Nestled in the lush hinterland of Far North Queensland, Bellenden Ker is a small but striking community surrounded by World Heritage-listed rainforest and the dramatic peaks of the Bellenden Ker Range. It's the kind of place where the scenery is extraordinary — and where insuring your home comes with its own unique set of considerations. This article takes a close look at a recent home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Bellenden Ker (postcode 4871), breaking down what's driving the premium and whether the price stacks up.

---

Is This Quote Fair?

The annual premium for this property came in at $3,545 per year (or $340/month), covering a building sum insured of $600,000 and contents valued at $10,000. The building excess is $2,000 and the contents excess is $1,000.

Based on CoverClub's pricing data, this quote is rated CHEAP — meaning it sits below average for the area. That's genuinely good news for the homeowner. In a region of Queensland where insurance premiums can be eye-watering, landing a below-average quote for a property of this size and specification is a meaningful win.

It's worth noting that a "cheap" rating doesn't imply the cover is inadequate — it simply means the premium is competitive relative to comparable properties in the region. The $600,000 building sum insured is a substantial level of cover, and the combined home and contents policy provides broad protection.

---

How Bellenden Ker Compares

To put this quote in proper context, here's how it lines up against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,545 |

| QLD State Median | $3,903 |

| QLD State Average | $9,129 |

| National Median | $2,764 |

| National Average | $5,347 |

| LGA (Carpentaria) Average | $5,066 |

A few things stand out here. The Queensland state average of $9,129 is remarkably high — nearly triple the national average — which reflects the outsized impact of cyclone, flood, and storm risk across much of the state. The fact that this quote comes in well below both the QLD average and the LGA (Carpentaria) average of $5,066 is a strong indicator that the property's characteristics are working in the homeowner's favour.

Compared to the national average of $5,347, this quote is also meaningfully cheaper, though it does sit above the national median of $2,764. That's not surprising given the Far North Queensland location and the relatively high building sum insured. Overall, this is a competitive result.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some pushing it down, others keeping it in check.

