Homeowners in Alice River, QLD 4817 know that insuring a property in regional Queensland comes with its own set of considerations — not least the area's exposure to cyclone risk. This article takes a close look at a real building insurance quote for a four-bedroom, two-bathroom free-standing home in Alice River, breaking down whether the premium represents good value and what factors are likely driving the cost.

---

Is This Quote Fair?

The quote in question is $3,221 per year (or approximately $309 per month) for building-only cover on a free-standing home with a sum insured of $635,000 and a building excess of $2,000.

Our price rating for this quote is FAIR — Around Average, which is actually a solid outcome for a property in this part of Queensland.

To put that in context:

- The suburb median for Alice River is $4,615/yr, meaning this quote sits comfortably below the midpoint of what locals are typically paying.

- It also falls between the 25th percentile ($3,126/yr) and the 50th percentile ($4,615/yr) — placing it in the lower half of the local price range.

- The suburb average is a steep $11,332/yr, which is heavily skewed by high-end outlier quotes in the area. The median is a far more reliable benchmark here.

In short, at $3,221/yr, this homeowner is paying less than most of their neighbours for comparable cover — a genuinely competitive result given the risk profile of the region.

---

How Alice River Compares

Understanding where Alice River sits within the broader insurance landscape helps put this quote in sharper perspective. You can explore the full local data on the Alice River suburb stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $3,221/yr |

| Alice River Median | $4,615/yr |

| Alice River Average | $11,332/yr |

| LGA (Charters Towers) Average | $4,457/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

A few things stand out here. First, both the suburb and state averages are dramatically higher than their respective medians — a telltale sign that a small number of very expensive quotes are pulling the averages up. This is common in cyclone-prone regions of Queensland, where some properties attract eye-watering premiums.

Second, this quote is only marginally above the national median of $2,764/yr, which is remarkable for a home in a cyclone risk area. Nationally, premiums are much lower on average because the bulk of Australian homes sit in lower-risk metropolitan areas. For a regional Queensland property to come in close to the national median is a strong result.

For broader Queensland and national comparisons, visit the QLD insurance stats page or the national home insurance stats page.

Note: This analysis is based on a sample of 13 quotes for the Alice River suburb, so while directionally useful, the data should be interpreted with that sample size in mind.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens.

