Baldivis is one of Perth's fastest-growing southern suburbs, and with that growth comes a wave of modern family homes — and the very real need to protect them. This article takes a close look at a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Baldivis (WA 6171), breaking down whether the price is competitive, what's influencing the premium, and what local homeowners can do to get better value.

---

Is This Quote Fair?

The quote in question comes in at $1,621 per year (or around $158 per month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $300,000. The building excess sits at $2,000, with a separate contents excess of $600.

Our independent price rating for this quote is Fair — Around Average. That's not a bad result, but it does leave room to explore whether a better deal is out there.

To put it in context: the suburb average for Baldivis sits at $1,754 per year, meaning this quote comes in roughly $133 below the local average — a modest but meaningful saving. Compared to the suburb median of $1,136, however, it's sitting on the higher side, which suggests there are cheaper options available in the area for those willing to shop around.

The spread of premiums across Baldivis is worth noting: the 25th percentile sits at $944/yr, while the 75th percentile reaches $2,432/yr. That's a wide range, and it reflects just how much individual property characteristics — size, features, sum insured — can influence what you pay.

---

How Baldivis Compares

Zooming out from the suburb level paints an encouraging picture for Baldivis homeowners.

| Benchmark | Premium |

|---|---|

| This Quote | $1,621/yr |

| Baldivis Suburb Average | $1,754/yr |

| LGA Average (Rockingham) | $1,618/yr |

| WA State Average | $2,144/yr |

| WA State Median | $1,944/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

At $1,621, this quote sits 24% below the WA state average and a substantial 45% below the national average. For a property with a $900,000 building sum insured, a pool, solar panels, and ducted climate control, that's a genuinely competitive outcome relative to what Australians are paying elsewhere.

The Rockingham LGA average of $1,618 is almost identical to this quote, suggesting it's well-aligned with what similar properties in the broader local government area are attracting. Baldivis benefits from being a relatively low-risk suburb — no cyclone rating, newer housing stock, and predominantly brick construction — all of which help keep premiums in check compared to coastal or high-risk regions of WA and Queensland.

