If you own a free standing home in Alpha, QLD 4724, you've probably noticed that home insurance doesn't come cheap in regional Queensland. This article breaks down a real home and contents insurance quote for a 2-bedroom, 2-bathroom property in Alpha — and puts it under the microscope against suburb, state, and national benchmarks to help you understand whether you're paying a fair price.

---

Is This Quote Fair?

The quote in question comes in at $20,838 per year (or $1,997/month), covering both building (sum insured: $400,000) and contents ($75,000). The building excess is $1,000 and the contents excess is $500.

Our price rating for this quote is EXPENSIVE — Above Average.

To put that into perspective, the suburb average for Alpha (QLD 4724) sits at $10,342 per year, with a median of $10,559. This quote is almost double the local average — a significant gap that warrants a closer look.

Even when you account for the upper end of the suburb range (the 75th percentile sits at $11,743/yr), this quote still exceeds that benchmark by more than $9,000 annually. That's not a small difference — it's the kind of gap that makes shopping around not just worthwhile, but essential.

---

How Alpha Compares to the Rest of Australia

Alpha doesn't exist in a vacuum, and understanding the broader pricing landscape helps contextualise just how much regional Queensland homeowners can pay for coverage.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $20,838 |

| Alpha Suburb Average | $10,342 |

| Alpha Suburb Median | $10,559 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Isaac LGA Average | $3,567 |

(Based on a sample of 14 quotes in the Alpha suburb.)

A few things stand out here. First, even the suburb average in Alpha ($10,342) is well above both the QLD state average ($9,129) and the national average ($5,347). This tells us that Alpha is already a more expensive area to insure — likely due to a combination of remoteness, age of housing stock, and the specific risk profile of the region.

Second, the gap between the QLD state average ($9,129) and the state median ($3,903) is enormous. This suggests that a relatively small number of high-cost properties — like this one — are pulling the average upward significantly. The same pattern appears nationally.

The Isaac LGA average of just $3,567 is particularly striking. It implies that while some properties in the broader Isaac region attract very affordable premiums, others — particularly those with older construction, specific materials, or higher sum insured values — can cost many times more to insure.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its elevated premium. Here's what insurers are paying close attention to:

