Aroona is a well-established residential suburb on Queensland's Sunshine Coast, sitting within postcode 4551 and known for its family-friendly streets and proximity to Caloundra's beaches and amenities. If you own a free standing home in the area, understanding what you should expect to pay for home and contents insurance — and why — can make a real difference when it comes time to renew or shop around.

This article breaks down a recent home and contents insurance quote for a five-bedroom, three-bathroom free standing home in Aroona, comparing it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,454 per year (or $338 per month), covering a building sum insured of $798,000 and contents valued at $50,000, each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average. That assessment holds up well when you dig into the numbers. The suburb average for Aroona sits at $2,881 per year, with a median of $3,153. At $3,454, this quote lands just above the median but comfortably within the suburb's interquartile range — the middle 50% of quotes in the area fall between $1,568 and $4,098 per year. In other words, this is not an outlier; it's a reasonable reflection of what insurers are currently pricing for homes of this size and type in the suburb.

It's also worth noting that the building sum insured of $798,000 is on the higher end for the area, which naturally pushes the premium upward. A larger, well-appointed five-bedroom home with a pool and ducted climate control will always attract a higher premium than a modest three-bedroom dwelling — so comparing purely on premium without accounting for coverage level can be misleading.

---

How Aroona Compares

To put this quote in broader context, here's how Aroona stacks up against Queensland state averages and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Aroona (QLD 4551) | $2,881/yr | $3,153/yr |

| Queensland (State) | $4,547/yr | $3,931/yr |

| Sunshine Coast (LGA) | $4,608/yr | — |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, the Aroona suburb average of $2,881 is notably lower than both the Queensland state average ($4,547) and the Sunshine Coast LGA average ($4,608). This is encouraging for local homeowners — it suggests that Aroona, despite being part of a coastal LGA that typically attracts higher premiums due to weather risk, benefits from relatively favourable risk characteristics at the suburb level.

Second, Aroona's average is actually quite close to the national average of $2,965, which is somewhat unusual for a Queensland coastal suburb. Many parts of Queensland — particularly those exposed to cyclone risk or flooding — carry premiums well above the national norm. Aroona's position in this regard is a genuine positive for homeowners.

The quote of $3,454 sits above the suburb average but below the state and LGA averages, which is consistent with a larger-than-average home with a higher sum insured.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium. Understanding them helps explain the pricing — and highlights where there may be room to adjust.

