If you own a free standing home in Baynton, WA 6714, you already know that insuring a property in the Pilbara comes with its own set of challenges — and costs. This article breaks down a recent building insurance quote for a four-bedroom, two-bathroom home in the suburb, examines how it stacks up against local, state, and national benchmarks, and offers practical guidance for homeowners looking to get the best value from their cover.

---

Is This Quote Fair?

The quote in question is $8,246 per year (or $790/month) for building-only cover, with a sum insured of $1,500,000 and a building excess of $5,000.

Our price rating for this quote is EXPENSIVE — Above Average.

To put that in context, the suburb average premium in Baynton sits at $7,660/year, with a median of $7,179/year. This quote lands above both figures, and also exceeds the suburb's 75th percentile of $7,840/year — meaning it's pricier than at least three-quarters of comparable quotes in the area. That's a meaningful gap, and worth investigating before renewing or accepting this premium as the norm.

That said, it's important to acknowledge that Baynton is not a typical Australian suburb. Situated within the City of Karratha in Western Australia's northwest, it sits in a cyclone risk zone, which fundamentally drives up the cost of building insurance across the entire region. The LGA (Karratha) average premium of $10,438/year actually makes this quote look relatively competitive when viewed through a regional lens — it's roughly $2,200 below the LGA average.

So while the quote is above the suburb average, it's well below what many homeowners in the broader Karratha area are paying. The "expensive" rating reflects its position relative to Baynton specifically, not the wider region.

---

How Baynton Compares

Understanding how Baynton premiums sit relative to broader benchmarks is essential context for any homeowner. Here's a clear picture:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $8,246 |

| Baynton Suburb Average | $7,660 |

| Baynton Suburb Median | $7,179 |

| Baynton 25th Percentile | $6,116 |

| Baynton 75th Percentile | $7,840 |

| WA State Average | $2,811 |

| WA State Median | $2,127 |

| National Average | $5,347 |

| National Median | $2,764 |

| Karratha LGA Average | $10,438 |

The contrast between Baynton and the broader WA state average ($2,811/year) is striking. This quote is nearly three times the state average — a stark reminder of just how significantly cyclone exposure inflates insurance costs in northwest WA. Even compared to the national average of $5,347/year, this premium is elevated.

You can explore the full breakdown of Baynton insurance statistics here, or compare against all of WA's home insurance data to see how your suburb sits within the state picture.

It's worth noting that the suburb sample size is 11 quotes, which is relatively small. As more data is collected, these averages may shift — so checking back periodically is worthwhile.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Understanding them helps you make sense of the number on your renewal notice.

