Ballajura is a well-established residential suburb in Perth's north-eastern corridor, sitting within the City of Swan. Known for its family-friendly streets, parks, and solid brick homes built largely through the 1990s and 2000s, it's the kind of suburb where home insurance is a serious consideration for most owners. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Ballajura (postcode 6066), and helps you understand whether the premium on the table is reasonable — or whether there's room to do better.

---

Is This Quote Fair?

The quote in question sits at $2,827 per year (or $271/month) for combined home and contents cover, with a building sum insured of $1,168,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

Compared to the Ballajura suburb average of $1,487/year, this premium is nearly double what most local homeowners are paying. Even the 75th percentile for the suburb — meaning 75% of comparable quotes come in cheaper — sits at $1,869/year, still well below this figure.

That said, context matters. The high building sum insured of $1,168,000 for a 214 sqm home is a significant driver of cost. Replacement cost calculations in WA have climbed sharply in recent years due to construction material and labour price increases, so a higher sum insured isn't necessarily wrong — but it's worth double-checking whether that figure is accurate for your property, as over-insuring can mean unnecessarily inflated premiums.

---

How Ballajura Compares

To put this quote in proper perspective, here's how it stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,827/yr |

| Ballajura suburb average | $1,487/yr |

| Ballajura suburb median | $1,439/yr |

| Ballajura 25th percentile | $900/yr |

| Ballajura 75th percentile | $1,869/yr |

| WA state average | $2,811/yr |

| WA state median | $2,127/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| LGA (City of Swan) average | $4,057/yr |

A few things stand out here. While this quote is expensive relative to the Ballajura suburb average, it's actually very close to the WA state average of $2,811/year — suggesting that once you factor in property size and features, the premium isn't wildly out of step with broader Western Australian pricing.

Zooming out further, the national average of $5,347/year puts this quote in a much more favourable light. Homeowners in coastal Queensland, northern NSW, and cyclone-prone parts of the NT are routinely paying far more. Ballajura's location in Perth's inland suburbs, away from cyclone risk zones and flood-prone areas, generally keeps premiums more manageable.

The City of Swan LGA average of $4,057/year is notably higher than this individual quote, which may reflect a mix of higher-value properties and varying risk profiles across the broader LGA.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful impact on the insurance premium:

