If you own a four-bedroom free standing home in Banora Point, NSW 2486, you've probably wondered whether your home insurance premium is competitive — or whether you're quietly overpaying. Banora Point sits in the Tweed region of northern New South Wales, close to the Queensland border, and it's a suburb where insurance pricing can vary quite significantly depending on the specifics of your property. This article breaks down a real home and contents insurance quote for a brick veneer home in the area, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote we're analysing comes in at $4,489 per year (or $430/month) for combined home and contents cover, with a building sum insured of $950,000 and contents valued at $220,000. Both the building and contents excess are set at $5,000.

Our price rating for this quote is FAIR — Around Average, which means it's sitting in a reasonable position relative to what other homeowners in Banora Point are paying, but there's still room to potentially do better.

To put that in context: the suburb's median premium is $4,189 per year, meaning this quote is only about $300 above the midpoint for the area. It falls comfortably within the interquartile range (between the 25th percentile of $3,531 and the 75th percentile of $5,997), which tells us it's not an outlier in either direction. It's a reasonable quote — but not the sharpest price available in the suburb.

---

How Banora Point Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful things you can do as a homeowner. Here's how the numbers stack up:

| Benchmark | Premium |

|---|---|

| This Quote | $4,489/yr |

| Banora Point Suburb Average | $5,083/yr |

| Banora Point Suburb Median | $4,189/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Tweed LGA Average | $26,089/yr |

(Based on [Banora Point suburb insurance data](https://coverclub.com.au/stats/NSW/2486/banora-point) from 27 quotes, [NSW state data](https://coverclub.com.au/stats/NSW), and [national benchmarks](https://coverclub.com.au/stats/national).)

A few things stand out here. First, the NSW state average of $9,528 is dramatically higher than this quote — but that figure is heavily skewed by high-risk coastal and flood-prone areas across the state, which is why the median of $3,770 is a more representative comparison point. This quote sits slightly above the NSW median, which is consistent with a "fair" rating.

The Tweed LGA average of $26,089 is an eye-catching number. This is almost certainly driven by cyclone-rated and flood-risk properties elsewhere in the Tweed region, which push the LGA average well above what a standard Banora Point home would attract. Since this property is not in a cyclone risk area, it avoids the significant loading that affects many properties in the broader Tweed region.

Against the national average of $5,347, this quote is actually slightly below — another positive sign. The national median of $2,764 is lower, but that includes many lower-value properties and lower-risk regions that aren't really comparable to a 235 sqm home in coastal northern NSW.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding them helps you appreciate why your premium lands where it does.