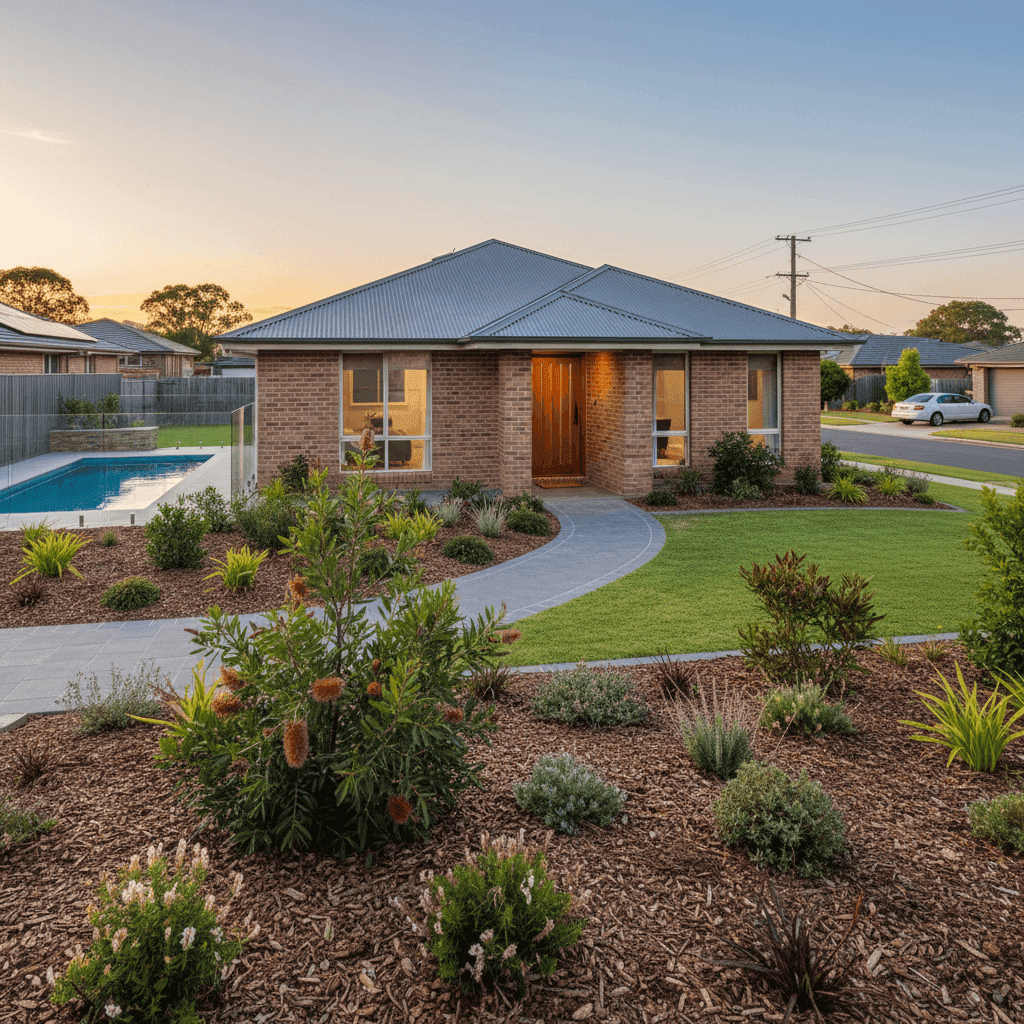

Size and sum insured: At 235 sqm with five bedrooms and three bathrooms, this is a substantial home. The building sum insured of $798,000 reflects the cost to rebuild a property of this scale, and insurers price accordingly. Getting your sum insured right is critical — underinsuring to reduce premiums can leave you significantly out of pocket after a major claim.

Brick veneer construction: Brick veneer external walls are generally viewed favourably by insurers. They offer solid fire resistance and structural durability, which can help moderate premiums compared to timber-framed or clad alternatives.

Steel/Colorbond roof: Colorbond roofing is a popular choice across Queensland for good reason — it's lightweight, durable, and performs well in high-wind conditions. Insurers typically regard it positively, particularly in areas with elevated storm risk.

Slab foundation: A concrete slab is considered a stable and low-risk foundation type. It reduces the likelihood of subsidence-related claims and is generally preferred by underwriters over suspended timber floors in terms of risk profile.

Swimming pool: The presence of a pool adds to the replacement cost of the property and introduces additional liability considerations, both of which contribute to a higher premium. Pools also require specific safety compliance under Queensland law, which insurers may factor into their assessment.

Ducted climate control: Ducted air conditioning systems are a significant asset that adds to the insured value of the building. Replacement or repair costs for these systems can be substantial, and their inclusion in the building sum insured is appropriate.

No cyclone risk: Aroona is not classified as a cyclone risk area, which is a meaningful premium advantage. Properties in cyclone-designated zones across Queensland and northern Australia can face dramatically higher premiums due to the catastrophic loss potential of tropical cyclones.

---

Tips for Homeowners in Aroona

1. Review your building sum insured annually Construction costs have risen significantly in recent years across Australia. The cost to rebuild your home today may be higher than it was when you first took out your policy. Use a building cost estimator or speak with a quantity surveyor to ensure your sum insured keeps pace with current rebuild costs — especially for a larger home like this one.

2. Compare quotes before renewing Loyalty doesn't always pay in the insurance market. Insurers frequently offer sharper pricing to new customers than to existing ones. Before your renewal date, get a fresh quote through CoverClub to see whether a better deal is available without sacrificing coverage quality.

3. Consider your excess level Both the building and contents excess on this policy sit at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. If you have sufficient savings to cover a larger out-of-pocket cost in the event of a claim, this trade-off can make good financial sense.

4. Ensure your pool and outdoor assets are correctly covered Pools, outdoor entertaining areas, and fixed garden structures can sometimes fall into grey areas within a policy. Check that your policy explicitly covers pool equipment, fencing, and associated structures, and that liability coverage extends to pool-related incidents — a legal requirement in Queensland regardless of insurance.

---

Ready to Compare?

Whether you're assessing a new quote or approaching your renewal, it pays to see the full picture. CoverClub makes it easy to compare home and contents insurance options side by side, so you can be confident you're getting fair value for your cover. Start comparing quotes today and see how your premium stacks up against what others in Aroona and across Queensland are paying.

For more localised data, explore the Aroona suburb insurance stats or browse Queensland-wide benchmarks to get a clearer sense of the market.