If you own a free standing home in Avenell Heights, QLD 4670, you've probably wondered whether you're paying a fair price for building insurance — or quietly overpaying year after year. This article breaks down a real building-only insurance quote for a four-bedroom, two-bathroom home in the suburb, and stacks it up against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,875 per year (or $281/month) for building-only cover, with a $2,000 building excess and a sum insured of $674,000. Our rating for this quote is Expensive — above average for the area.

That label isn't just a gut feeling. When we compare this figure against the suburb average for Avenell Heights of $2,372/year, this quote sits roughly 21% higher. More telling still is the suburb median of just $1,783/year — meaning this homeowner is paying over $1,000 more annually than the typical Avenell Heights policyholder in our dataset.

Even against the suburb's 75th percentile of $1,880/year, this quote exceeds what 75% of comparable local properties are paying. That's a meaningful gap, and one worth investigating before simply renewing.

That said, context matters. Every property is different, and factors like construction materials, sum insured, and individual insurer risk assessments all influence the final figure. The key takeaway is that there's likely room to shop around.

---

How Avenell Heights Compares

To put this quote in broader perspective, here's how Avenell Heights stacks up against Queensland and the national average:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Avenell Heights (suburb) | $2,372/yr | $1,783/yr |

| Queensland (state) | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. Queensland as a whole carries some of the highest home insurance premiums in the country — driven largely by cyclone, flood, and storm risk across much of the state. Avenell Heights, however, sits well below both the state average and the national average, suggesting it's a relatively lower-risk suburb from an insurer's perspective.

This is actually good news for homeowners in the area. The suburb's average of $2,372/year is around 48% cheaper than the Queensland state average, and also sits below the national average of $2,965/year. Residents here benefit from a comparatively favourable risk profile.

Given this context, a quote of $2,875/year — while above the suburb norm — is still significantly cheaper than what many Queenslanders are paying. However, that's cold comfort if cheaper options are available for the same property.

