If you own a free standing home in Amaroo, ACT 2914, understanding what you should be paying for home and contents insurance is one of the smartest financial checks you can make. Premiums vary significantly depending on your property's features, the level of cover you choose, and how insurers assess risk in your area. In this article, we break down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Amaroo — and put it in context against suburb, territory, and national benchmarks.

---

Is This Quote Fair?

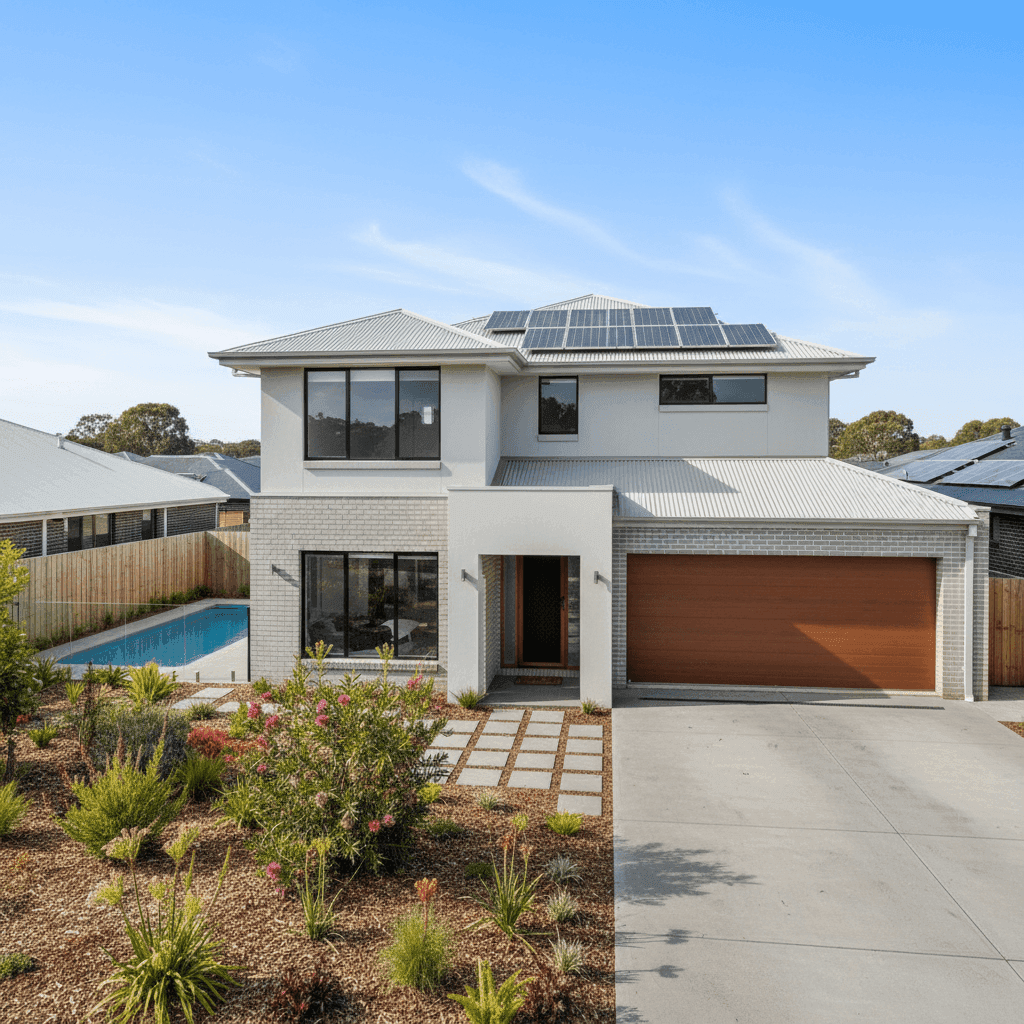

The quote in question comes in at $2,175 per year (or $213/month) for a combined home and contents policy. The building is insured for $1,005,000 and contents for $99,000, with a $1,000 excess applying to both building and contents claims.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you dig into the numbers. The suburb average for Amaroo sits at $2,057 per year, with a median of $1,925. At $2,175, this quote is modestly above both figures — but well within the normal range. The suburb's 75th percentile is $2,504, meaning roughly a quarter of Amaroo homeowners are paying more than this quote. In other words, you're not being overcharged, but there may be room to do better.

