If you own a free standing home in Avondale, QLD 4670, you already know this part of Queensland offers a relaxed lifestyle at an accessible price point. But what about the cost of protecting your home? This article breaks down a real home and contents insurance quote for a 3-bedroom weatherboard property in Avondale, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $1,649 per year (or around $158 per month) for combined home and contents cover, with a building sum insured of $520,000 and contents valued at $50,000. The building excess is $5,000 and the contents excess is $1,000.

Our price rating for this quote? Cheap — below average. That's a strong result.

To put it in context, the average home and contents premium across Avondale sits at $2,834 per year, with a suburb median of $2,728. This quote comes in at roughly 42% below the suburb average — a significant saving of over $1,185 annually. Even compared to the 25th percentile of local quotes ($2,479), this premium is noticeably lower, suggesting it sits among the most competitively priced policies available for this area.

At the state level, the picture becomes even more striking. The Queensland state average premium is a substantial $9,129 per year, though the median is considerably lower at $3,903 — a gap that reflects the outsized influence of high-risk coastal and cyclone-prone areas dragging the average upward. Against either figure, this Avondale quote looks very attractive.

Nationally, the average home insurance premium in Australia is $5,347 per year, with a national median of $2,764. This quote edges just below the national median, reinforcing its "cheap" rating across every benchmark we apply.

---

How Avondale Compares

| Benchmark | Premium |

|---|---|

| This Quote | $1,649/yr |

| Avondale Suburb Average | $2,834/yr |

| Avondale Suburb Median | $2,728/yr |

| Avondale 25th Percentile | $2,479/yr |

| Avondale 75th Percentile | $3,124/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

It's worth noting that the Avondale suburb stats are based on a sample of 15 quotes, which is a reasonable baseline but not an enormous dataset. As more data comes in, these figures may shift. That said, the consistent gap between this quote and every available benchmark gives a clear signal — this is genuinely good value cover for the area.

The wide spread between Queensland's average ($9,129) and median ($3,903) is a reminder that premium data in QLD can be heavily skewed by properties in cyclone-declared zones, flood-prone areas, and high-value coastal locations. Avondale, sitting in the Bundaberg region, does not fall within a designated cyclone risk zone — a factor that meaningfully reduces the risk profile for insurers and, in turn, the premium for homeowners.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence where its premium lands — both positively and negatively.

