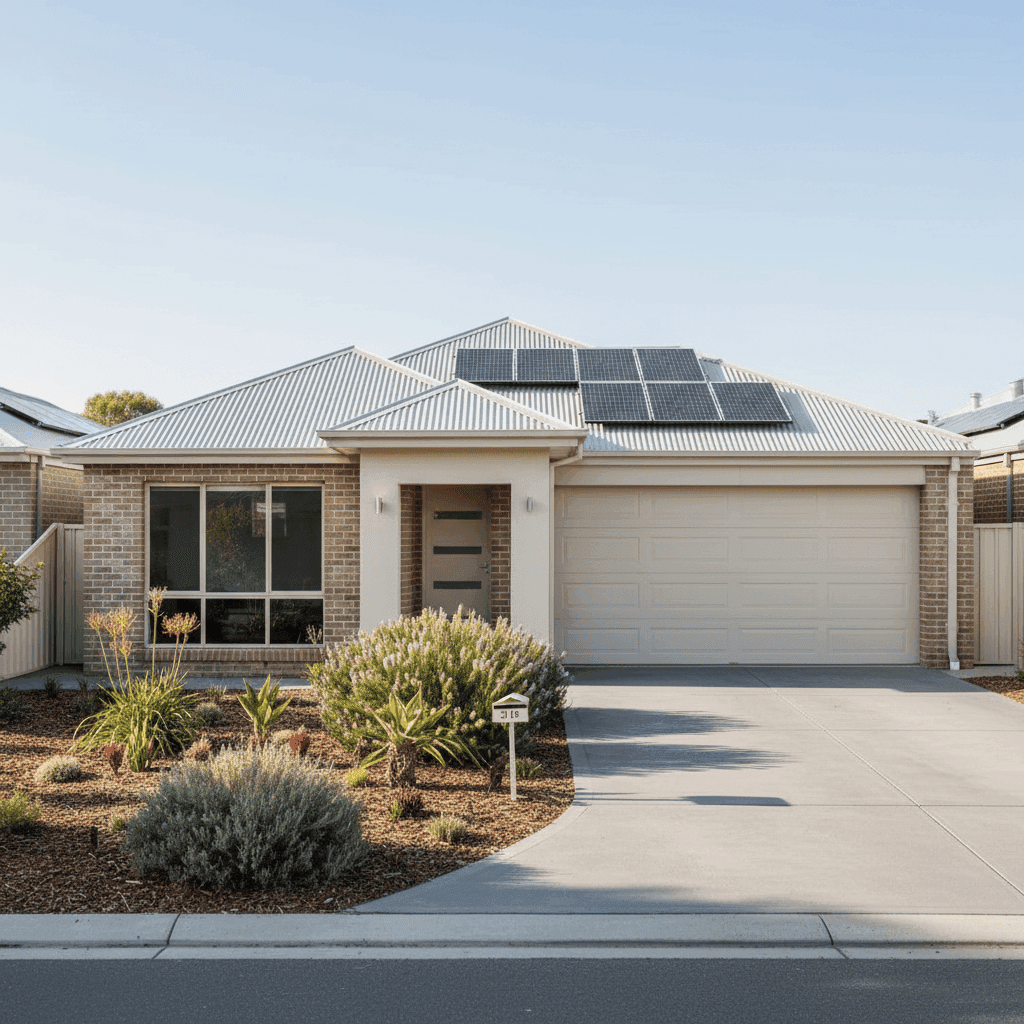

If you own a free standing home in Ashford, SA 5035, you're probably curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in Ashford, comparing it against local, state, and national benchmarks to help you make a confident decision.

---

Is This Quote Fair?

The short answer? Yes — and then some. This quote comes in at $1,202 per year (or roughly $115 per month) for combined home and contents cover, with a building sum insured of $535,000 and contents valued at $63,000. Both the building and contents excess sit at $1,000, which is a standard and reasonable figure.

Our price rating for this quote is CHEAP — below average — meaning it's well positioned relative to what most South Australian homeowners are paying. For a property of this size, age, and specification, that's a genuinely competitive outcome.

To put it in perspective: the South Australian state average premium is $2,433 per year, and the state median is $1,679 per year. This quote beats both figures comfortably. Nationally, the picture is even starker — the national average premium sits at $5,347 per year, with a national median of $2,764 per year. Compared to those figures, this Ashford homeowner is paying less than a quarter of the national average for equivalent cover.