It's also worth noting that a building sum insured of over $1 million is on the higher end for the suburb, which naturally pushes the premium upward. If the rebuild cost estimate is accurate, that's appropriate coverage — but it's always worth reviewing your sum insured periodically to make sure it reflects current construction costs rather than an inflated or outdated figure.

---

How Amaroo Compares

To understand whether Amaroo is an expensive or affordable place to insure a home, it helps to zoom out.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Amaroo (2914) | $2,057/yr | $1,925/yr |

| ACT (Territory) | $2,288/yr | $2,186/yr |

| National | $5,347/yr | $2,764/yr |

| Unincorporated ACT (LGA) | $2,172/yr | — |

Amaroo compares very favourably on every measure. The suburb's average premium sits $231 below the ACT average and a remarkable $3,290 below the national average. Even the national median — a more representative figure than the average, which is skewed by high-risk coastal and cyclone-prone regions — is $839 higher than Amaroo's median.

This reflects Amaroo's relatively low natural hazard profile. As a planned suburb in the ACT's north, it sits well away from flood-prone zones and is not classified as a cyclone risk area. Bushfire risk exists in parts of the ACT, but Amaroo's suburban density and distance from the rural urban interface generally keeps this risk manageable compared to many other parts of the country.

You can explore the full picture on our ACT insurance statistics page or compare Amaroo against the rest of Australia on our national stats page.

---

Property Features That Affect Your Premium

Every insurer weighs up a property's characteristics when calculating a premium. Here's how the key features of this particular home play into the pricing:

Brick Veneer Walls & Steel/Colorbond Roof Brick veneer is one of the most common and well-regarded construction types in Australia. It's durable, fire-resistant, and generally attracts favourable treatment from insurers. Combined with a steel Colorbond roof — which is lightweight, long-lasting, and performs well in hail events — this home has a construction profile that insurers tend to view positively.

Concrete Slab Foundation A slab foundation is standard for homes built from the 1990s onward in the ACT, and it's a stable, low-risk base. It eliminates the underfloor moisture and pest access issues sometimes associated with raised timber floors, which can subtly reduce risk in insurer assessments.

268 sqm Floor Area & Above-Average Fittings At 268 square metres, this is a generously sized home. Larger floor areas mean higher rebuild costs, which directly influences the building sum insured and, in turn, the premium. The above-average fittings quality — think stone benchtops, quality cabinetry, and premium fixtures — adds further to the replacement value. A $1,005,000 building sum insured is consistent with these characteristics given current ACT construction costs.

Swimming Pool A pool adds to the replacement cost of the property and introduces a small amount of additional liability exposure. Most home and contents policies cover the pool structure under the building component, but it's worth confirming your policy covers pool equipment, fencing, and any associated structures.

Solar Panels Solar panels are generally covered under building insurance as a fixed structure, but coverage varies between insurers. Some policies cover panels for accidental damage and storm events as standard; others may treat them as optional extras. Given the investment involved — a typical system on a 268 sqm home could be worth $8,000–$15,000 — it's worth verifying your policy terms explicitly.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar panels, it should be covered under the building component of your policy, but confirm this is the case and that the sum insured adequately accounts for its replacement cost.

---

Tips for Homeowners in Amaroo

1. Review Your Building Sum Insured Annually Construction costs in the ACT have risen considerably over recent years. A sum insured set several years ago may no longer reflect the true cost of rebuilding your home to the same standard. Most insurers offer a calculator, and independent quantity surveyors can provide a formal assessment if needed.

2. Confirm Solar Panel and Pool Coverage Don't assume these are included — read your Product Disclosure Statement (PDS) carefully. Check whether solar panels are covered for all damage types, and whether your pool equipment and fencing are included in the building definition.

3. Consider Your Excess Strategically This policy carries a $1,000 excess on both building and contents. Opting for a higher excess (say, $2,000) can meaningfully reduce your annual premium. If you have a healthy emergency fund and are unlikely to make small claims, this trade-off often makes financial sense.

4. Compare at Renewal, Not Just at Inception Insurers often reserve their best rates for new customers. Each year at renewal, it's worth running a fresh comparison — even if you're happy with your current insurer. Loyalty doesn't always pay in the insurance market.

---

Get a Better Deal on Home Insurance

Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to see real, comparable quotes for your specific property in Amaroo and across the ACT.

Get a home insurance quote at CoverClub — it takes just a few minutes and could save you hundreds of dollars a year.