If you own a free standing home in Avenell Heights, QLD 4670, you've probably wondered whether you're paying a fair price for home insurance — or whether there's room to save. This article breaks down a real home and contents insurance quote for a four-bedroom brick veneer home in the suburb, and puts it into context against local, state-wide, and national pricing data.

---

Is This Quote Fair?

The quote in question comes in at $3,541 per year (or roughly $339 per month) for combined home and contents cover, with a building sum insured of $634,000 and contents valued at $50,000. The building excess is $1,000 and the contents excess is $500.

Our price rating for this quote is FAIR — Around Average.

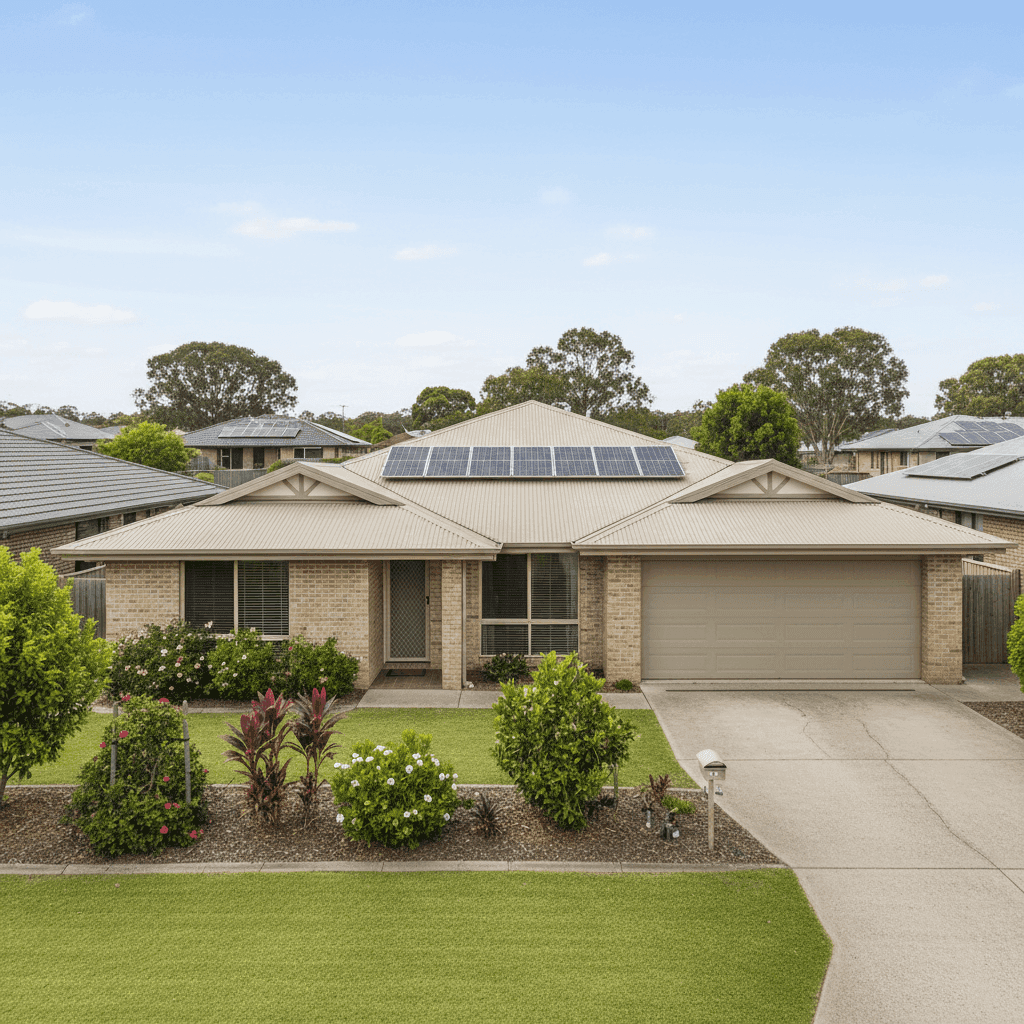

That rating reflects a premium that sits comfortably within the normal range for the area. It's not the cheapest quote you could find, but it's also well below what many Avenell Heights homeowners are paying. For a property of this size and specification — 205 sqm, built in 1995, with solar panels and ducted climate control — a "fair" rating is a reasonable outcome and suggests the insurer has priced the risk sensibly rather than loading the premium unnecessarily.

