If you own a free standing home in Barham, NSW 2732, you might be wondering whether you're paying a fair price for home and contents insurance — or leaving money on the table. Barham is a quiet riverside town in the Murray River region of southern New South Wales, and like many rural communities, insurance costs here can vary dramatically depending on your property's features, insurer, and level of cover. This article breaks down a real insurance quote for a 3-bedroom, 2-bathroom home in Barham to help you understand what's reasonable, what's not, and how to make the most of your policy.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote came in at $2,110 per year (or around $202 per month) for combined home and contents cover, with a building sum insured of $689,000 and $50,000 in contents cover. Both the building and contents excess sit at $2,000.

Based on CoverClub's pricing data, this quote is rated CHEAP — below average for the area. That's a meaningful distinction. With a suburb average of $4,581/yr and a suburb median of $3,083/yr, this quote sits well below even the 25th percentile of $2,593/yr for Barham. In plain terms, roughly three-quarters of comparable quotes in this suburb cost more than this one.

For a property with a granny flat, solar panels, and ducted climate control — all features that can push premiums upward — landing a quote this competitive is a solid outcome. It suggests the insurer has assessed the property's risk profile favourably, likely influenced by its brick veneer construction, Colorbond roof, and slab foundation, all of which are considered durable and low-maintenance by underwriters.

---

How Barham Compares

Understanding where Barham sits in the broader insurance landscape adds important context. You can explore the full data on the Barham suburb insurance stats page.

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,110 |

| Barham suburb average | $4,581 |

| Barham suburb median | $3,083 |

| Barham 25th percentile | $2,593 |

| Barham 75th percentile | $6,106 |

| NSW state average | $9,528 |

| NSW state median | $3,770 |

| National average | $5,347 |

| National median | $2,764 |

| Murray River LGA average | $24,396 |

A few things stand out here. First, the Murray River LGA average of $24,396/yr is extraordinarily high — likely skewed by high-value rural and farming properties, which can carry significant structures, machinery, and flood-related risk. This makes Barham township properties look very affordable by comparison.

Second, the NSW state average of $9,528/yr is heavily influenced by Sydney and coastal markets where property values and natural hazard risks (particularly storm and flooding) drive premiums up sharply. Barham's more modest property values and relatively stable risk environment help keep costs grounded. Check out NSW-wide insurance statistics and national benchmarks for a broader picture.

It's also worth noting that the suburb sample size here is 13 quotes — a relatively small dataset — so averages can shift as more data comes in. That said, the trend is clear: this quote represents genuine value.

