Armidale is one of New England's most distinctive regional cities — known for its university town character, cool-climate seasons, and a mix of heritage and modern housing stock. For owners of a free standing home in this part of New South Wales, understanding what drives your home insurance premium can make a real difference to your budget. This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Armidale (postcode 2350), and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The annual premium in question comes in at $3,198 per year (or $300 per month) for a combined home and contents policy. The building is insured for $679,000 and contents are covered for $50,000, with a $1,000 excess applying to both building and contents claims.

Based on CoverClub's pricing data, this quote has been rated Fair — Around Average. That's a reasonable outcome for a property of this size and construction type in regional NSW. It's not the cheapest on the market, but it's also well within the normal range for comparable homes in the area — meaning the insurer isn't dramatically overcharging for the risk profile involved.

For homeowners wondering whether they should shop around, a "Fair" rating suggests there's modest room for improvement, but you're unlikely to find dramatically lower pricing without adjusting your cover or excess levels.

---

How Armidale Compares

To understand whether this premium is truly competitive, it helps to look at the broader data. According to CoverClub's Armidale suburb statistics, the local pricing landscape looks like this:

| Benchmark | Premium |

|---|---|

| Suburb average | $3,270/yr |

| Suburb median | $3,435/yr |

| Suburb 25th percentile | $2,259/yr |

| Suburb 75th percentile | $4,111/yr |

| LGA (Uralla) average | $2,816/yr |

At $3,198 per year, this quote sits below both the suburb average and median — a positive sign. It falls comfortably in the middle of the distribution, above the cheapest 25% of quotes but well short of the more expensive end of the market.

Zooming out to a state level, the picture shifts considerably. The NSW state average premium is a striking $9,528 per year, though this figure is heavily influenced by high-value coastal and flood-prone properties across the state. The NSW median is a more representative $3,770 per year — and this quote comes in below that, which is encouraging.

At the national level, the average premium sits at $5,347 per year, while the national median is $2,764 per year. The fact that this quote is above the national median reflects the realities of insuring a larger-than-average home with a substantial building sum insured in a regional area with its own risk characteristics.

Overall, the data paints a consistent picture: this is a reasonable, mid-range premium for a property of this type in Armidale.

---

Property Features That Affect Your Premium

Several characteristics of this particular home will have influenced how insurers assessed the risk — and therefore the price.

