Ashgrove is one of Brisbane's most sought-after inner-north-west suburbs — a leafy, family-friendly pocket of Queensland that blends character homes with modern builds. For owners of a free standing home in this postcode, understanding what you're paying for home and contents insurance, and whether that figure is reasonable, is an important part of managing household finances. This article breaks down a real quote for a four-bedroom, four-bathroom property in Ashgrove QLD 4060, and puts the numbers into context.

---

Is This Quote Fair?

The quote in question comes to $2,572 per year (or $263 per month) for combined home and contents cover, with a building sum insured of $1,052,000 and contents valued at $99,000. Both the building and contents excess are set at $5,000.

Our price rating for this quote is FAIR — Around Average, which means it sits in a reasonable range relative to what other homeowners in the area are paying. It's not the cheapest quote on the market, but it's well below what many comparable properties in the suburb are being quoted.

To put it plainly: this homeowner is paying less than the suburb average and less than both the Queensland state average and the national average. That's a solid outcome, particularly given the property's above-average fittings quality, generous size, and additional features like a pool and solar panels — all of which typically push premiums higher.

---

How Ashgrove Compares

Benchmarking your premium against local and broader data is one of the best ways to gauge value. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $2,572/yr |

| Ashgrove suburb average | $3,520/yr |

| Ashgrove suburb median | $3,398/yr |

| Ashgrove 25th percentile | $2,149/yr |

| Ashgrove 75th percentile | $3,880/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

Based on 47 quotes sampled in the Ashgrove area.

At $2,572, this quote sits between the suburb's 25th percentile ($2,149) and the median ($3,398) — meaning it's cheaper than more than half of comparable quotes in the area. It also comes in roughly $948 below the suburb average and a substantial $1,975 below the Queensland state average.

Interestingly, Queensland premiums are notably elevated compared to the rest of the country, largely due to the state's exposure to severe weather events including storms, flooding, and cyclones. While Ashgrove itself is not classified as a cyclone risk area, broader Queensland pricing reflects the state's overall risk profile. You can explore Ashgrove-specific insurance stats, Queensland-wide data, and national benchmarks on CoverClub.

It's also worth noting the LGA (Brisbane) average of $16,277/yr — a figure that reflects the wide spread of properties across the Brisbane local government area, including high-risk or high-value outliers that can significantly skew averages upward.

---

Property Features That Affect Your Premium

Every home is different, and insurers price policies based on a detailed combination of property characteristics. Here's how the features of this particular Ashgrove home likely influence the premium:

