting multiple quotes is one of the most effective ways to find better value. Compare quotes at CoverClub to see what's available for your specific property.

3. Consider your excess level Both the building and contents excess on this policy are set at $500. Opting for a higher voluntary excess — say, $1,000 or $2,000 — can meaningfully reduce your annual premium. If you're unlikely to make small claims, this trade-off often makes financial sense.

4. Confirm your contents value is accurate $270,000 in contents cover is a reasonable figure for a six-bedroom home, but it's worth doing a room-by-room audit periodically. Electronics, furniture, appliances, clothing, and valuables all add up quickly — and many homeowners find they're either over- or under-estimating the true replacement cost of their belongings.

---

Ready to Find a Better Rate?

Whether this quote looks right for your situation or you suspect you could be paying less, the best next step is to compare. CoverClub makes it easy to benchmark your premium against real quotes from across the market — so you can make a confident, informed decision about your home insurance.

Get a home insurance quote for your Albion Park Rail property →

You can also explore detailed premium data for your area on the Albion Park Rail suburb stats page or browse NSW home insurance statistics for broader context.