Beerwah is a relaxed hinterland suburb on Queensland's Sunshine Coast, known for its semi-rural character, family-friendly streets, and proximity to the Glass House Mountains. For owners of a free standing home in this area, understanding what drives your insurance premium — and whether you're paying a fair price — can make a real difference to your household budget. This article breaks down a recent home and contents insurance quote for a five-bedroom property in Beerwah (postcode 4519) and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,464 per year (or $325 per month) for combined home and contents cover, with a building sum insured of $820,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the Beerwah area.

To put that in perspective, the suburb average premium sits at $2,952 per year, and the median is even lower at $2,724 per year. This quote lands above the 75th percentile for the suburb (which is $3,228/yr), meaning it's priced higher than roughly three-quarters of comparable quotes we've seen in the area. That's a meaningful gap — around $512 more per year than the suburb average, and $740 more than the median.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, specific property features, and the insurer's own risk model all play a role. The key question is whether the coverage justifies the cost — and whether shopping around might uncover a better deal.

---

How Beerwah Compares

One of the more reassuring findings here is just how favourably Beerwah stacks up against broader Queensland benchmarks. Queensland as a whole has a state average premium of $9,129 per year — driven heavily by high-risk cyclone and flood zones in North Queensland — with a state median of $3,903 per year. By that measure, even this above-average Beerwah quote is well below the state average.

The Sunshine Coast LGA average sits at $7,249 per year, which reflects the broader coastal and hinterland region. Again, Beerwah's local premiums are substantially lower, suggesting the suburb carries a more manageable risk profile than many parts of the Sunshine Coast.

Zooming out to the national picture, the Australian average premium is $5,347 per year, with a national median of $2,764 per year. This quote sits above the national median but well below the national average — a reasonable position for a five-bedroom home with a sizeable building sum insured.

You can explore suburb-level statistics for Beerwah (4519) to see how premiums in your area have been trending and how your quote stacks up against the 23 quotes in our local dataset.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining when it comes to understanding the premium.