---

How Ashford Compares

Understanding where Ashford sits in the broader insurance landscape helps contextualise why this quote is so competitive. While suburb-level aggregate data isn't available for this postcode at the time of writing, the West Torrens LGA average premium of $1,992 per year gives us a useful local benchmark.

Here's a quick snapshot:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,202 |

| West Torrens LGA Average | $1,992 |

| SA State Average | $2,433 |

| SA State Median | $1,679 |

| National Average | $5,347 |

| National Median | $2,764 |

This quote is approximately 40% below the LGA average and 51% below the SA state average — a significant saving. Ashford is an established inner-western suburb of Adelaide, located roughly 4 kilometres from the CBD. Its relatively flat terrain, urban infrastructure, and distance from high-risk bushfire zones all contribute to a more favourable risk profile compared to many regional or coastal South Australian postcodes.

You can explore more local data on the Ashford suburb stats page as it becomes available.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — it's driven by a combination of property characteristics, location risk factors, and the level of cover you select. Here's how the specific features of this property influence the premium:

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is one of the most common and well-regarded wall types in Australian suburban homes. It offers solid fire resistance and durability, which insurers generally view favourably. Paired with a steel Colorbond roof, this home has a robust, low-maintenance external envelope. Colorbond is lightweight, non-combustible, and highly resistant to the elements — all factors that reduce the likelihood of significant weather-related claims.

Concrete Slab Foundation

A slab-on-ground foundation is standard for homes built in this era and region. It's structurally sound and doesn't carry the subsidence or moisture risks sometimes associated with older timber stumped foundations, which can be a premium driver in some areas.

Construction Year: 2004

At just over 20 years old, this home sits in a sweet spot for insurers. It's modern enough to comply with updated building codes — including improved cyclone and earthquake standards introduced in the early 2000s — but not so new that replacement costs are inflated by cutting-edge materials or bespoke finishes.

Solar Panels

The presence of solar panels is worth noting. While they add value to the property and are included in the building sum insured, they can marginally increase premiums due to the cost of replacement and the specialist installation required. However, the impact here appears minimal, suggesting the insurer has priced this risk proportionately.

Ducted Climate Control

A ducted air conditioning system is a meaningful inclusion in the building's value. These systems can cost $10,000–$20,000 or more to replace, so ensuring your sum insured accounts for this is important — and it appears this policy does.

Standard Fittings & Tiled Flooring

With standard-quality fittings and tile flooring throughout, there are no luxury finishes inflating the replacement cost estimate. Tiles are durable, easy to replace, and don't carry the same moisture sensitivity as timber or carpet, which keeps claims risk lower.

No Pool, No Cyclone Risk Zone

The absence of a swimming pool removes a common liability and maintenance risk from the equation. And being outside a designated cyclone risk area means the property isn't subject to the significant premium loadings that apply to homes in northern Australia.

---

Tips for Homeowners in Ashford

Even with a competitive quote, there are always ways to optimise your cover and keep costs in check over time.

- Review your sum insured annually. Construction costs in South Australia have risen considerably in recent years. Make sure your $535,000 building sum insured still reflects what it would actually cost to rebuild your home from scratch — including the slab, fitouts, and solar system. Underinsurance is one of the most common and costly mistakes homeowners make.

- Document your contents thoroughly. With $63,000 in contents cover, it's worth creating a room-by-room home inventory with photos and receipts where possible. This makes any future claim significantly smoother and reduces the risk of disputes over item values.

- Ask about bundling discounts. Many insurers offer reduced premiums when you combine home and contents cover (as this policy does) or when you hold multiple policies — such as car insurance — with the same provider. It's always worth asking.

- Consider your excess carefully. A $1,000 excess is standard, but opting for a higher voluntary excess can lower your annual premium further. If you have an emergency fund and are unlikely to make small claims, this can be a smart trade-off.

---

Compare More Quotes at CoverClub

This quote is a strong result for an Ashford homeowner — but the best way to know you're getting the right deal is to compare. At CoverClub, we make it easy to benchmark your current premium against the market and explore options from multiple insurers in minutes. Get a home insurance quote today and see how your property stacks up.