Bardon is one of Brisbane's most characterful inner-western suburbs — a leafy hillside pocket of Queensland known for its Federation and post-war homes, tree-lined streets, and proximity to the CBD. If you own a free standing home here, you're sitting on a genuinely desirable slice of real estate. But what should you expect to pay for home and contents insurance? This article breaks down a real quote for a 3-bedroom, 2-bathroom property in Bardon (QLD 4065), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $893 per year (or roughly $86 per month) for combined home and contents cover, with a building sum insured of $417,000 and contents valued at $75,000. The building excess sits at $2,000, with a separate $600 excess for contents claims.

Our price rating for this quote? Cheap — well below average.

To put that in perspective: the average home and contents premium across Bardon sits at $4,887 per year, with a median of $3,754. That means this quote is coming in at roughly 18% of the suburb average — an extraordinary result by any measure. Even against the 25th percentile (the cheapest quarter of quotes in the area), which sits at $2,421, this premium is still less than half.

So yes — this is an exceptionally competitive quote. Whether that reflects the specific insurer's appetite for this type of property, the building characteristics, or a combination of factors, it's well worth taking seriously.

---

How Bardon Compares

Home insurance in Bardon is notably more expensive than the national average, which is an important reality check for local homeowners. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bardon (QLD 4065) | $4,887/yr | $3,754/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

| Brisbane LGA | $16,277/yr | — |

You can explore the full data on the Bardon suburb stats page, the Queensland state overview, or the national insurance stats.

A few things stand out here. First, Bardon's average premium closely tracks the broader Queensland average — suggesting that the suburb's risk profile is broadly in line with the rest of the state. Second, both figures are significantly higher than the national average, which reflects Queensland's elevated exposure to weather-related events including storms, flooding, and hail. Third, the Brisbane LGA average of $16,277 is extraordinarily high — likely skewed by a small number of very high-risk or high-value properties — and shouldn't be taken as representative of what most Brisbane homeowners pay.

The wide spread between Bardon's 25th percentile ($2,421) and 75th percentile ($6,922) also tells an important story: premiums in this suburb vary enormously depending on the property, insurer, and level of cover. Shopping around genuinely matters here.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth unpacking, as they each play a role in how insurers price the risk.

