Beaconsfield is a small historic town in northern Tasmania, nestled in the Tamar Valley and known for its rich gold-mining heritage. It's a peaceful, semi-rural community that attracts homeowners looking for character and quiet — but like anywhere in Australia, protecting your property with the right home insurance is essential. This article breaks down a real home and contents insurance quote for a three-bedroom free standing home in Beaconsfield (postcode 7270), helping you understand what's driving the premium and whether it represents good value.

---

Is This Quote Fair?

The quote in question comes in at $1,835 per year (or $179/month) for a combined home and contents policy, covering a building sum insured of $550,000 and $50,000 worth of contents. Our analysis rates this quote as FAIR — around average for the area.

That rating holds up well when you look at the numbers. The suburb average sits at $1,848/yr and the median at $1,818/yr, meaning this quote lands almost exactly in the middle of the market for Beaconsfield. It falls comfortably within the interquartile range — between the 25th percentile of $1,531/yr and the 75th percentile of $2,085/yr — which tells us it's neither a bargain nor a rip-off. It's a solidly mid-market result.

That said, "fair" doesn't mean you can't do better. Premiums vary between insurers even for identical properties, and shopping around can sometimes shift you from the middle of the pack toward that lower quartile. More on that shortly.

---

How Beaconsfield Compares

One of the more encouraging aspects of this quote is just how favourably Beaconsfield stacks up against broader benchmarks. Check out the full suburb stats for Beaconsfield TAS 7270 for a deeper look, but here's the headline picture:

| Benchmark | Average Premium |

|---|---|

| Beaconsfield (suburb) | $1,848/yr |

| LGA – Latrobe (Tas.) | $2,263/yr |

| Tasmania (state) | $2,458/yr |

| Australia (national) | $2,965/yr |

Beaconsfield homeowners are paying significantly less than the Tasmanian state average of $2,458/yr — a difference of over $600 annually. Compared to the national average of $2,965/yr, the gap is even more striking, with local premiums running roughly 38% below what Australians pay on average.

This is largely a reflection of Beaconsfield's relatively low-risk profile. The area isn't classified as a cyclone risk zone, and while Tasmania does experience its share of storms and flooding, Beaconsfield doesn't carry the elevated risk premiums seen in coastal Queensland or bushfire-prone parts of Victoria and NSW.

It's worth noting that the sample size for this suburb is 24 quotes — a reasonable dataset, though not enormous. The averages are directionally reliable, but individual quotes can still vary depending on insurer appetite and specific property characteristics.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a detailed picture of your property. Here's how the key features of this particular home influence the premium:

