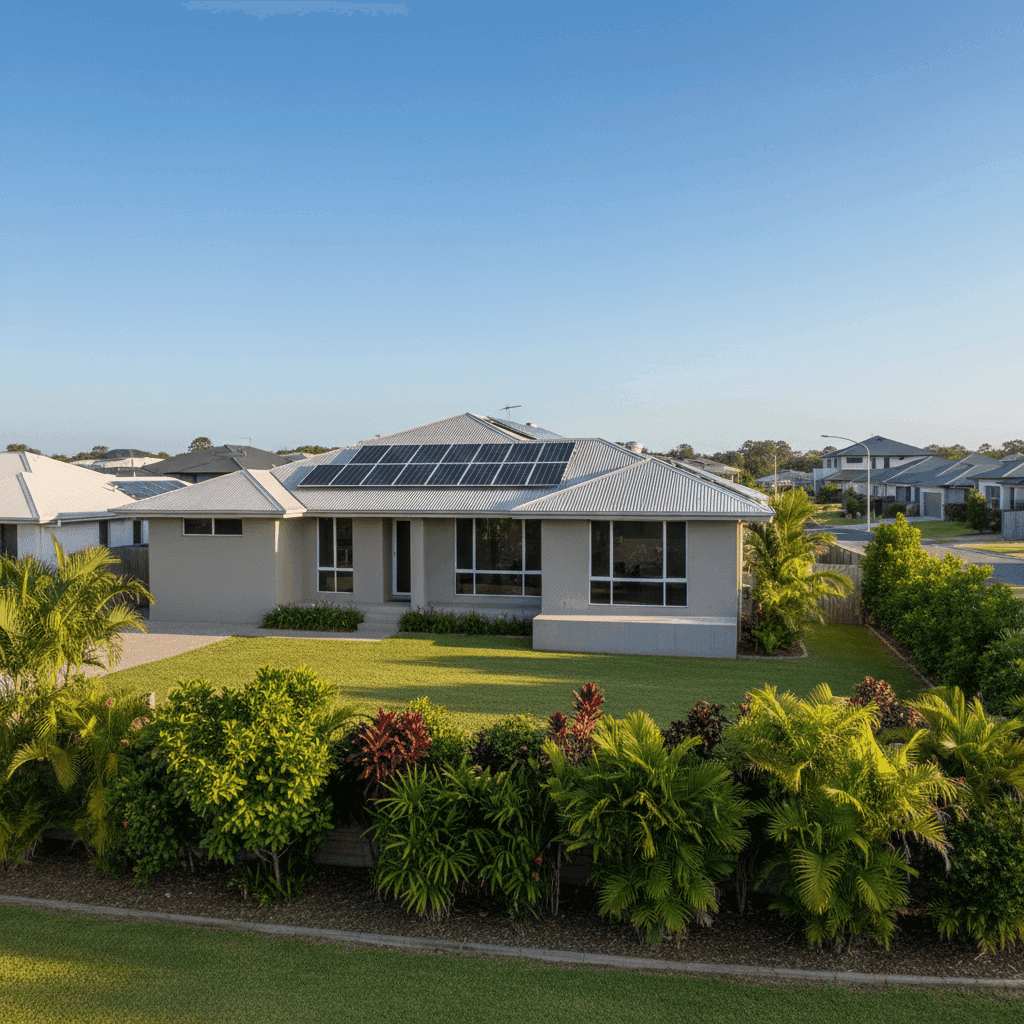

If you own a free standing home in Beaconsfield, QLD 4740, you already know that insuring a property in this part of Queensland comes with some unique considerations. From the region's tropical climate to the ever-present threat of cyclones, home insurance in the Mackay area is rarely straightforward — and the premiums reflect that. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom property in Beaconsfield, comparing it against suburb, state, and national benchmarks to help you understand what you're paying for and whether there's room to do better.

---

Is This Quote Fair?

The quote in question comes to $6,787 per year (or $650/month) for combined home and contents cover, with a building sum insured of $637,000 and contents valued at $85,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up. At $6,787 annually, this premium sits well above the suburb median of $4,094/yr, placing it closer to the 75th percentile ($4,805/yr) and beyond. It also exceeds the Queensland state median of $3,903/yr and the national median of $2,764/yr.

That said, "expensive" doesn't necessarily mean "wrong." A newly built home (2025 construction) with above-average fittings, a larger-than-average footprint at 214 sqm, and solar panels will naturally attract a higher replacement cost — and insurers price accordingly. The $637,000 building sum insured is substantial and reflects the quality and scale of the build. What matters most is whether the cover is appropriate, not just whether it's cheap.