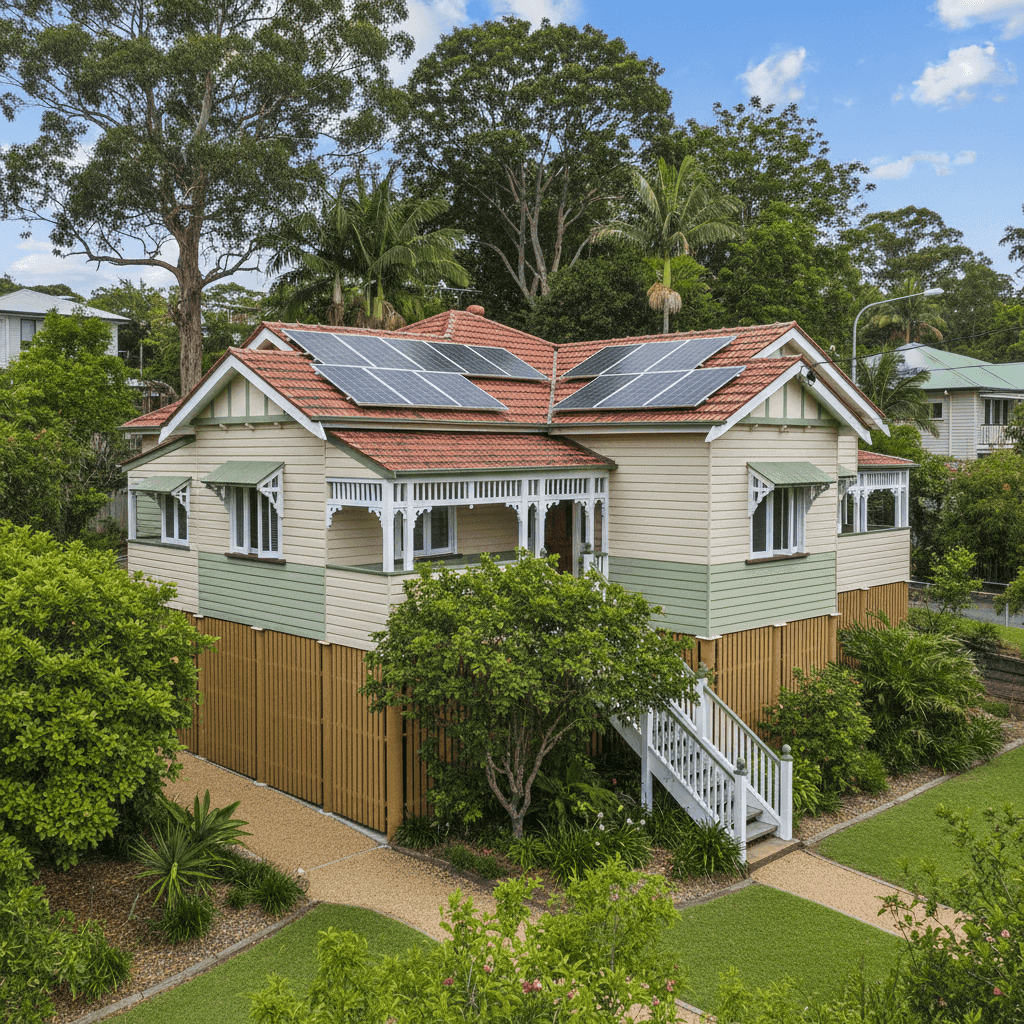

Weatherboard timber construction (1960): Older weatherboard homes are among the most common dwelling types in inner Brisbane, but they do attract attention from insurers. Timber is more susceptible to fire, termite damage, and general wear than brick veneer or double brick construction. A home built in 1960 is now over 60 years old, which means wiring, plumbing, and structural elements may be ageing — factors that can push premiums higher. That this quote remains so low despite these characteristics is notable.

Timber stumps foundation: Homes on stumps (also called pier-and-beam foundations) are very typical in Queensland, particularly in hilly suburbs like Bardon. This style of construction offers good ventilation and flexibility on sloped blocks, but can be vulnerable to subsidence, termite activity, and storm-related movement. Insurers factor this in.

Tiled roof: Terracotta or concrete tiles are generally viewed favourably by insurers compared to older materials like asbestos sheeting or corrugated iron. Tiles offer solid weather resistance, though they can be damaged in severe hailstorms.

Solar panels: The presence of rooftop solar adds replacement value to the property. It's worth confirming with your insurer that solar panels are explicitly covered under your building sum insured, as some policies treat them as an optional inclusion.

Ducted climate control: Ducted air conditioning is a significant fixed asset and should be captured in your building sum insured. At $417,000, the building cover here appears reasonable for a 139 sqm home in this suburb, but it's always worth reviewing rebuild cost estimates periodically — particularly given construction cost inflation in recent years.

No pool, no cyclone risk zone: The absence of a pool removes one common source of liability and premium loading. And while Queensland is no stranger to severe weather, Bardon falls outside designated cyclone risk areas, which keeps that particular loading off the table.

---

Tips for Homeowners in Bardon

1. Review your sum insured regularly. Construction costs have risen sharply across Australia over the past few years. A building sum insured that was accurate two or three years ago may now be insufficient to cover a full rebuild. Use a professional quantity surveyor or your insurer's rebuild cost calculator to sense-check your coverage — underinsurance is a real and common risk.

2. Confirm solar panels are covered. If your policy doesn't explicitly list solar panels as a covered item under building insurance, you may face a gap at claim time. Check your Product Disclosure Statement (PDS) carefully and contact your insurer if you're unsure.

3. Shop around — the spread in Bardon is enormous. With premiums ranging from around $2,400 to nearly $7,000 across the suburb, the difference between the cheapest and most expensive quotes is staggering. Don't auto-renew without comparing. Get a quote through CoverClub to see how your current premium stacks up.

4. Consider your excess settings strategically. This quote carries a $2,000 building excess — higher than many standard policies. A higher excess typically lowers your premium, which can be a smart trade-off if you have the financial buffer to cover it in a claim scenario. Just make sure the excess level is genuinely manageable for your household.

---

Compare Your Home Insurance Today

Whether you're a long-time Bardon resident or you've recently purchased in the suburb, it pays to know what the market looks like. The quote analysed here is a strong result — but every property is different, and the right cover for your home depends on your specific circumstances. Visit CoverClub to compare home and contents quotes tailored to your property, and make sure you're not leaving money on the table at renewal time.