---

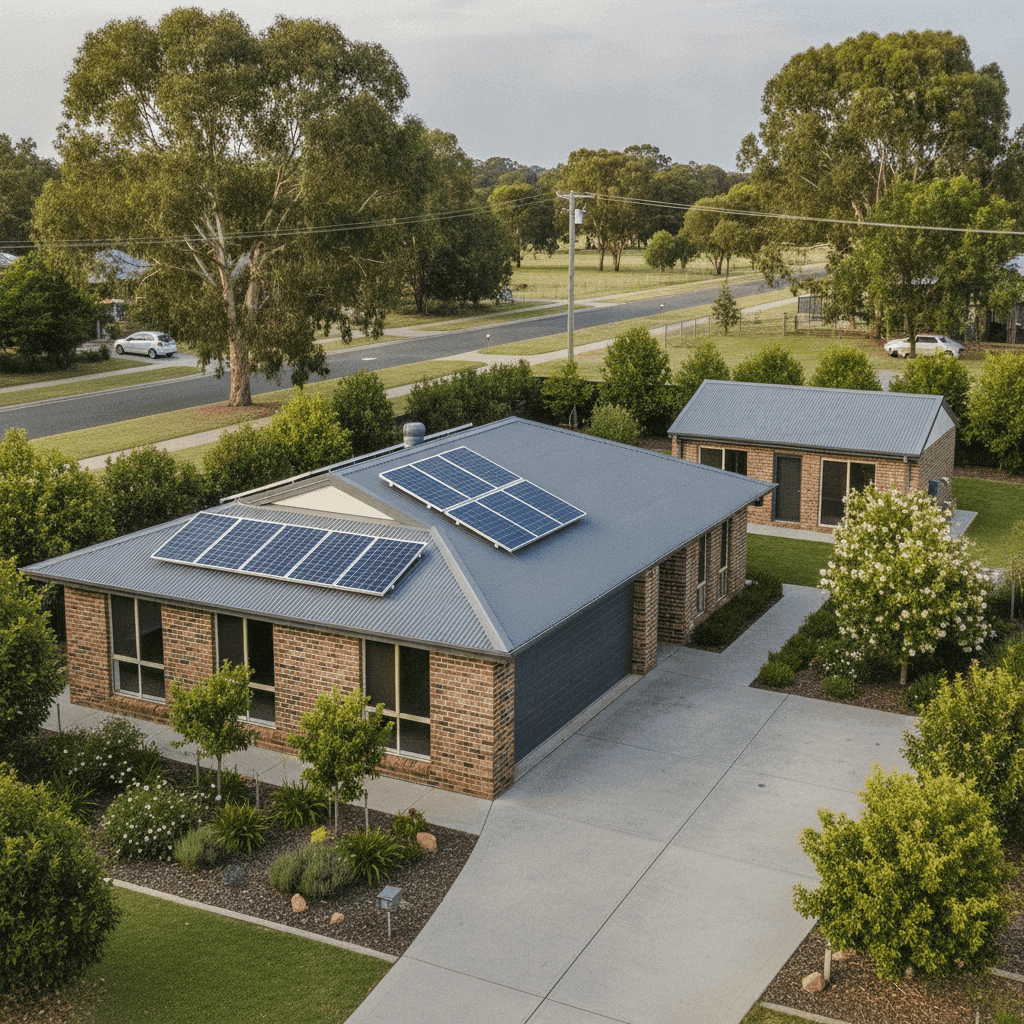

Property Features That Affect Your Premium

Several characteristics of this property directly influence how insurers price the risk.

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the most common — and insurer-friendly — external wall types in Australia. It offers solid fire resistance and durability. Paired with a steel Colorbond roof, which handles heat, rain, and wind well, this combination signals a well-built, low-maintenance property to underwriters.

Slab Foundation Concrete slab foundations are generally viewed as stable and less susceptible to subsidence or pest damage compared to older timber subfloor systems. This can contribute to a lower risk assessment.

Timber and Laminate Flooring While aesthetically appealing, timber and laminate floors can be more costly to replace after water damage than tiles. Insurers may factor this into contents or building assessments, though the impact is typically modest.

Solar Panels This property has solar panels, which adds some replacement cost to the building sum insured. Solar systems can be damaged by hail, storms, or fire, and their inclusion in a building policy is worth confirming explicitly with your insurer to ensure they're adequately covered.

Ducted Climate Control Ducted air conditioning systems are expensive to repair or replace and are typically covered under the building policy. Their presence can slightly increase the building sum insured, which may nudge premiums upward — though the effect here appears to have been well-managed.

Granny Flat The presence of a granny flat is a notable factor. Secondary dwellings add to the total replacement cost of the property and introduce additional liability considerations. Ensuring the granny flat is explicitly included in the building sum insured of $689,000 is critical — underinsurance is a real risk if the flat isn't accounted for.

No Pool, No Cyclone Risk The absence of a pool removes a common liability risk, and Barham's location outside cyclone-prone zones means the property avoids the significant premium loadings that apply in northern Queensland and parts of WA.

---

Tips for Homeowners in Barham

1. Double-check your building sum insured includes the granny flat With a secondary dwelling on the property, your $689,000 sum insured needs to cover the full cost of rebuilding both structures, including site clearance, professional fees, and current construction costs. Use a quantity surveyor or an online building calculator to verify this figure annually, as construction costs have risen sharply in recent years.

2. Confirm your solar panels are covered Ask your insurer directly whether your solar panel system is included under the building policy and up to what value. Some policies cap solar coverage or require it to be listed as a separate item. Given the cost of modern solar systems, this is worth clarifying before you need to make a claim.

3. Review your contents sum insured $50,000 in contents cover is on the modest side for a 3-bedroom, 2-bathroom home — particularly one with a granny flat that may contain additional furnishings. Walk through each room and estimate the replacement value (not second-hand value) of your belongings. Many Australians are significantly underinsured on contents.

4. Compare quotes at renewal time Even a competitive quote like this one can be beaten at renewal. Insurers often apply automatic premium increases each year, and loyalty doesn't always pay off. Set a reminder to compare at least 30 days before your renewal date to give yourself time to switch if a better deal is available.

---

Ready to Compare Home Insurance in Barham?

Whether you're a first-time buyer or a long-term homeowner, getting a second opinion on your insurance costs is always worth the effort. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property's specific features and location. Get a quote today and see how your current premium stacks up against the market.