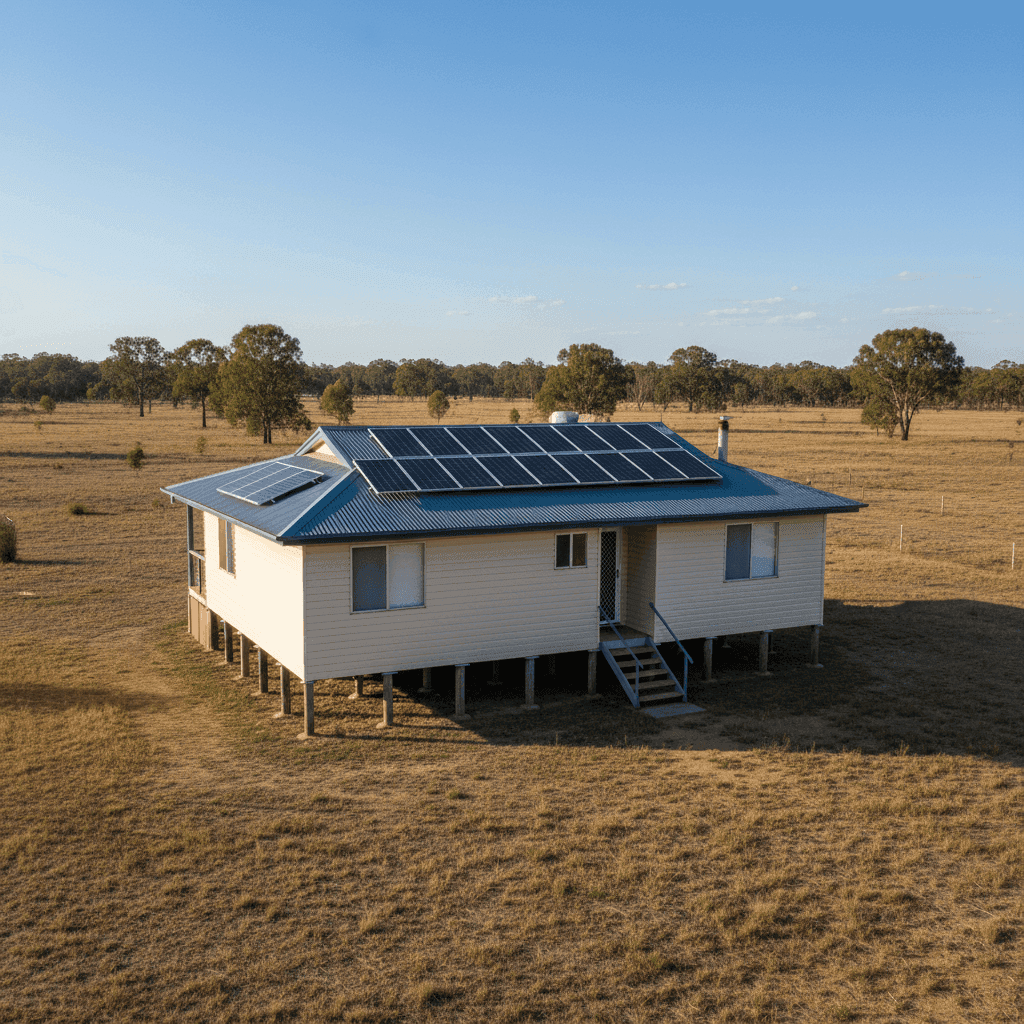

Age of Construction (1949)

At over 75 years old, this home was built well before modern building codes were established. Older homes can present higher risk for insurers due to ageing electrical wiring, plumbing, and structural components that may be more susceptible to damage or failure.

Vinyl Cladding External Walls

Vinyl cladding is generally considered a moderate-risk material. While it's durable and low-maintenance, it can be more vulnerable to impact damage and extreme heat compared to brick or fibre cement. Some insurers price this material at a slight premium.

Stumped Foundation

Homes on stumps (also known as timber or concrete pier foundations) are common in regional Queensland, particularly in older properties. While this style offers good airflow and flood resilience in some scenarios, stumped homes can be more susceptible to movement, subsidence, and termite activity — all factors that can influence premiums.

Solar Panels

The presence of solar panels adds replacement value to the property. If damaged in a storm or hailstorm, panels can be costly to repair or replace, and insurers factor this into their risk calculations.

Ducted Climate Control

Ducted air conditioning systems represent a significant capital investment and add to the overall replacement cost of the home. This can push the sum insured higher and, in turn, lift the premium.

High Sum Insured ($400,000)

For a 130 sqm home, a $400,000 building sum insured is on the higher end. It's worth verifying this figure with a quantity surveyor or using an online building cost calculator to ensure you're not over-insured — paying for more coverage than you'd actually need to rebuild.

---

Tips for Homeowners in Alpha

Whether you're reviewing an existing policy or shopping for the first time, here are some practical steps to help manage your insurance costs in Alpha.

1. Review your sum insured carefully. Over-insurance is a common and costly mistake. Use a professional rebuild cost estimator to confirm whether $400,000 accurately reflects the cost to rebuild your home from scratch — not its market value. Even a modest reduction in sum insured can meaningfully lower your annual premium.

2. Compare multiple quotes. With only 14 quotes in our Alpha suburb sample, the market here is relatively thin. That makes it even more important to cast a wide net. Different insurers assess risk very differently, particularly for older homes with non-standard construction materials. A quote that seems high from one insurer may be significantly cheaper from another.

3. Consider a higher excess. Opting for a higher building or contents excess can reduce your annual premium. If you have the financial capacity to cover a larger out-of-pocket cost in the event of a claim, this trade-off can make sense — particularly for lower-probability events.

4. Ask about discounts and bundling. Many insurers offer discounts for bundling home and contents insurance (which this policy already does), paying annually rather than monthly, or for installing security features. It's always worth asking what discounts are available before accepting a quote.

---

Ready to Find a Better Deal?

If this quote has you wondering whether there's a more competitive option out there, the good news is that comparing is easier than ever. At CoverClub, we aggregate real insurance pricing data so you can see exactly how your quote stacks up — and find a policy that actually fits your budget.

Get a home insurance quote now and see what Alpha homeowners are actually paying in 2025. You might be surprised at the difference a comparison can make.