---

How Beaconsfield Compares

To put this quote in context, here's how the premium stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $6,787/yr |

| Beaconsfield Suburb Median | $4,094/yr |

| Beaconsfield Suburb Average | $30,644/yr |

| Beaconsfield 25th Percentile | $3,177/yr |

| Beaconsfield 75th Percentile | $4,805/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| LGA (Mackay) Average | $8,458/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the suburb average of $30,644 is extraordinarily high — a figure likely skewed by a small sample size of just 27 quotes and potentially some very high-value or high-risk properties in the mix. The median of $4,094 is a far more reliable indicator of what most Beaconsfield homeowners are paying.

At $6,787, this quote is above the suburb median but sits well below the LGA (Mackay) average of $8,458 and the QLD state average of $9,129. From that angle, it's not as alarming as it first appears. You can explore the full Beaconsfield suburb insurance data to see how other properties in the area are rated.

The gap between Queensland and national medians is also telling. QLD homeowners consistently pay more than their interstate counterparts, largely due to the state's exposure to cyclones, flooding, and severe storms — risks that are very real in the Mackay region.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding them can help you have more informed conversations when shopping for cover.

Cyclone Risk Zone

This is arguably the single biggest premium driver. Beaconsfield falls within a cyclone risk area, and insurers apply significant loadings to properties in these zones. The Mackay region has a well-documented history of cyclone activity, and rebuilding costs after a major event are substantial. Expect this factor alone to add hundreds — if not thousands — of dollars to your annual premium compared to a similar property in southern Queensland.

New Construction (2025 Build)

Newly built homes are generally viewed favourably by insurers. Modern building codes in Queensland require cyclone-rated construction standards, which can reduce the likelihood of catastrophic damage. However, a brand-new home also means a higher replacement value, which pushes the sum insured — and therefore the premium — upward.

Concrete Walls & Colorbond Roof

Concrete external walls are among the most resilient building materials available, offering strong resistance to wind, fire, and impact. Combined with a steel/Colorbond roof (which performs well in high-wind environments when properly installed), this construction profile is well-suited to the local climate and may attract more competitive rates than a timber-framed equivalent.

Slab Foundation & Vinyl Flooring

A concrete slab foundation is standard for modern Queensland homes and is generally considered low-risk by insurers. Vinyl flooring is durable, water-resistant, and relatively affordable to replace — all positives from an underwriting perspective.

Solar Panels

Solar panels add replacement value to the property and must be adequately covered under your building policy. They can also be a point of vulnerability in high-wind events if not properly secured. Make sure your policy explicitly covers solar panels and that the sum insured accounts for their replacement cost.

Above-Average Fittings

The above-average fittings quality — think quality appliances, stone benchtops, premium fixtures — increases the cost to rebuild or repair the home to its original standard. This is factored into the building sum insured and contributes to the higher-than-median premium.

---

Tips for Homeowners in Beaconsfield

1. Check Your Sum Insured Carefully

With a 214 sqm home of above-average quality built in 2025, it's critical that your building sum insured accurately reflects current rebuild costs — not just the purchase price. Underinsurance is a serious risk in Queensland, particularly after a cyclone event when building costs can spike due to demand. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Compare Multiple Quotes Before Renewing

The spread of premiums in Beaconsfield is wide — from $3,177 at the 25th percentile to well above $6,000 at the top end. That gap represents real money. Insurers price cyclone risk differently, and shopping around at renewal time can yield meaningful savings without sacrificing cover quality. Get a comparison quote at CoverClub to see what else is available.

3. Review Your Contents Sum Insured Annually

An $85,000 contents value is reasonable for a 3-bedroom home, but contents values can creep up over time as you acquire new furniture, electronics, and appliances. Underinsuring your contents is just as risky as underinsuring the building — review your list each year and update accordingly.

4. Understand Your Cyclone Excess

Many insurers apply a separate, higher excess for cyclone claims on top of the standard excess. This can be a flat dollar amount or a percentage of the sum insured, and it's often buried in the fine print. Make sure you know what your cyclone excess is before you need to make a claim — and factor it into your emergency savings planning.

---

Ready to Find a Better Rate?

Whether this quote feels right or you suspect there's a better deal out there, the smartest move is to compare. CoverClub makes it easy to see how your premium stacks up and explore alternatives tailored to your property and location. Start your free quote comparison at CoverClub — it takes just a few minutes and could save you hundreds on your next renewal.