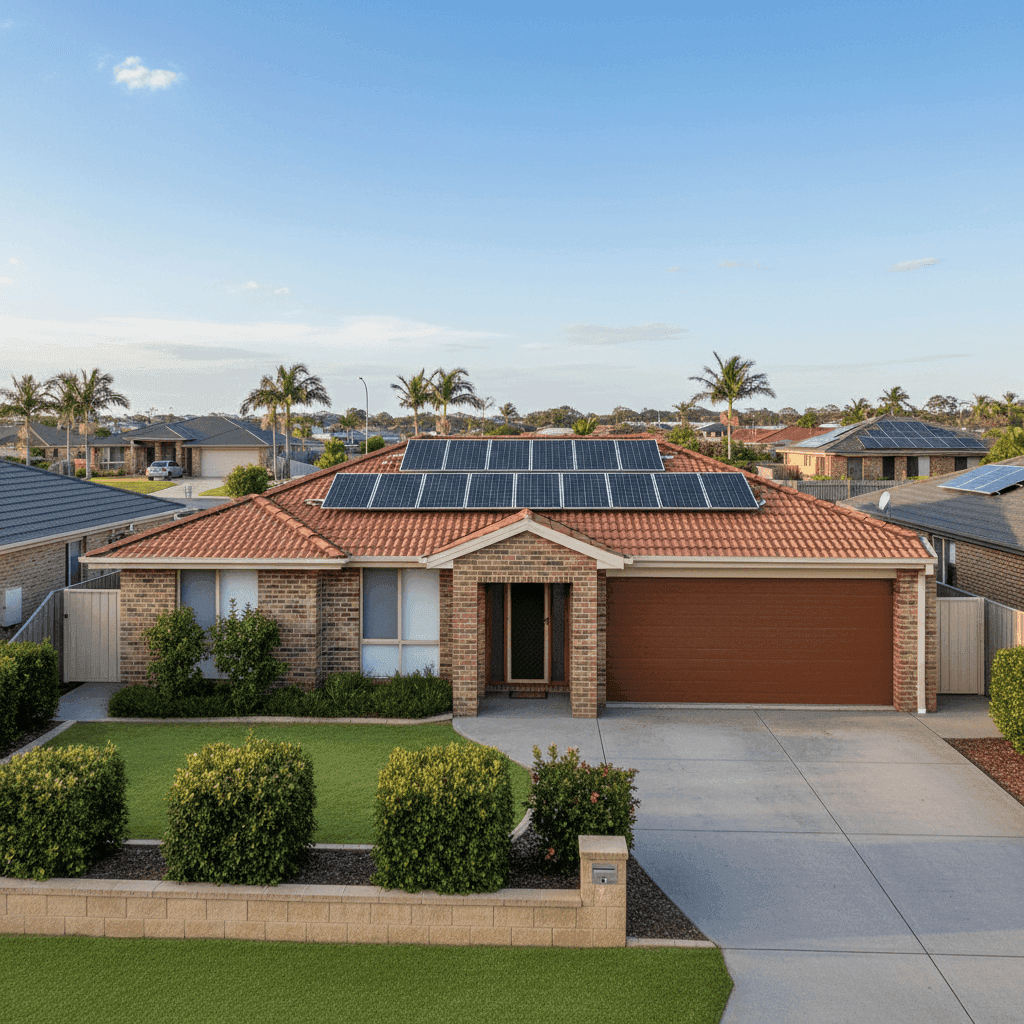

Brick veneer construction and tiled roof are generally viewed favourably by insurers. Brick veneer walls offer solid fire resistance and durability, while a tiled roof is considered lower risk than corrugated iron or colorbond in many scenarios. These two features likely help keep this premium competitive.

Slab foundation is standard in this region and doesn't typically attract any loading — unlike homes on stumps or piers, which can be more expensive to repair after events like flooding or subsidence.

Construction year of 1981 means this home is over 40 years old. Older homes can attract slightly higher premiums due to the age of electrical wiring, plumbing, and roofing materials, even when they're well-maintained. Insurers factor in the likelihood of wear-related claims.

Solar panels are an increasingly common feature and one that insurers are paying more attention to. They add to the replacement value of the home and can affect claims if damaged by storm or hail. It's important to confirm with your insurer that your solar system is explicitly covered under your building policy.

Ducted climate control adds to the overall value of the home's fixtures and fittings, which is reflected in the building sum insured. At $950,000, the sum insured is substantial — and getting this figure right is critical. Underinsurance is one of the most common and costly mistakes homeowners make.

Standard fittings quality means there are no high-end finishes or bespoke features that would push rebuild costs — and therefore the sum insured — significantly higher. This helps keep the premium grounded.

---

Tips for Homeowners in Banora Point

1. Review your sum insured annually Building costs in NSW have risen sharply over recent years. A sum insured of $950,000 for a 235 sqm home may be appropriate today, but it's worth recalculating your estimated rebuild cost each year — especially given the age of this property and the cost of materials in the Tweed region. Many insurers offer a building cost calculator to help.

2. Check your solar panels are covered Not all policies automatically extend full cover to rooftop solar systems. Ask your insurer specifically whether your panels, inverter, and mounting hardware are covered for storm, hail, and accidental damage — and whether there are any sub-limits that apply.

3. Consider whether your excess is working for you Both the building and contents excess on this quote are set at $5,000. A higher excess generally reduces your premium, but it also means a larger out-of-pocket cost when you do make a claim. If cash flow is a consideration, it's worth modelling what a lower excess (say, $1,000 or $2,500) would cost in additional premium versus the financial exposure you'd carry.

4. Compare quotes before renewal The "fair" price rating on this quote means there's a reasonable chance a more competitive option exists. With 27 quotes sampled in the Banora Point area showing a range from $3,531 at the 25th percentile to $5,997 at the 75th, the spread is wide — and shopping around could realistically save you several hundred dollars a year.

---

Get a Better Deal on Your Home Insurance

Whether you're renewing an existing policy or insuring a new property, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up and find competitive options tailored to your property.