---

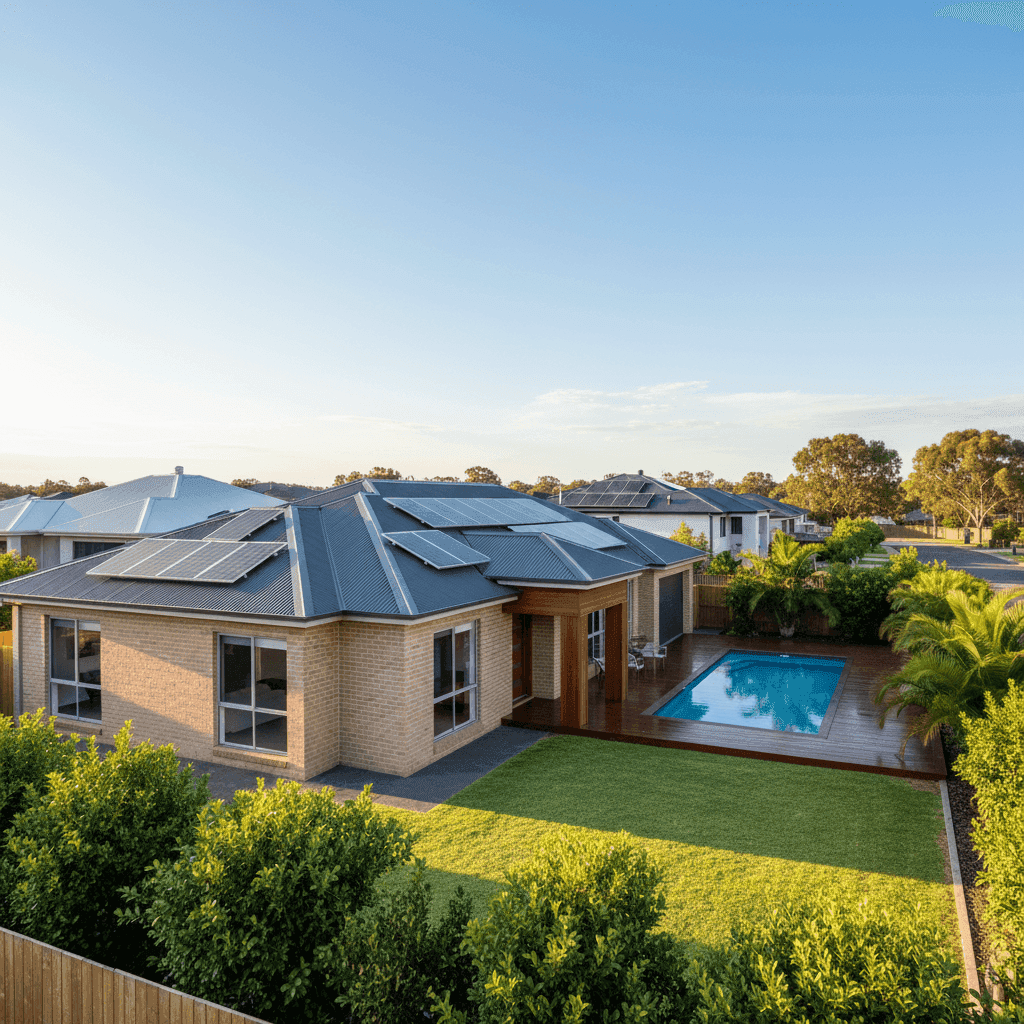

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the insurance premium, both positively and negatively.

Double Brick Construction

Double brick walls are among the most insurer-friendly external wall materials available. They offer excellent structural integrity, superior fire resistance, and strong protection against impact damage. Insurers typically view double brick homes more favourably than those with timber or clad exteriors, and this likely contributes to keeping the premium on the lower end.

Steel / Colorbond Roof

A Colorbond steel roof is another tick in the right column. It's durable, low-maintenance, and performs well in high-wind conditions. Unlike terracotta or concrete tiles, Colorbond is less prone to cracking and is generally cheaper to repair or replace — factors that reduce the insurer's risk exposure.

Slab Foundation

A concrete slab foundation is standard for modern Perth builds and presents minimal risk from a claims perspective. There's no subfloor space that can trap moisture or pests, and slabs tend to perform reliably in the sandy soils common across Baldivis.

Swimming Pool

A pool adds value to the property but also increases the insurer's liability exposure and the overall cost to rebuild or repair the home. It's a contributing factor to a higher sum insured and, in turn, a higher premium.

Solar Panels

Solar panels are increasingly common on Perth homes, and most insurers now include them under building cover — but they do add to the replacement cost calculation. With energy costs rising, panels are a worthwhile investment, though homeowners should confirm with their insurer exactly what's covered (panels, inverter, mounting hardware) and whether storm or hail damage is included.

Ducted Climate Control

Ducted air conditioning systems are expensive to install and replace. Including this in the building sum insured is appropriate, but it does nudge the overall insured value — and therefore the premium — upward.

Timber / Laminate Flooring

Flooring type primarily affects contents and internal finishes cover. Timber and laminate floors can be costly to replace if damaged by water or fire, so ensuring the building sum insured accounts for this is important.

Construction Year (2012)

At just over a decade old, this home is relatively new by insurance standards. Newer builds tend to comply with modern building codes, use updated materials, and carry lower risk of structural issues — all of which insurers reward with more competitive pricing.

---

Tips for Homeowners in Baldivis

1. Review your sum insured regularly The building is insured for $900,000, which is a substantial figure. Make sure this reflects the actual cost to rebuild (not the market value) including all features like the pool, solar system, and ducted air conditioning. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Shop around at renewal time A "Fair" rating means there's likely a better deal available. Use a comparison tool like CoverClub to benchmark your renewal quote against the broader market before you automatically roll over your policy.

3. Consider your excess settings This policy carries a $2,000 building excess. Opting for a higher excess can meaningfully reduce your annual premium — but make sure it's an amount you could comfortably cover out of pocket in the event of a claim.

4. Confirm your pool and solar are properly covered Ask your insurer specifically whether your pool (including fencing, pump, and filtration equipment) and solar panel system are fully covered under your building policy. Some policies have sub-limits or exclusions that catch homeowners off guard at claim time.

---

Find a Better Deal with CoverClub

Whether you're renewing an existing policy or insuring a new home in Baldivis, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb, your state, and across Australia. Get a home insurance quote today and find out if you're paying a fair price — or if you could be doing better.