Barmaryee is a quiet residential locality on Queensland's Capricorn Coast, sitting just inland from the popular beaches of Yeppoon. It's an area that attracts families and lifestyle seekers alike, drawn by the space, the climate, and the relative affordability compared to major southeast Queensland centres. For owners of a substantial free standing home in this postcode, understanding what drives your insurance premium — and whether you're paying a fair price — is well worth the effort.

This article breaks down a recent home and contents insurance quote for a six-bedroom, three-bathroom free standing home in Barmaryee (QLD 4703), covering a building sum insured of $1,419,900 and contents valued at $193,700, with an annual premium of $4,596 (or $434/month).

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated Fair (Around Average), which means it sits in a reasonable range relative to what other homeowners in Queensland are paying for comparable cover.

To put it in perspective, the Queensland state average premium sits at $4,547 per year, with a median of $3,931. The quote in question — at $4,596 — lands just $49 above the state average, which is a negligible difference given the size and value of this property. For a six-bedroom home with above-average fittings, a pool, solar panels, and a building sum insured approaching $1.42 million, this is a reasonably competitive result.

It's worth noting that "fair" doesn't necessarily mean "the best available." Insurance pricing varies considerably between providers, and even a modest improvement in the premium could save hundreds of dollars annually on a policy of this size.

---

How Barmaryee Compares

Comparing this quote against available benchmarks reveals some interesting context. Unfortunately, no suburb-level aggregate data is currently available specifically for Barmaryee — you can check for updates at the Barmaryee suburb stats page as more data becomes available.

What we do have paints a clear picture at a broader level:

| Benchmark | Premium |

|---|---|

| This Quote | $4,596/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

| Livingstone LGA Average | $13,146/yr |

A few things stand out here. First, this quote is dramatically lower than the Livingstone LGA average of $13,146 per year — less than a third of that figure. The LGA average is likely skewed upward by higher-risk properties, coastal exposure, and potentially larger or older homes in the broader Livingstone council area. If your neighbours are paying closer to the LGA average, this quote represents genuinely strong value.

Second, the gap against national benchmarks is significant — the national average sits at $2,965 and the median at $2,716. However, Queensland homeowners consistently pay more than the national average due to the state's elevated exposure to natural hazards including storms, flooding, and cyclone risk in certain regions. This premium uplift is a structural feature of the Queensland insurance market rather than a reflection of any individual insurer's pricing.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on how insurers price the risk. Understanding these can help you have more informed conversations with insurers and identify where you may have room to negotiate or adjust your cover.