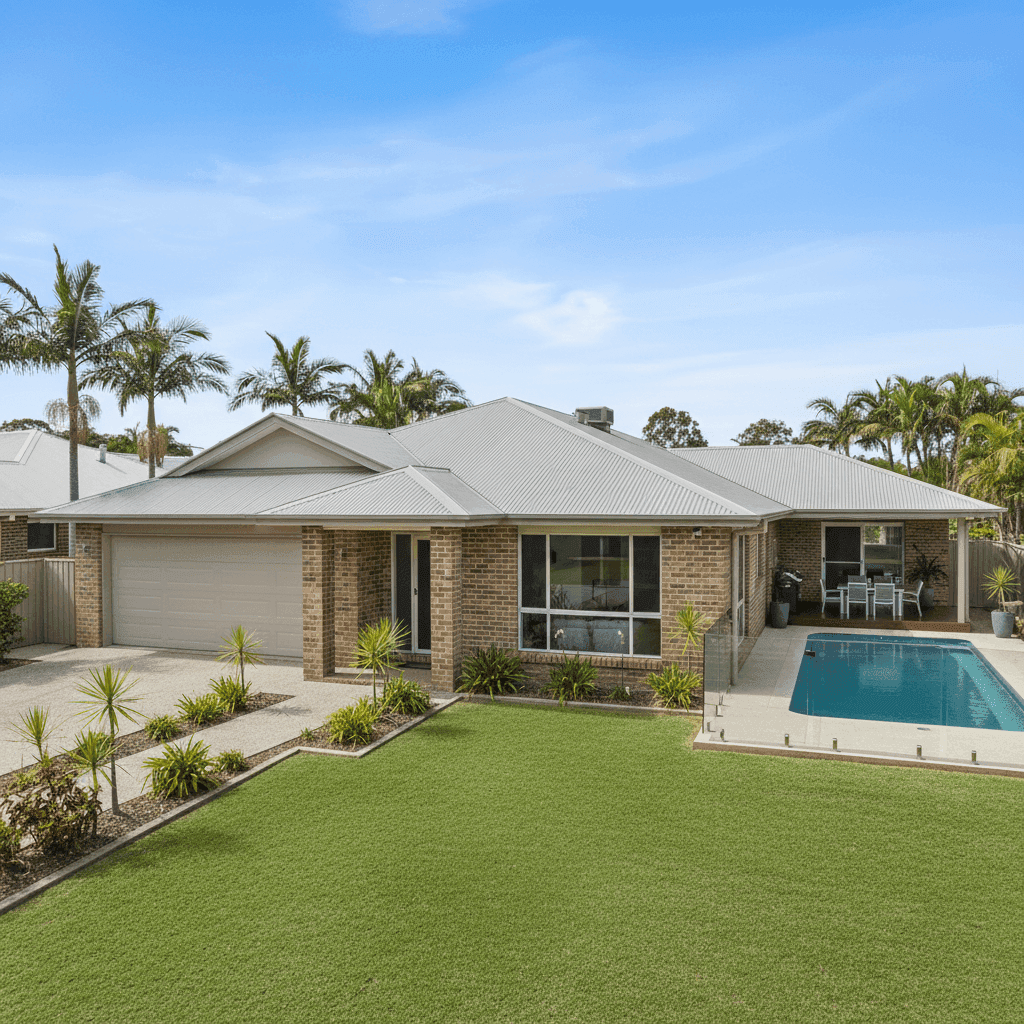

Size and sum insured: At 277 sqm with five bedrooms and two bathrooms, this is a substantial home. The $820,000 building sum insured reflects that scale, and a higher rebuild cost naturally pushes the premium up. It's worth periodically reviewing your sum insured to ensure it's accurate — both underinsurance and overinsurance carry risks.

Construction type: The home features brick veneer external walls and a steel/Colorbond roof, both of which are generally well-regarded by insurers. Brick veneer offers solid fire resistance, while Colorbond roofing is durable and performs well in Queensland's heat and occasional severe weather. These materials typically attract more favourable rates than timber-framed or fibro homes.

Foundation and flooring: A concrete slab foundation is standard for Queensland homes of this era and is generally considered a stable, low-risk construction method. Timber and laminate flooring is common and doesn't significantly influence the premium either way, though it's worth noting for contents cover purposes.

Built in 1985: A home approaching 40 years old may attract slightly higher premiums due to the age of plumbing, electrical systems, and roofing — even when the structure itself remains sound. Insurers factor in the likelihood of age-related claims.

Swimming pool: The presence of a pool adds both to the replacement cost of the property and to the insurer's liability considerations, which can nudge premiums upward.

Ducted climate control: Ducted air conditioning is a significant fixture that adds to the overall rebuild and replacement value of the home. Ensuring it's adequately captured in your sum insured is important.

No cyclone risk: Beerwah is not classified as a cyclone risk area, which is a meaningful premium advantage compared to coastal and northern Queensland properties where cyclone levies can add hundreds — or thousands — of dollars annually.

---

Tips for Homeowners in Beerwah

1. Review your building sum insured regularly Construction costs have risen significantly in recent years. If your $820,000 sum insured hasn't been reviewed lately, it may be worth getting a professional building valuation or using an online calculator to confirm it reflects current rebuild costs — not just the market value of your property.

2. Shop around before renewing Given this quote sits above the 75th percentile for Beerwah, there's a reasonable chance that comparing quotes from multiple insurers could uncover a more competitive premium for equivalent cover. Loyalty doesn't always pay with home insurance — renewal prices can creep up year on year.

3. Consider your excess settings Both excesses here are set at $1,000. Opting for a higher voluntary excess can reduce your annual premium, which may make sense if you're unlikely to make small claims. Conversely, if you'd prefer lower out-of-pocket costs at claim time, the current setting is reasonable.

4. Check what's included for your pool and ducted system Not all policies treat pools and ducted air conditioning the same way. Make sure your policy explicitly covers these fixtures under the building definition, and confirm whether accidental damage to the pool or ducted system is included or requires an optional add-on.

---

Ready to Compare?

If this quote feels a little steep, you're not alone — and the good news is that comparing your options has never been easier. At CoverClub, we help Australian homeowners see how their premiums stack up and find cover that suits their property and budget. Get a quote today and see what's available for your Beerwah home.