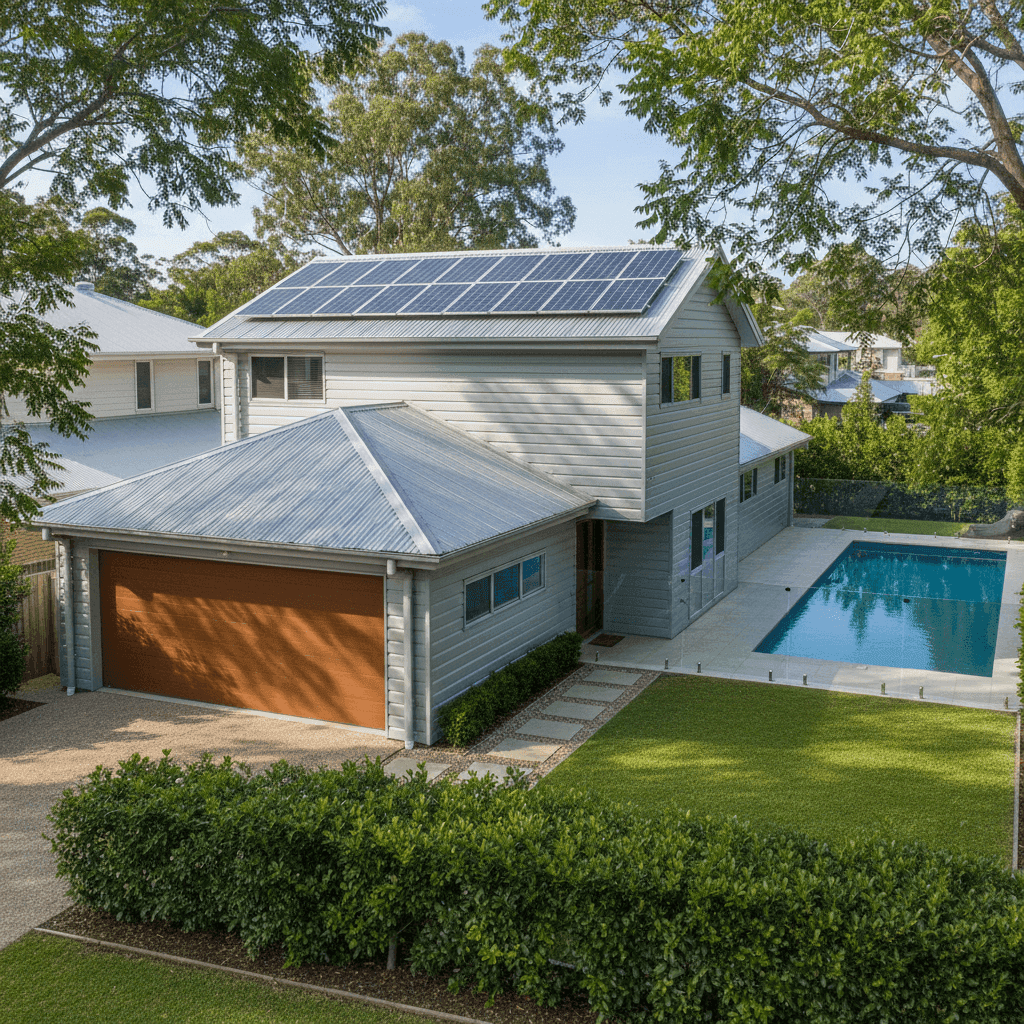

Construction (2009 build, aluminium walls, Colorbond roof, slab foundation) A home built in 2009 benefits from relatively modern construction standards, which generally translates to better structural resilience and lower risk in the eyes of insurers. Aluminium cladding is lightweight and low-maintenance, while a steel Colorbond roof is highly regarded for its durability and resistance to corrosion, fire, and harsh weather. A concrete slab foundation is considered stable and predictable — a positive from an underwriting perspective.

Flooring: Timber and Laminate Timber and laminate flooring can be more expensive to replace than tiles or carpet, which may contribute modestly to the building sum insured and overall premium. However, these materials are standard in quality Brisbane homes and are unlikely to be a significant pricing driver on their own.

Above-Average Fittings Quality This is one of the more influential factors. Above-average fittings — think stone benchtops, quality cabinetry, premium tapware, and high-end appliances — increase the cost to rebuild or repair, which flows through to a higher sum insured and, in turn, a higher premium.

Pool Swimming pools add liability exposure and increase the replacement cost of the property. Most insurers factor in pool fencing compliance and the cost of pool equipment when calculating premiums.

Solar Panels Solar systems are now a standard feature on many Australian homes, but they do add to the replacement cost of the building. Insurers generally include solar panels under building cover, and the value of the system is typically reflected in the sum insured.

Size: 235 sqm At 235 square metres, this is a generously sized home. Larger floor areas mean higher rebuild costs, which directly supports a building sum insured of over $1 million.

---

Tips for Homeowners in Ashgrove

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps to make sure you're getting the best deal:

- Review your sum insured regularly. Construction costs have risen sharply in recent years. An outdated sum insured could leave you underinsured in the event of a total loss. Use a building cost calculator or speak with a quantity surveyor to validate your figure annually.

- Consider your excess carefully. This quote carries a $5,000 excess on both building and contents. A higher excess generally reduces your premium, but make sure you can comfortably cover that amount out of pocket if you need to make a claim. If cash flow is a concern, a lower excess with a slightly higher premium may be a better fit.

- Don't overlook contents. At $99,000, the contents value here is a meaningful figure. Take time to do a proper home inventory — many Australians underestimate the combined value of their furniture, electronics, clothing, and personal items. Underinsuring your contents can be just as costly as underinsuring the building.

- Compare quotes at renewal time. The insurance market is competitive, and premiums can vary significantly between providers for the same property. Even if your current insurer offers a "fair" price, running a comparison at renewal could reveal better value — or simply give you the confidence that you're already on a good deal.

---

Ready to Compare?

If you own a home in Ashgrove or anywhere else in Australia, CoverClub makes it easy to see how your current premium stacks up and find competitive quotes from a range of insurers. Get a home insurance quote today and take the guesswork out of protecting one of your most valuable assets.