---

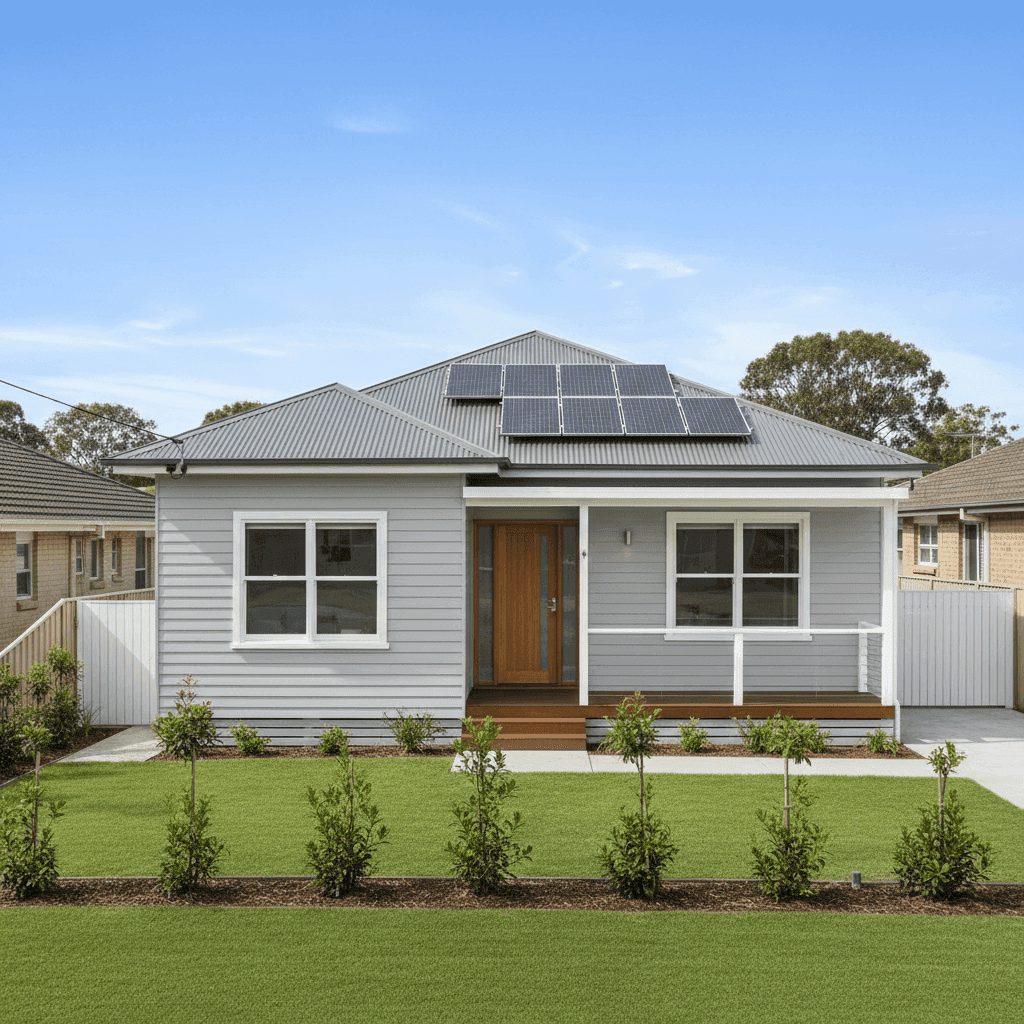

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk. Here's what's relevant:

Construction year (2021): A relatively new build is generally viewed favourably by insurers. Newer homes meet modern building codes, tend to have updated electrical and plumbing systems, and are less likely to have hidden structural issues. This should work in the homeowner's favour.

Hardiplank/Hardiflex external walls: Fibre cement cladding like Hardiplank is considered a durable, fire-resistant material. Most insurers view it positively compared to timber weatherboard, which can carry higher fire risk. It's a neutral-to-positive factor for premiums.

Steel/Colorbond roof: Colorbond roofing is widely regarded as one of the most insurer-friendly roofing materials in Australia. It's durable, low-maintenance, resistant to fire and pests, and handles Queensland's heat and storm conditions well. This should help keep premiums down relative to tile or older iron roofing.

Slab foundation: Concrete slab foundations are standard in Queensland and generally attract no premium loading. They're stable, resistant to termite ingress, and well-suited to the local climate.

Solar panels: The presence of solar panels adds to the replacement value of the home, which is reflected in the sum insured of $674,000. Insurers will factor in the cost of replacing panels in the event of a covered loss. It's worth confirming with your insurer that solar panels are explicitly covered under your policy.

No pool, no ducted climate control: The absence of a pool removes a common liability and maintenance risk that can nudge premiums upward. Similarly, no ducted air conditioning means fewer mechanical systems that could fail or cause damage.

Tiled flooring throughout: Tiles are durable, water-resistant, and low-risk from an insurer's perspective — a minor but positive factor.

Overall, this is a well-constructed, modern home with features that should attract competitive pricing. The above-average premium is likely more a function of the insurer selected and the sum insured level than any inherent risk with the property itself.

---

Tips for Homeowners in Avenell Heights

1. Shop around — seriously. The single most effective way to reduce your premium is to compare quotes from multiple insurers. With a quote sitting above the suburb's 75th percentile, there's a strong case that alternative providers may offer equivalent cover for less. Use CoverClub to compare quotes specific to your property.

2. Review your sum insured carefully. At $674,000 for a 214 sqm home built in 2021, the sum insured works out to roughly $3,150 per sqm — which is on the higher end for a standard-quality finish. While it's critical not to underinsure, it's equally worth ensuring you haven't over-estimated the rebuild cost. An independent quantity surveyor can provide a more precise figure.

3. Consider adjusting your excess. This policy carries a $2,000 building excess. Opting for a higher excess (if your budget allows) can meaningfully reduce your annual premium. Conversely, if the excess feels too high for comfort, it's worth comparing policies with different excess structures to find the right balance.

4. Confirm solar panel coverage. With solar panels on the roof, make sure your policy explicitly covers them for damage from storms, hail, and fire. Not all standard building policies include solar panels by default, or they may be subject to sublimits. Ask your insurer directly and get it in writing.

---

Compare and Save with CoverClub

Whether you're renewing your policy or taking out cover for the first time, it pays to know where you stand. CoverClub makes it easy to see how your quote compares to others in Avenell Heights and across Queensland — so you can make a confident, informed decision. Get a building insurance quote today and find out if you could be paying less for the same level of protection.