Cyclone Risk Area

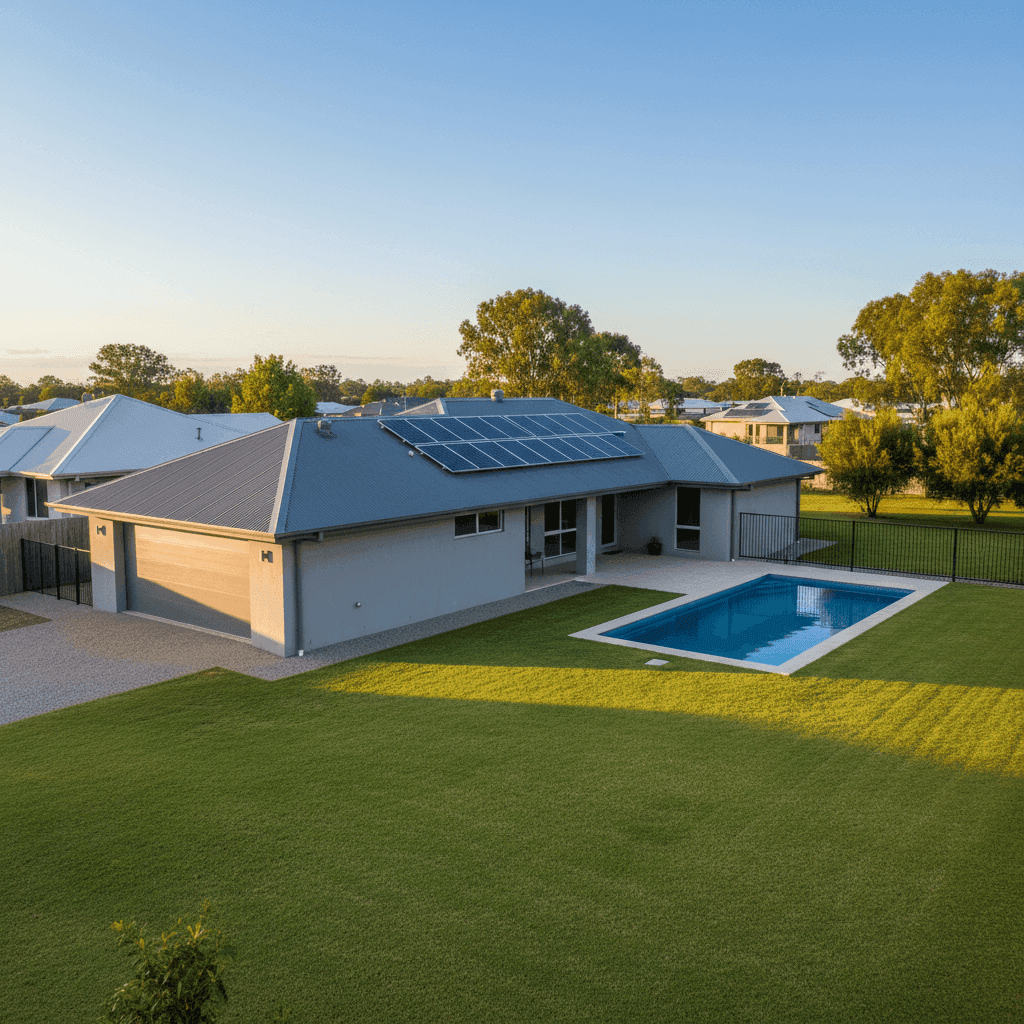

This is the single biggest factor. Alice River falls within a designated cyclone risk zone, which significantly elevates building insurance premiums across the board. Insurers price in the potential for wind, rain, and storm surge damage, and many policies in this region include a separate cyclone excess. The fact that this quote is still relatively competitive is partly a reflection of the property's resilient construction.

Concrete Walls & Colorbond Roof

A home built with concrete external walls and a steel/Colorbond roof is considered highly resilient to cyclone and storm damage. These materials are far more resistant to wind uplift and impact than timber-framed or fibrous cement alternatives, and insurers typically reward this with lower premiums. This construction combination is one of the most likely reasons this quote sits below the suburb median.

Slab Foundation & Tile Flooring

A concrete slab foundation is standard and well-regarded in Queensland's climate — it offers stability and reduces the risk of subsidence or termite-related structural damage. Tile flooring is similarly practical in tropical and sub-tropical regions, being resistant to moisture and humidity damage.

Swimming Pool

A pool adds a modest amount to the insured value of the property and can introduce some liability considerations, though for building-only cover its impact is primarily on the sum insured rather than the risk profile.

Solar Panels

Rooftop solar panels are an increasingly common feature in Queensland homes and are typically covered under building insurance. They do add to the replacement cost of the property, which is reflected in the sum insured. Homeowners should ensure their policy explicitly covers solar panels and that the sum insured accounts for their full replacement value.

2000 Build Year & Standard Fittings

A home built in 2000 is relatively modern — old enough that some wear is expected, but well within the era of contemporary building codes. Standard fittings keep the replacement cost predictable and avoid the premium loading that can come with high-end or bespoke fixtures.

---

Tips for Homeowners in Alice River

1. Review Your Sum Insured Regularly

Building costs in regional Queensland have risen sharply in recent years. A sum insured of $635,000 for a 244 sqm concrete home is substantial, but it's worth cross-checking against current construction cost estimates annually to ensure you're neither underinsured nor paying for more cover than you need.

2. Understand Your Cyclone Excess

Many policies in cyclone-prone areas apply a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured. Make sure you know what your cyclone excess is before a storm season arrives, so there are no surprises at claim time.

3. Keep Documentation of Your Solar Panels and Pool

Insurers will want evidence of the value of your solar system and pool equipment in the event of a claim. Keep receipts, installation records, and photos updated. Confirm with your insurer that both are explicitly listed under your building cover.

4. Compare Quotes Before Renewal

Even a "fair" quote can be beaten. The wide spread between the 25th percentile ($3,126/yr) and 75th percentile ($7,941/yr) in Alice River shows that premiums vary enormously for similar properties. Shopping around at renewal time — rather than auto-renewing — can save hundreds of dollars per year.

---

Compare Home Insurance Quotes for Alice River

Whether you're reviewing an existing policy or insuring a property for the first time, comparing quotes is the smartest way to make sure you're getting the right cover at the right price. Get a home insurance quote at CoverClub and see how your premium stacks up against the local market in seconds.