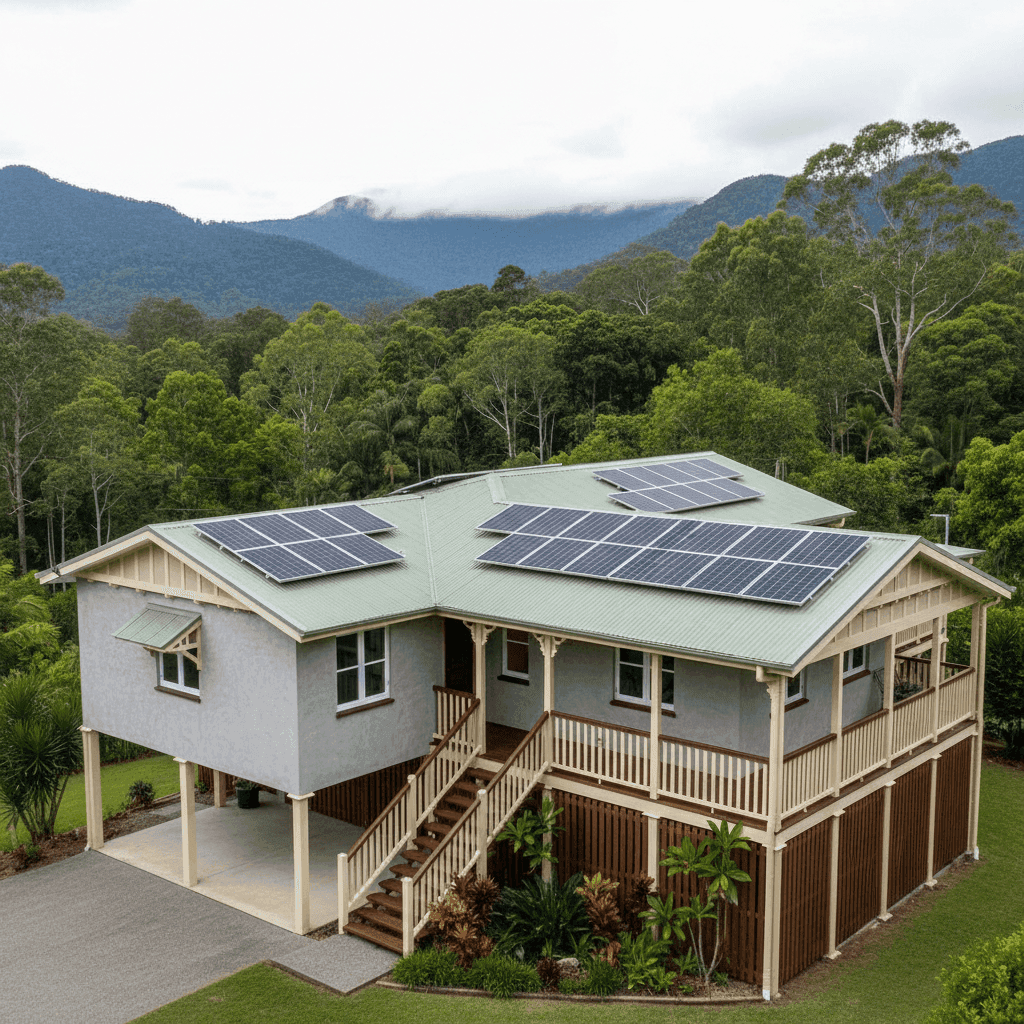

Construction Materials

The home features concrete external walls and a steel/Colorbond roof — a combination that insurers generally view favourably. Concrete is highly resistant to fire, wind, and pest damage, while Colorbond roofing is durable, low-maintenance, and performs well in extreme weather. Compared to timber-framed or fibrous cement homes, this construction profile typically attracts lower premiums.

Foundation and Flooring

Built on a concrete slab with tile flooring, this property has a solid, moisture-resistant base. Slab foundations are generally considered lower risk than suspended timber floors, particularly in areas prone to moisture or flooding. Tiles are similarly robust and don't carry the same water damage risk as carpet or timber flooring.

Elevation

The property is elevated by less than one metre, which provides a modest degree of flood mitigation. While it won't qualify for the same risk reduction as a fully elevated Queenslander, even a small amount of elevation can help in minor inundation events and may be factored into the insurer's assessment.

Heritage Overlay

This property sits under a heritage overlay, which is an important flag for insurers. Heritage-listed or heritage-overlay properties can be more expensive to repair or rebuild to the required standard, as they may need to use specific materials or construction methods to comply with heritage guidelines. This could push the rebuilding cost — and therefore the appropriate sum insured — higher than a comparable non-heritage property.

Solar Panels and Ducted Climate Control

The presence of solar panels and ducted climate control adds to the replacement value of the home. Both are typically covered under a home and contents policy, but it's worth confirming with your insurer that these are explicitly included and that the sum insured accounts for their replacement cost.

No Cyclone Risk

Interestingly, this property is not flagged as being in a cyclone risk area, which is somewhat unusual for Far North Queensland. This is likely a significant factor in keeping the premium below the regional average, as cyclone cover is one of the biggest cost drivers for QLD homeowners.

---

Tips for Homeowners in Bellenden Ker

1. Review your sum insured regularly With a heritage overlay, rebuilding costs can escalate quickly if specific materials or craftsmanship are required. Make sure your $600,000 sum insured is reviewed annually and updated to reflect current construction costs — underinsurance is a common and costly mistake.

2. Confirm solar panel and system coverage Solar panel systems and ducted air conditioning units can be expensive to replace. Check your policy wording to ensure these are covered for damage from storms, hail, and power surges, and that they're included in your building sum insured rather than treated as exclusions.

3. Understand your heritage obligations If your property is subject to a heritage overlay, speak with your insurer about how this affects your claim process. Some policies may not automatically cover the additional cost of heritage-compliant repairs — you may need to confirm this is explicitly included in your cover.

4. Compare quotes before renewal Even if your current premium is competitive, the insurance market shifts constantly. Use a comparison platform like CoverClub to benchmark your renewal quote each year — it takes minutes and could save you hundreds.

---

Find a Better Deal with CoverClub

Whether you're a first-time buyer or a long-term Bellenden Ker local, making sure you have the right home insurance at the right price is one of the smartest financial moves you can make. CoverClub makes it easy to compare home and contents quotes from leading Australian insurers in minutes — so you can see exactly where your premium sits and whether there's a better deal waiting for you.