---

How Avenell Heights Compares

To understand what "fair" really means here, it helps to look at the numbers in context. Based on quotes collected for Avenell Heights (postcode 4670) from a sample of 45 policies:

| Benchmark | Premium |

|---|---|

| This quote | $3,541/yr |

| Suburb average | $4,393/yr |

| Suburb median | $3,163/yr |

| Suburb 25th percentile | $2,489/yr |

| Suburb 75th percentile | $5,095/yr |

This quote sits between the suburb median and the suburb average — meaning it's higher than what half of local policyholders pay, but noticeably below the average, which is pulled upward by some significantly more expensive policies. In practical terms, roughly 50–75% of comparable homes in the area are quoted somewhere between $3,163 and $5,095, so landing at $3,541 is a solid result.

The state-level picture is even more telling. Across all of Queensland, the average home insurance premium is a striking $9,129 per year, though the median sits at a more moderate $3,903. Queensland's elevated state average is driven by high-risk coastal and cyclone-prone areas, which push premiums skyward for many postcodes. At $3,541, this Avenell Heights quote comes in well below both the QLD average and median — a meaningful saving compared to many Queensland homeowners.

Zooming out to the national picture, the Australian average premium is $5,347/yr and the national median is $2,764/yr. This quote sits above the national median but below the national average, which is consistent with a property in a regional Queensland suburb that carries moderate risk rather than extreme exposure.

---

Property Features That Affect Your Premium

Several characteristics of this property influence where the premium lands — for better or worse.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which tends to translate into more competitive pricing compared to timber-framed or clad homes. Combined with a steel/Colorbond roof, the property benefits from a roofing material that handles Queensland's weather well — resistant to rust, lightweight, and relatively straightforward to repair or replace after storm damage.

The slab foundation is another positive signal for insurers. Slab-on-ground construction eliminates the underfloor cavity that can harbour moisture issues or pest damage, reducing certain categories of risk. Vinyl flooring is practical and cost-effective to replace if water damage occurs, which may also contribute to a more modest contents or building repair estimate.

Solar panels are worth noting. While they add value to the home and reduce energy costs, they do represent an additional insurable asset on the roof. Some insurers include solar panels under building cover automatically, while others may treat them differently — it's worth confirming exactly what your policy covers. The good news is that solar panels are now common enough that most mainstream insurers price them in without significant loading.

Ducted climate control adds to the overall replacement value of the home, which is partly why the building sum insured of $634,000 is appropriate for a 205 sqm home of this specification. Underinsuring a home with premium fixtures and systems is a genuine risk — if the sum insured doesn't reflect true rebuild costs, you could face a shortfall at claim time.

Importantly, this property is not in a designated cyclone risk area, which is a significant factor in keeping the premium reasonable. Many Queensland postcodes carry cyclone loading that can dramatically increase premiums, so Avenell Heights homeowners benefit from being outside that band.

---

Tips for Homeowners in Avenell Heights

1. Review your sum insured annually Building costs have risen considerably in recent years due to labour shortages and material price increases. A sum insured of $634,000 for a 205 sqm home is a reasonable starting point, but it's worth recalculating your rebuild cost each year — not just your market value — to make sure you're not underinsured.

2. Confirm solar panel coverage With solar panels on the roof, check your policy documents carefully. Verify whether panels are covered under building, contents, or as a separate item — and whether storm damage, electrical faults, and accidental breakage are all included. If anything is unclear, ask your insurer directly before you need to make a claim.

3. Consider your excess strategically This policy carries a $1,000 building excess and a $500 contents excess. Opting for a higher voluntary excess can reduce your annual premium, which makes sense if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim. Conversely, if cash flow is a concern, a lower excess might be worth the slightly higher premium.

4. Compare at renewal time A "fair" rating means this quote is competitive — but the insurance market changes constantly. New insurers enter the market, existing providers adjust their pricing models, and your own risk profile may shift over time. Running a fresh comparison at each renewal takes only a few minutes and could uncover a better deal without sacrificing coverage quality.

---

Compare Home Insurance Quotes in Avenell Heights

Whether you're reviewing an existing policy or shopping for cover on a new property, it pays to see what the full market has to offer. At CoverClub, we make it easy to compare home and contents insurance quotes side by side so you can make a confident, informed decision.

Get a home insurance quote today and find out where your premium sits relative to your neighbours — and the rest of Australia.