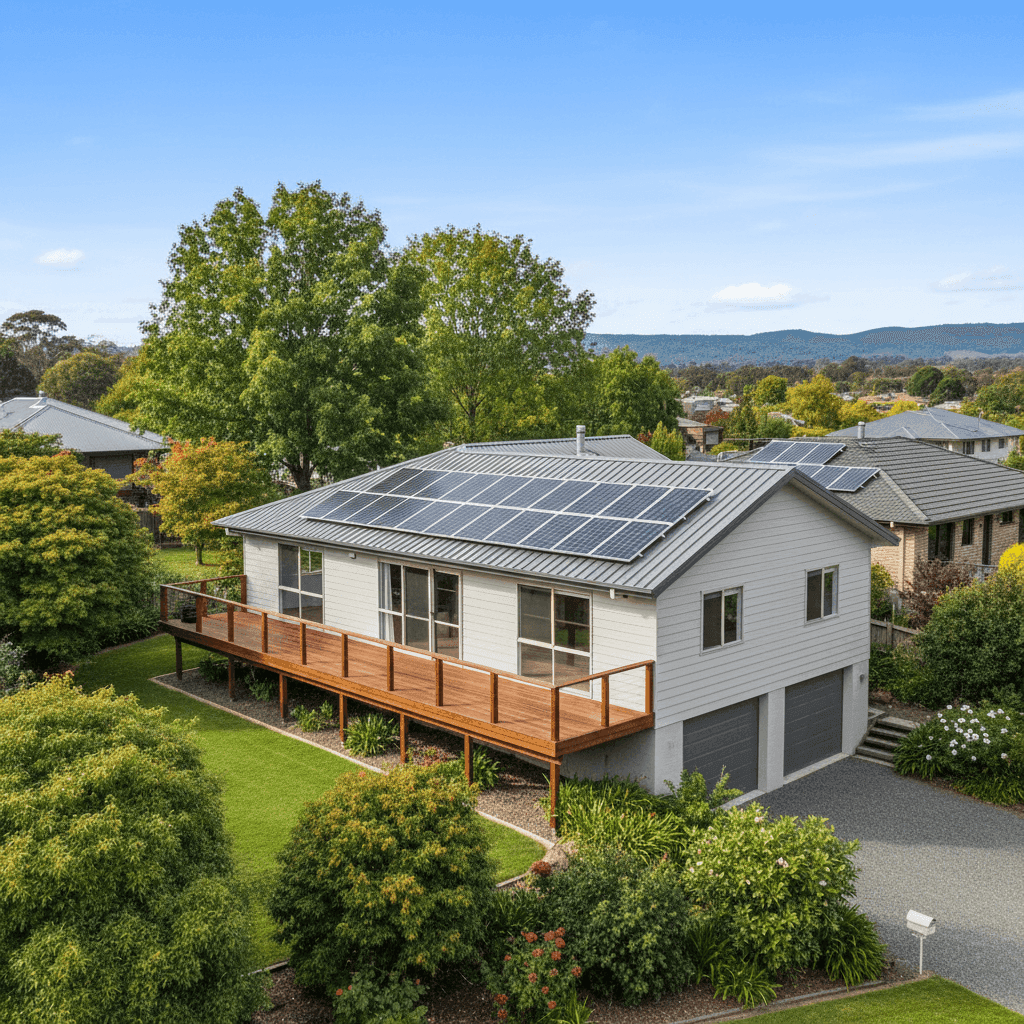

Hardiplank/Hardiflex external walls are a fibre cement cladding product widely used in Australian residential construction. Insurers generally view this material favourably compared to timber weatherboard, as it offers good fire resistance and durability. This likely has a neutral-to-positive effect on the premium.

Steel/Colorbond roofing is another feature that tends to be viewed positively by underwriters. It's resilient, long-lasting, and performs well in extreme weather compared to older tile or corrugated iron roofing. For a property in Armidale — which experiences cold winters, occasional hail, and significant temperature swings — a robust roof is a meaningful risk factor.

Stump foundations are common in older Australian homes, particularly those built before the 1990s. This property, constructed in 1985, sits on stumps, which can introduce some maintenance considerations (such as subfloor ventilation and potential for movement over time). Insurers may factor in the age and construction style when pricing the policy.

Solar panels are present on this property. While solar systems add value to the home, they can also add to the cost of reinstatement in the event of a total loss — which may be partially reflected in the building sum insured of $679,000. Some insurers specifically cover solar panels under the building policy, so it's worth confirming this is the case with your provider.

Ducted climate control is another feature that increases the replacement cost of the home. Ducted systems are expensive to install and reinstate, and their inclusion in the building sum insured is important to verify.

The 244 sqm building size is above average for a regional home, which directly supports the higher building sum insured and contributes to a premium above the national median.

---

Tips for Homeowners in Armidale

1. Review your building sum insured regularly. With construction costs continuing to rise across Australia, the cost to rebuild a 244 sqm home with ducted climate control and solar panels can change significantly year to year. Make sure your sum insured reflects current building rates — underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider increasing your excess to reduce your premium. The current excess is set at $1,000 for both building and contents. If you have the financial buffer to absorb a higher out-of-pocket cost in the event of a claim, opting for a higher excess (say, $2,000) could meaningfully reduce your annual premium.

3. Shop around at renewal time. Even with a "Fair" rating, the spread between the 25th and 75th percentile in Armidale is wide — from $2,259 to $4,111 per year. That's a gap of nearly $1,900 annually. Comparing multiple quotes before renewing could put you in a much better position without sacrificing cover quality.

4. Check what's covered for your solar panels and ducted system. Not all policies treat solar panels and ducted HVAC systems the same way. Some insurers include them automatically under building cover; others may require specific endorsements. Clarifying this now avoids nasty surprises at claim time.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see multiple home and contents insurance options side by side, tailored to your specific property in Armidale.