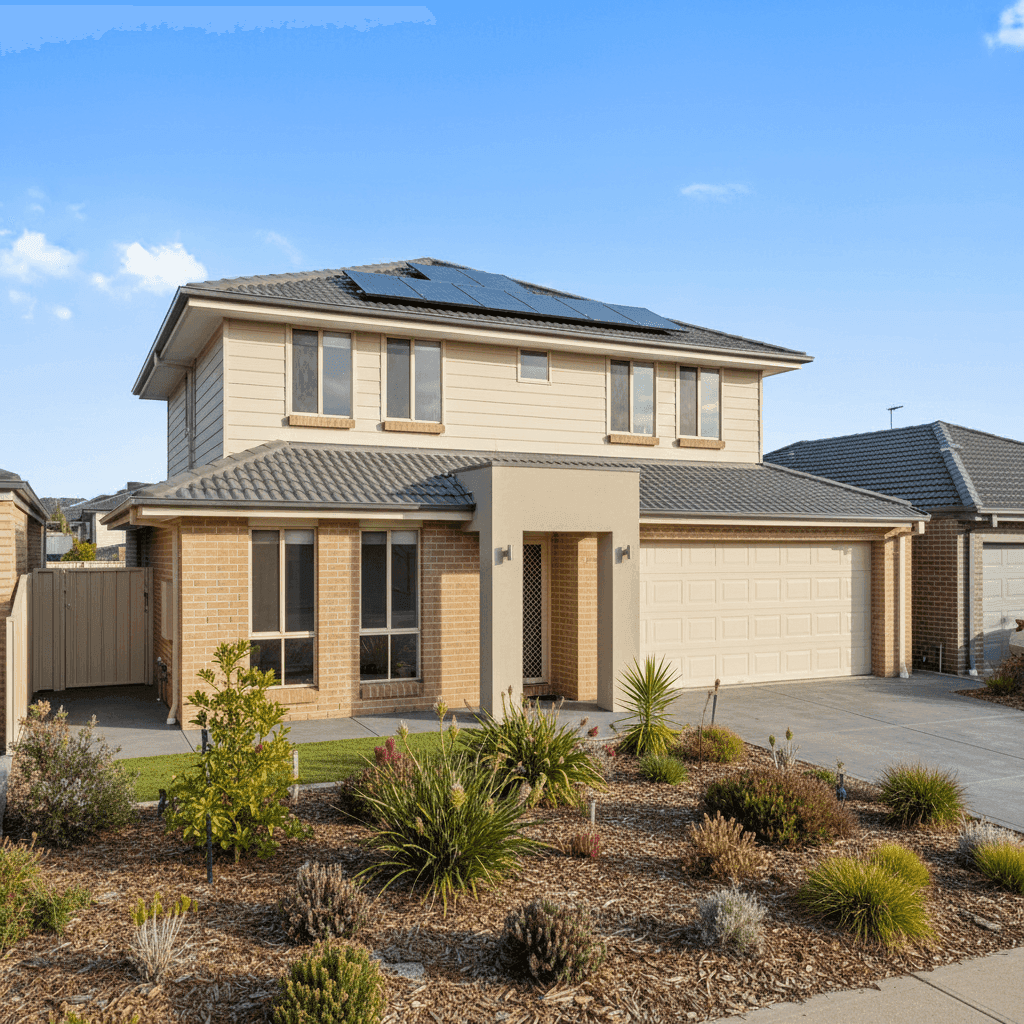

If you own a free standing home in Banksia Grove, WA 6031, you're likely paying close attention to the cost of home and contents insurance — especially as premiums across Australia continue to climb. This article breaks down a real insurance quote for a four-bedroom, double brick home in the suburb, putting the numbers in context so you can make a genuinely informed decision about your cover.

---

Is This Quote Fair?

The quote in question comes in at $1,586 per year (or $152/month) for combined home and contents insurance, covering a building sum insured of $501,000 and contents valued at $50,000. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Looking at recent quotes collected for Banksia Grove, the suburb average sits at $1,398/yr and the median at $1,121/yr. This quote lands above both of those figures, but it's well within the normal spread — the 75th percentile for the suburb is $1,769/yr, meaning roughly a quarter of homeowners in the area are paying more than this quote.