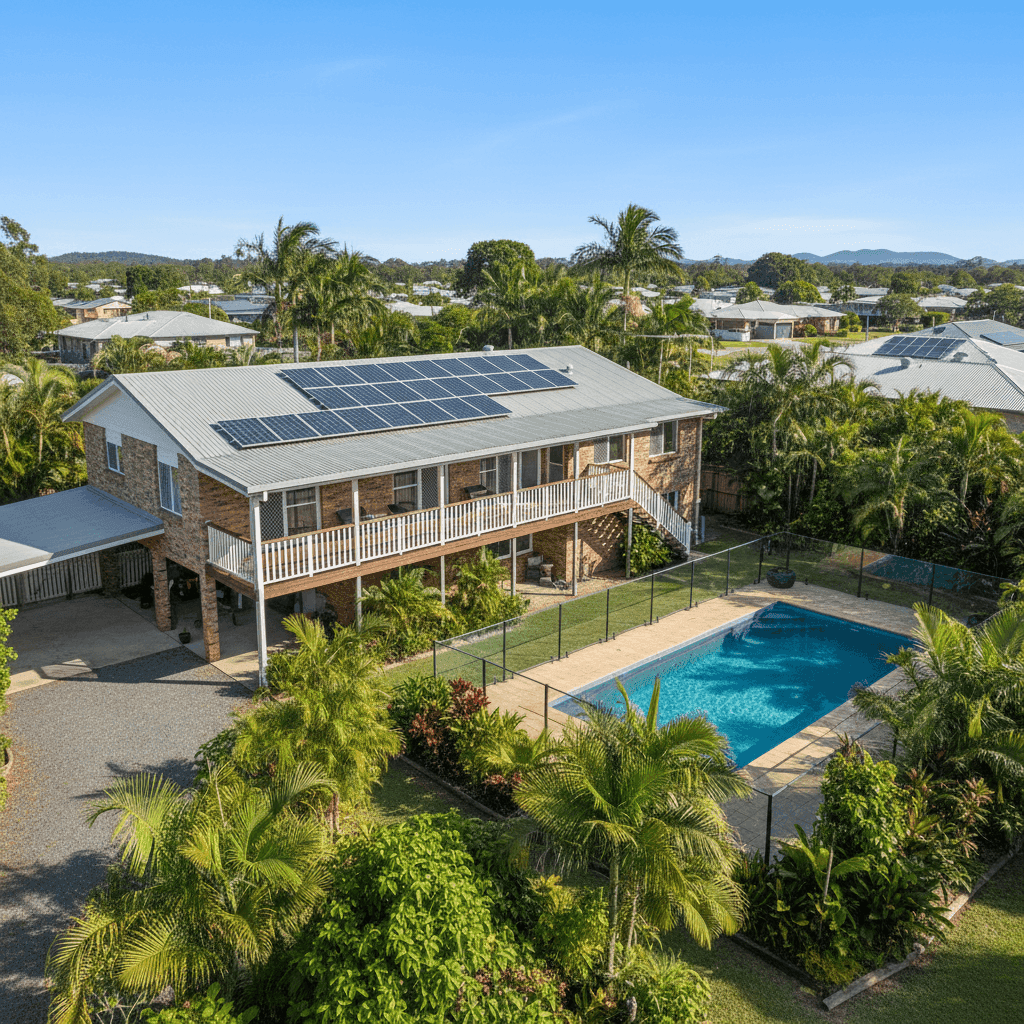

Size and value of the home A six-bedroom, three-bathroom home with above-average fittings commands a high building sum insured of $1,419,900. Larger homes cost more to rebuild, and premium-quality fixtures, fittings, and finishes add to that replacement cost. This is one of the most significant drivers of the premium.

Brick veneer construction with Colorbond roofing Brick veneer walls are generally viewed favourably by insurers — they offer solid fire resistance and structural durability. A steel Colorbond roof is similarly well-regarded for its longevity and resistance to ember attack, which is a meaningful consideration in regional Queensland. This combination tends to attract more competitive premiums than timber-framed or fibre cement alternatives.

Elevated on stumps The home sits elevated on stumps (less than 1 metre), a construction style common in Queensland. Stump foundations can improve airflow and help with moisture management, but insurers assess them carefully for flood and storm surge vulnerability. Being elevated under 1 metre means the home isn't classified as a high-set Queenslander, but the foundation type is still factored into the risk profile.

Timber and laminate flooring Timber and laminate floors are susceptible to water damage, which can be costly to repair or replace following a storm or flood event. This is a consideration in the contents and building assessment, particularly given Queensland's storm season.

Swimming pool A pool adds to the insurable value of the property and introduces some liability considerations. It's included in the building sum insured and contributes to the overall premium.

Solar panels Solar panels are increasingly common on Queensland homes and are typically covered under building insurance. They represent a meaningful replacement cost — a full rooftop system can cost $10,000–$20,000 or more to replace — so confirming they're adequately covered in your policy is important.

---

Tips for Homeowners in Barmaryee

1. Review your sum insured regularly Construction costs in regional Queensland have risen sharply in recent years. If your building sum insured hasn't been reviewed since you first took out the policy, there's a real risk of being underinsured. Use a building cost calculator or speak with a quantity surveyor to ensure $1,419,900 still reflects the true cost of rebuilding your home from scratch — including demolition, debris removal, and professional fees.

2. Compare quotes before renewal A "fair" rating means this quote is competitive, but it doesn't mean it's the cheapest available. Insurance markets shift year to year, and loyalty rarely pays off. Use a comparison platform like CoverClub to run multiple quotes side by side before your renewal date — even saving 10–15% on a $4,596 premium is worth $460–$690 back in your pocket annually.

3. Check your pool and solar panel coverage specifics Not all policies treat pools and solar panels the same way. Some policies cover solar panels only as a fixed structure (not for mechanical or electrical breakdown), and pool cover may exclude certain types of damage. Read the Product Disclosure Statement carefully and ask your insurer to confirm what's included.

4. Understand your excess structure This policy carries a $1,000 building excess and a $500 contents excess. Opting for a higher voluntary excess can reduce your premium, but make sure the saving is meaningful and that you'd genuinely be able to cover that excess out of pocket if you needed to make a claim. For a home of this value, the existing excess levels are fairly standard.

---

Ready to Find a Better Deal?

Whether you're renewing soon or just curious about what else is on the market, comparing quotes is the single most effective way to ensure you're not overpaying. Head to CoverClub to get a personalised home and contents insurance quote for your Barmaryee property — it takes just a few minutes and could save you hundreds.