Cyclone Risk Zone

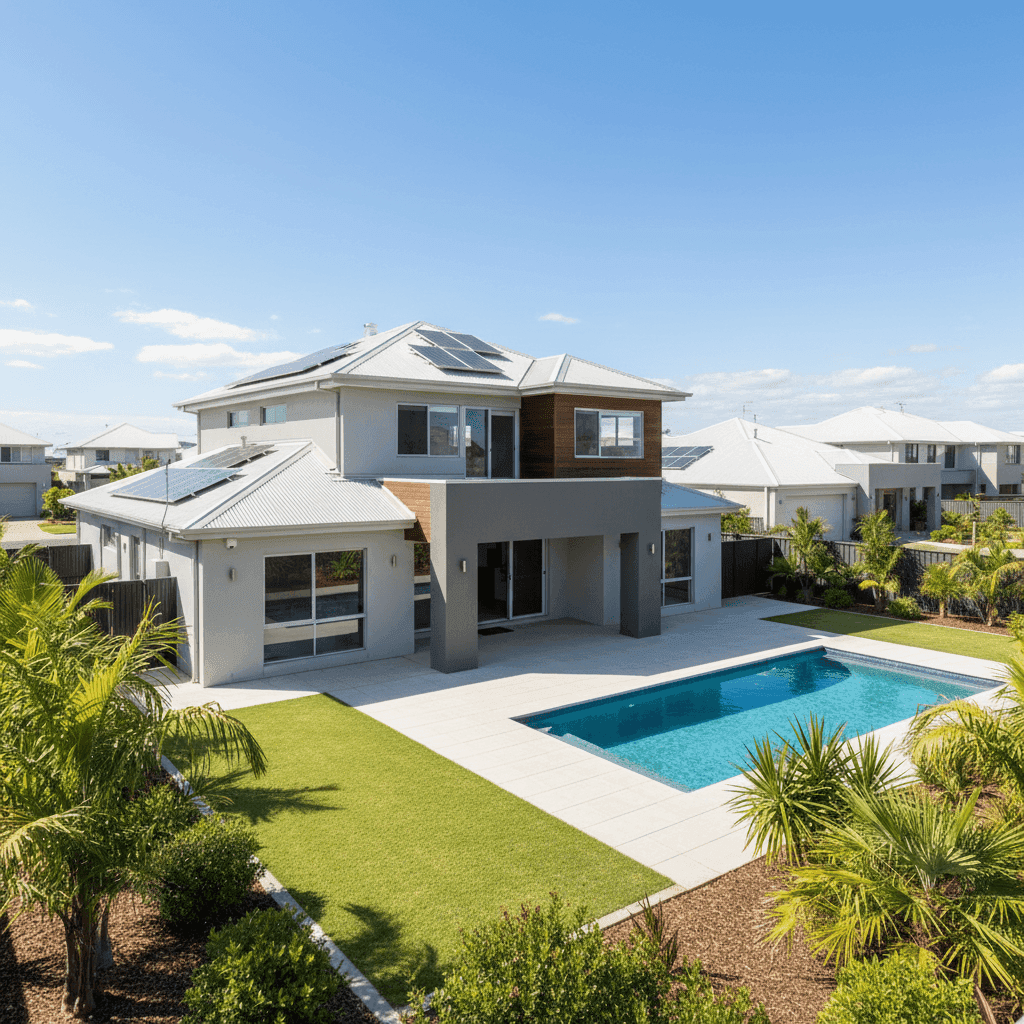

This is the single biggest factor. Baynton falls within a designated cyclone risk area, and insurers price that exposure heavily. Cyclone-rated construction requirements, the potential for wind-driven rain damage, and the sheer cost of rebuilding in a remote location all feed into the premium calculation.

Steel/Colorbond Roof

A Colorbond roof is generally viewed favourably by insurers — it's durable, fire-resistant, and performs well in high-wind events. Compared to tiled roofs, Colorbond can sometimes attract a marginally lower premium, though in a cyclone zone, the overall risk profile still dominates the pricing.

Slab Foundation

A concrete slab foundation is considered a stable and low-risk construction method by most insurers. It reduces the risk of subsidence and pest damage compared to raised timber floors, which can work in the homeowner's favour.

Swimming Pool

The presence of a pool adds to the insured value of the property and introduces additional liability considerations. Pools require specific mention in your policy, and any associated structures (fencing, pumps, surrounds) should be confirmed as covered under your building sum insured.

Solar Panels

Solar panels are typically covered under building insurance as a fixed structure, but it's crucial to confirm this with your insurer. With a 214 sqm home and a full solar system installed, ensuring the panels are adequately included in the $1,500,000 sum insured is important — especially given replacement costs in a remote area can be significantly higher than in metro locations.

Ducted Climate Control

Ducted air conditioning systems are a fixed building fixture and should be covered under building insurance. In the Pilbara's extreme heat, these systems are essential — and their replacement cost in a remote area can be substantial. Make sure your sum insured accounts for this.

Building Size & Age

At 214 sqm and constructed in 2011, this is a modern, mid-sized home. Newer builds tend to attract more straightforward claims assessments, and construction to post-2006 cyclone standards in WA generally means the home meets current wind-resistance requirements — a factor some insurers consider when pricing risk.

---

Tips for Homeowners in Baynton

1. Shop around — even in a high-risk zone The gap between the 25th percentile ($6,116/year) and this quote ($8,246/year) in Baynton alone is over $2,100 annually. That's real money. Insurers price cyclone risk differently, and comparing multiple quotes is one of the most effective ways to reduce your premium without reducing your cover. Get a comparison quote at CoverClub to see what other insurers are offering.

2. Review your sum insured carefully A sum insured of $1,500,000 on a 214 sqm home in a remote area may be appropriate — rebuilding costs in the Pilbara are significantly higher than in Perth or other metro areas due to labour and material transport costs. However, it's worth getting a professional building replacement cost estimate to ensure you're neither underinsured nor paying premiums on an inflated figure.

3. Ask about cyclone mitigation discounts Some insurers offer premium reductions for homes that have undergone cyclone-proofing improvements — such as upgraded roof tie-downs, storm shutters, or reinforced garage doors. If you've made any such improvements since the home was built, it's worth raising this with your insurer.

4. Consider your excess strategically This policy carries a $5,000 building excess. A higher excess typically reduces your annual premium. If you have the financial capacity to absorb a larger out-of-pocket cost in a claim scenario, exploring a higher excess tier could bring your premium down meaningfully — particularly useful in a high-premium area like Baynton.

---

Compare Your Home Insurance Today

Whether you're renewing your current policy or shopping for the first time, the best way to know if you're getting a fair deal is to compare. CoverClub makes it easy to see how your premium stacks up and find competitive quotes from a range of insurers. Enter your address at CoverClub to get started — it only takes a few minutes, and the savings could be significant.