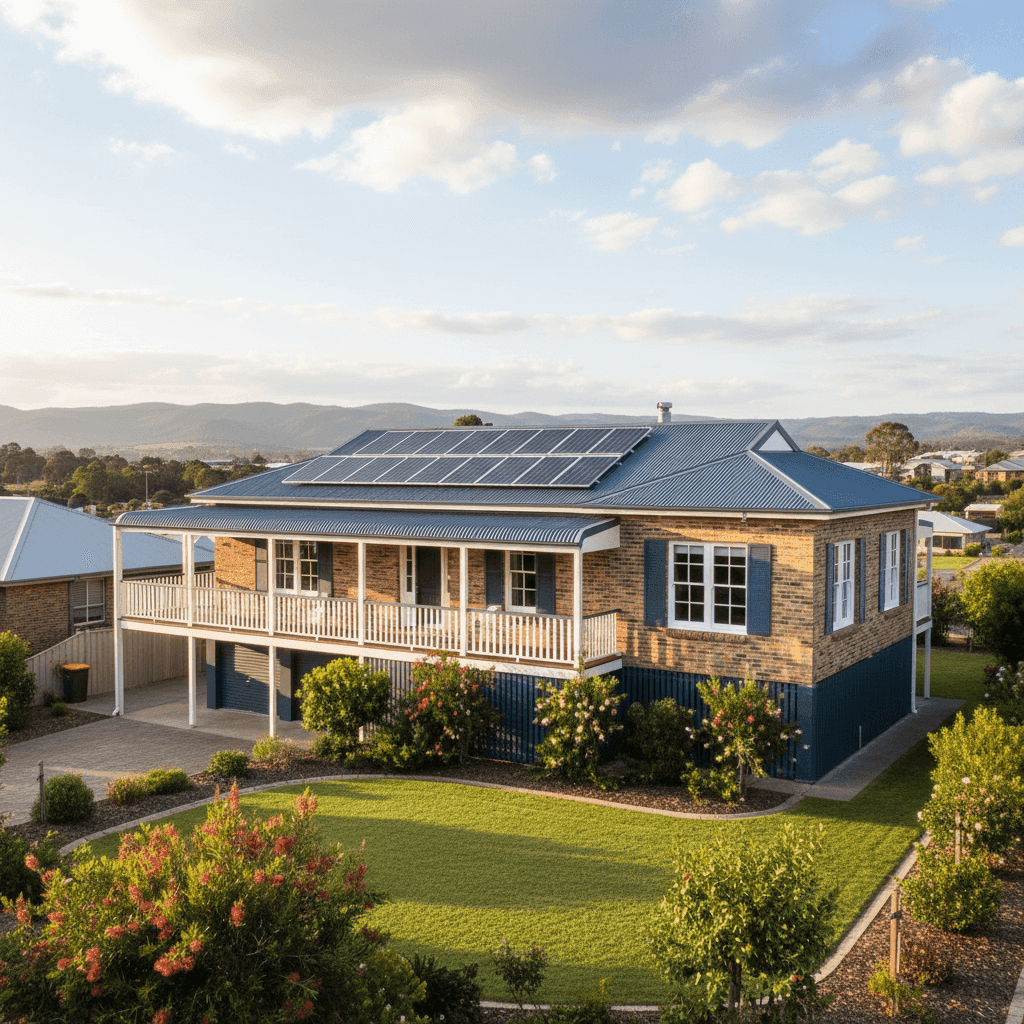

Brick Veneer Walls & Colorbond Roof Brick veneer is a popular and well-regarded construction type in Australia. It offers solid weather resistance and is generally viewed favourably by insurers. Combined with a steel Colorbond roof — durable, fire-resistant, and low-maintenance — this home presents a relatively low structural risk profile. These materials tend to attract more competitive premiums compared to, say, timber-framed homes with older roofing.

Stump Foundation & Elevated Position The home sits on stumps and is elevated by at least one metre. This is a classic construction style in many parts of Tasmania and can work both ways for insurance. On the positive side, elevation can reduce flood and moisture risk. However, elevated homes can also be more exposed to wind events, and the underfloor space introduces some additional considerations around maintenance and pest risk. Overall, this feature is fairly neutral for pricing in this region.

Timber & Laminate Flooring Timber and laminate floors are attractive but can be costly to repair or replace after water damage. Insurers factor this in, particularly given the elevated foundation style which can make underfloor moisture an issue over time.

Above Average Fittings Quality The home is noted as having above average fittings — think quality kitchen appliances, better-grade bathroom fixtures, and premium finishes. This pushes up the replacement cost of the building, which is reflected in the $550,000 sum insured. It's important this figure accurately reflects true rebuild costs, not just market value.

Solar Panels Solar panels are increasingly common across Australia, and insurers are becoming more accustomed to pricing them in. They add value to the property but also represent an additional asset to cover — particularly against storm, hail, or fire damage. Homeowners should confirm their policy explicitly covers rooftop solar systems.

No Pool, No Ducted Climate Control The absence of a pool removes a common source of liability and maintenance claims. No ducted climate control also keeps the mechanical complexity — and associated claims risk — lower.

---

Tips for Homeowners in Beaconsfield

1. Review your sum insured regularly Construction costs have risen sharply across Australia in recent years, and a building sum insured set a few years ago may no longer reflect what it would actually cost to rebuild your home today. With above average fittings, this is especially important — underinsurance is a real risk that can leave you significantly out of pocket after a major claim.

2. Confirm your solar panels are covered Not all standard home insurance policies automatically extend full cover to rooftop solar systems. Check the product disclosure statement (PDS) carefully, and if in doubt, ask your insurer directly. Given the cost of solar installations, you want to be certain they're included.

3. Maintain your stumps and subfloor space Elevated homes on stumps require periodic inspection to ensure the foundation remains sound and that moisture, rot, or pests haven't caused deterioration. Proactive maintenance not only protects your home but can also support your insurance position — some policies have exclusions for damage resulting from gradual deterioration or lack of maintenance.

4. Compare quotes at renewal time This quote is rated fair — but the market moves, and so does insurer appetite. What's competitive today may not be in 12 months. Running a comparison at renewal is one of the simplest ways to make sure you're not quietly drifting toward that upper quartile without realising it.

---

Compare Your Home Insurance Options

Whether you're a first-time buyer in Beaconsfield or a long-time local reviewing your cover, it pays to see the full picture. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in minutes — so you can see where your premium sits and whether there's a better deal waiting. Enter your address and get started today.