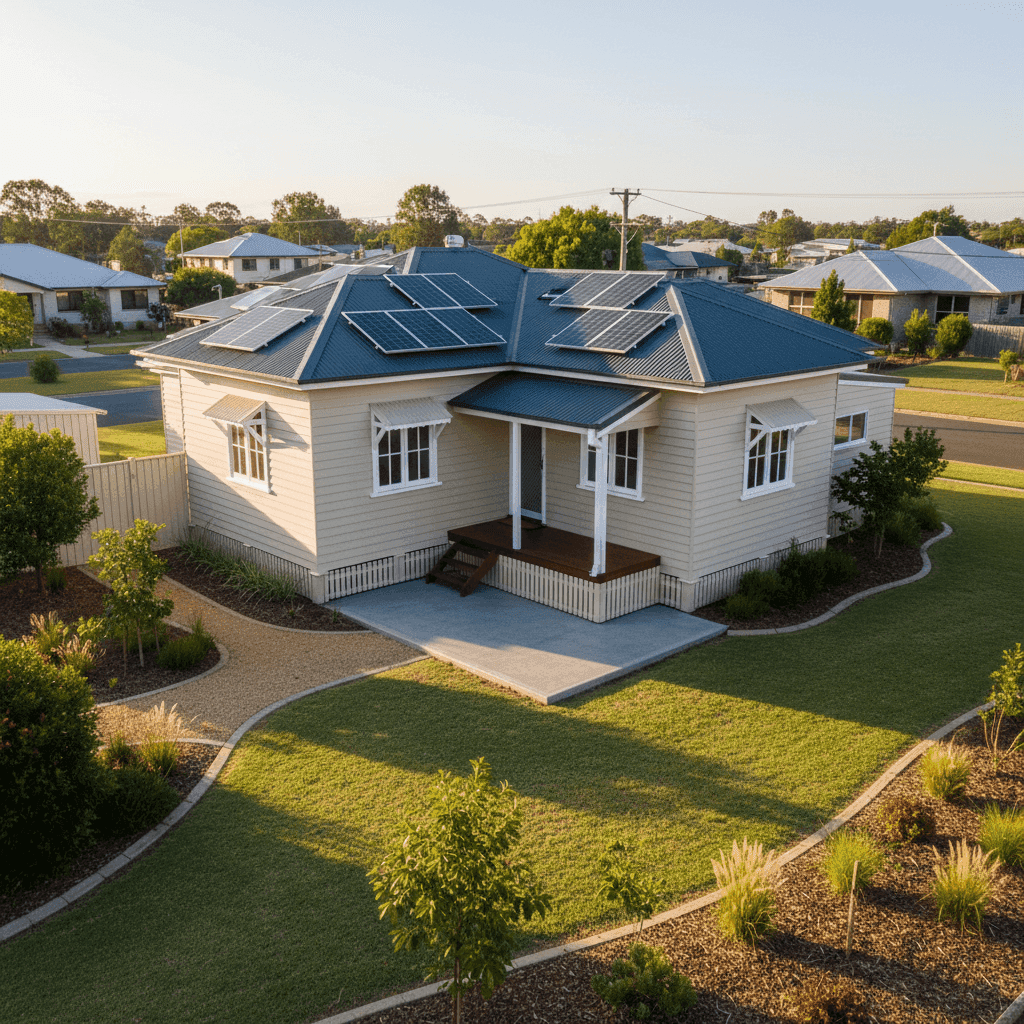

Weatherboard timber walls are one of the most significant rating factors. Timber-framed and clad homes are generally considered higher risk for fire and more susceptible to weather damage than brick veneer or rendered masonry. Insurers typically apply a loading for weatherboard construction, which can push premiums higher. Despite this, the overall quote remains competitive.

Steel/Colorbond roofing is a neutral-to-positive factor. Colorbond is durable, low-maintenance, and performs well in Australian conditions. It's generally viewed more favourably than older materials like terracotta tiles or corrugated iron in poor condition.

Slab foundation is one of the most straightforward and cost-effective foundation types from an insurance perspective. It reduces the risk of subsidence-related claims and is associated with lower premiums compared to suspended timber floors or older pier-and-beam setups.

Tile flooring throughout the home is a positive — tiles are non-combustible, easy to replace, and resistant to water damage, all of which reduce the likelihood and cost of claims.

Solar panels are present on this property. While solar adds value to a home, it also adds a small amount of insurable risk — panels can be damaged by hail, storms, or fire. Most policies cover rooftop solar as part of the building, but it's worth confirming this with your insurer.

Slight elevation (less than 1 metre) is a minor factor. The property is marginally raised above ground level, which can offer a small degree of flood mitigation compared to a flat slab at ground level — though the benefit is modest at this height.

No pool and no ducted climate control both simplify the risk profile. Pools introduce liability and maintenance risks, while ducted systems add mechanical complexity and replacement cost. Their absence helps keep the premium down.

The home was built in 2008, making it relatively modern. Newer builds tend to comply with more recent building codes, which typically means better structural integrity, improved fire resistance, and lower claims frequency — all factors that work in the homeowner's favour at renewal time.

---

Tips for Homeowners in Avondale

1. Review your sum insured regularly. Your building is insured for $520,000. Construction costs have risen sharply across Queensland in recent years, so it's worth checking that this figure accurately reflects what it would cost to rebuild your home from scratch — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Maintain your weatherboard cladding. Timber weatherboard requires periodic painting and sealing to prevent moisture ingress, rot, and pest damage. Keeping your cladding in good condition not only protects the home but can also support your claims eligibility — most policies exclude damage that results from lack of maintenance.

3. Confirm your solar panels are covered. Check your policy documents to ensure your rooftop solar system is explicitly included under the building sum insured. Some policies include it automatically; others may require a specific endorsement. Given the replacement cost of a solar system, this is worth a quick call to your insurer.

4. Consider your excess carefully. This policy carries a $5,000 building excess. While a higher excess typically lowers your premium, it also means you'll need to cover a significant amount out of pocket before your insurer steps in. Make sure this aligns with your financial comfort level — and that you'd genuinely be able to fund that gap in the event of a claim.

---

Compare Your Options at CoverClub

Whether you're renewing your current policy or shopping for the first time, it pays to compare. The quote analysed here is a strong result — but the right cover depends on your specific circumstances, risk tolerance, and budget. Get a home insurance quote at CoverClub to see how your property stacks up and find a policy that works for you.