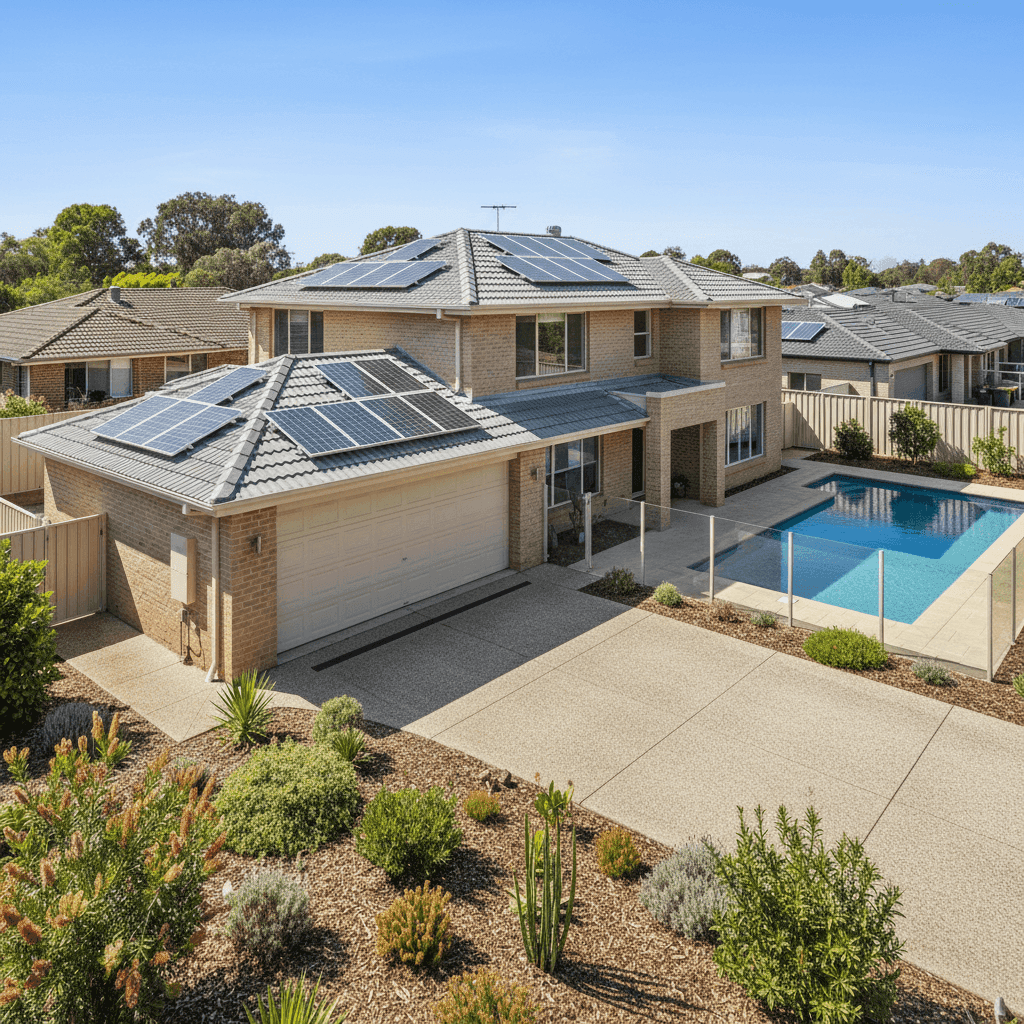

Double Brick Construction Double brick is widely regarded as one of the most durable and insurer-friendly wall materials in Australia. It offers strong resistance to fire, wind, and impact, which typically translates to lower risk in the eyes of insurers. This is a genuine positive for the premium.

Tiled Roof Terracotta or concrete tiles are a standard, well-regarded roofing material that insurers generally price favourably. They're durable and less susceptible to storm damage compared to some alternatives, though hail can occasionally be a factor in Perth's summer storm season.

Slab Foundation A concrete slab is a stable, low-maintenance foundation type that doesn't carry the subsidence or moisture risks associated with some older pier-and-beam constructions. This is another neutral-to-positive factor for insurers.

Swimming Pool Pools add to the insured value of the property and can introduce liability considerations, both of which can nudge premiums upward. Pool fencing compliance and maintenance are also factors some insurers assess at claims time.

Solar Panels Solar panels are increasingly common on Perth homes, but they do add replacement cost to the building sum insured. Depending on the insurer, panels may be covered under the building policy or require specific endorsement — it's worth confirming this is explicitly included in your cover.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and contribute to the overall replacement cost of the home. At 214 sqm, a full ducted system represents a meaningful portion of the building sum insured.

1999 Construction A home built in 1999 is now over 25 years old. While double brick construction ages well, some insurers may factor in the age of electrical systems, plumbing, and roofing when pricing risk. Keeping these systems well-maintained can support smoother claims outcomes.

---

Tips for Homeowners in Ballajura

1. Review Your Building Sum Insured Carefully At $1,168,000 for a 214 sqm home, the sum insured is on the higher end. Use an independent building replacement cost calculator (not the market value of your home) to verify this figure. Over-insuring inflates your premium without adding real protection, while under-insuring can leave you exposed at claim time.

2. Compare Multiple Quotes Before Renewing The gap between the cheapest and most expensive quotes in Ballajura is significant — from around $900/year at the 25th percentile to nearly $1,900 at the 75th. Insurers price risk differently, and loyalty doesn't always pay. Use CoverClub to compare quotes and see what's available for your specific property.

3. Confirm Solar Panels Are Explicitly Covered Not all policies automatically cover solar panel systems under the building section. Check your Product Disclosure Statement (PDS) to confirm panels, inverters, and associated wiring are included — and at what value.

4. Check Your Pool Fencing Compliance WA has specific pool fencing regulations under the Building Regulations 2012. Non-compliant fencing can affect liability cover and potentially complicate claims. An annual check ensures you remain compliant and fully protected.

---

Ready to Find a Better Rate?

Whether you're renewing your existing policy or insuring a Ballajura property for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to see how your premium stacks up and find competitive cover tailored to your property. Get a quote today and take the guesswork out of home insurance.