So while you're not getting the cheapest deal on the street, you're not being stung either. There's room to potentially do better with some shopping around, but this is a defensible premium for the property type and cover level.

---

How Banksia Grove Compares

One of the most reassuring things about insuring a home in Banksia Grove is just how favourably the suburb stacks up against broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Banksia Grove (suburb) | $1,398/yr | $1,121/yr |

| Wanneroo LGA | $1,550/yr | — |

| Western Australia | $2,811/yr | $2,127/yr |

| National | $5,347/yr | $2,764/yr |

The numbers tell a clear story. Banksia Grove sits comfortably below the WA state average of $2,811/yr, and dramatically below the national average of $5,347/yr. Even within the Wanneroo LGA, Banksia Grove comes in cheaper than the local government area average of $1,550/yr.

Much of this comes down to risk profile. Banksia Grove is not classified as a cyclone risk area, which is a significant cost driver in northern parts of Western Australia. The suburb also benefits from being a relatively modern residential development with consistent construction standards — factors that insurers weigh heavily when pricing premiums.

It's worth noting that the national average is heavily skewed by high-risk regions, particularly in Queensland and northern WA where cyclone, flood, and storm exposure push premiums into the thousands. For a Perth suburban homeowner, these headline figures can be alarming but aren't really your benchmark.

---

Property Features That Affect Your Premium

The specific characteristics of this property play a meaningful role in determining the premium. Here's how each feature influences the pricing:

Double Brick Construction Double brick is widely regarded as one of the most resilient building materials in the Australian residential market. It offers strong resistance to fire, wind, and general wear — all factors that reduce an insurer's risk exposure. Homes with double brick walls typically attract lower premiums than those with timber or lightweight cladding.

Tiled Roof Terracotta or concrete tiles are a standard roofing choice in Perth and are generally well-regarded by insurers. They're durable, fire-resistant, and hold up well in the mild-to-warm WA climate. This is a neutral-to-positive factor for pricing.

Slab Foundation A concrete slab foundation is the norm for homes built in the late 1990s across Perth's northern suburbs. It's structurally sound and doesn't carry the subsidence or termite risk associated with older timber subfloor construction.

Solar Panels This property has solar panels installed, which adds a modest amount to the insured value of the building. Solar systems can be damaged by hail, storms, or fire, and insurers factor in the replacement cost. It's worth confirming with your insurer that your solar system is explicitly covered under the building sum insured — not all policies include it by default.

Ducted Climate Control Ducted air conditioning is a significant fixture that contributes to the overall replacement cost of the home. At 214 sqm, this is a well-appointed family home, and the ducted system is one of several features that justify a building sum insured of $501,000.

Construction Year: 1998 At around 26 years old, this home is mature but not aged. It was built under modern building codes and with contemporary materials, which keeps risk relatively low. Homes of this era don't typically carry the elevated risk associated with pre-1970s construction.

---

Tips for Homeowners in Banksia Grove

1. Review your building sum insured annually Construction costs have risen sharply across Australia over the past few years. A sum insured of $501,000 may have been adequate when the policy was first taken out, but it's worth using a building cost calculator to verify it still reflects full replacement cost — not market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm your solar panels are covered As mentioned above, solar panels are sometimes treated as an optional add-on or excluded from standard building cover. Check your Product Disclosure Statement (PDS) carefully, and if in doubt, call your insurer to confirm the panels and inverter are included in your sum insured.

3. Shop around at renewal time A "FAIR" rating means there's a reasonable chance you could find a better deal with another provider. Loyalty doesn't always pay in insurance — many insurers offer their best rates to new customers. Set a reminder to compare quotes at least 30 days before your renewal date.

4. Consider your contents valuation A contents value of $50,000 is on the lower end for a four-bedroom family home. Take stock of your furniture, appliances, clothing, electronics, and valuables. It's easy to underestimate how quickly replacement costs add up. Many insurers offer online contents calculators to help you arrive at a more accurate figure.

---

Compare Your Options with CoverClub

Whether you're renewing soon or just curious about what else is available, it pays to see the full picture. CoverClub makes it easy to compare home and contents insurance quotes for properties in Banksia Grove and across Australia. Get a quote today and find out whether you could be paying less — or whether the cover you have is genuinely the right fit for your home.