If you own a free standing home in Bellingen, NSW 2454, you already know the appeal — lush hinterland scenery, a tight-knit community, and that unmistakable mid-North Coast charm. But owning property here also comes with real insurance considerations, from the age and construction style of local homes to the region's environmental risks. This article breaks down a recent building insurance quote of $3,535 per year for a 3-bedroom, 1-bathroom weatherboard home in Bellingen, and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote has been rated CHEAP (Below Average), meaning it sits well below what most homeowners in the same suburb are paying.

At $3,535 per year (or roughly $339 per month), this premium lands noticeably below the suburb's average of $5,033/yr and the suburb median of $5,045/yr. It also comes in under the 25th percentile for Bellingen, which sits at $3,867/yr — meaning this quote is cheaper than at least 75% of comparable quotes collected in the area. That's a strong result for a home insured at a $650,000 sum insured for building cover.

The building excess is set at $2,000, which is on the higher side and is one of the key levers that brings the annual premium down. A higher excess means the insurer takes on less risk for smaller claims, which is reflected in the lower price. It's worth keeping that trade-off in mind — you'll need to cover the first $2,000 out of pocket if you make a building claim.

---

How Bellingen Compares

To really understand what this quote means, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Premium |

|---|---|

| This Quote | $3,535/yr |

| Bellingen Suburb Average | $5,033/yr |

| Bellingen Suburb Median | $5,045/yr |

| Bellingen 25th Percentile | $3,867/yr |

| LGA (Nambucca Valley) Average | $5,223/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/yr is strikingly high — driven largely by expensive premiums in flood-prone, bushfire-affected, and high-density urban areas across the state. The state median of $3,770/yr is a far more representative figure for typical NSW homeowners, and this quote sits just slightly above it.

Against the national average of $5,347/yr, this quote looks very competitive. However, the national median of $2,764/yr is lower — a reminder that in cheaper parts of the country, home insurance can be significantly more affordable.

For Bellingen specifically, based on a sample of 14 quotes, the local market tends to price building cover in the $3,867–$6,045/yr range for the middle 50% of properties. Coming in below that band is a genuine win for this homeowner.

Explore more data for your area at the Bellingen suburb stats page, or browse NSW state-wide insurance statistics and national home insurance benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this particular home will have influenced how insurers priced the risk. Here's what matters most:

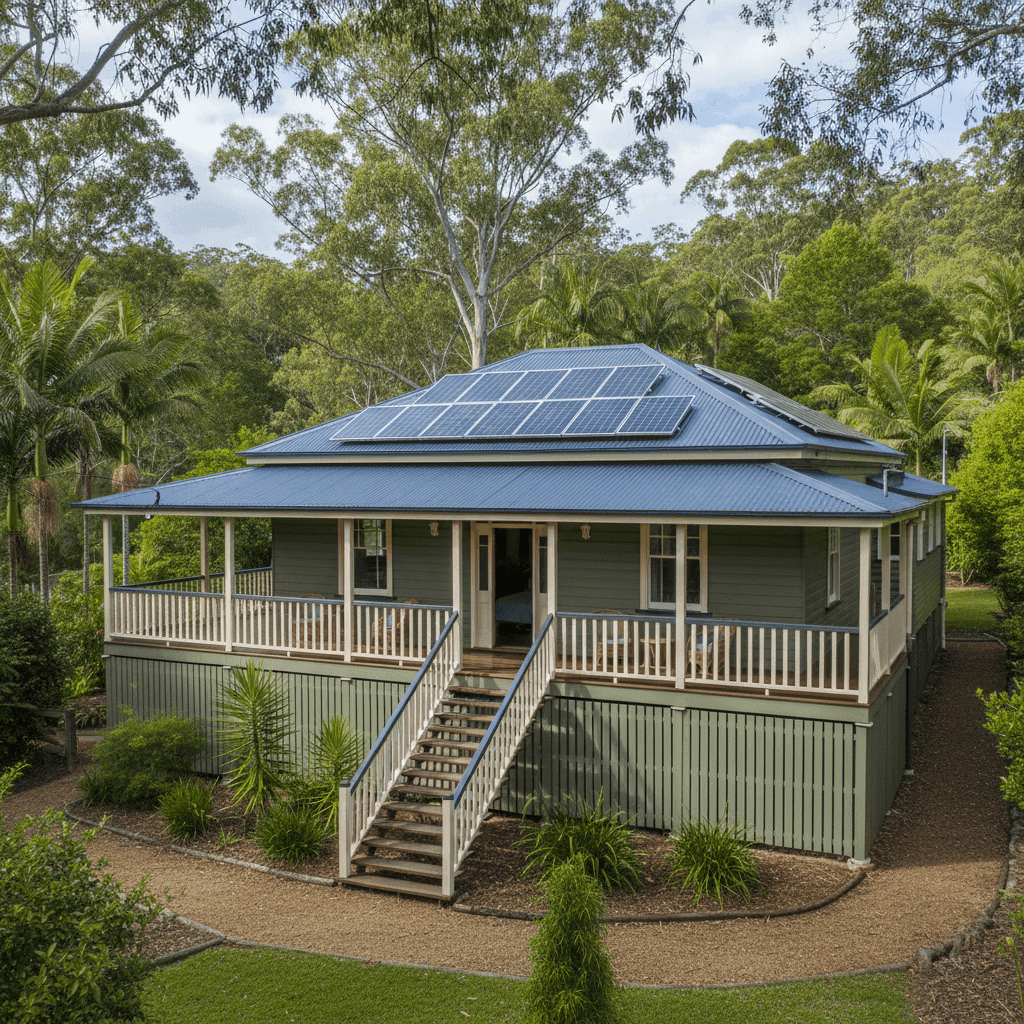

Weatherboard Timber Construction (1950)

Older weatherboard homes are one of the most common dwelling types in regional NSW — and one of the most nuanced to insure. Timber walls are more susceptible to fire, rot, and termite damage than brick veneer or double brick, which generally pushes premiums up. A home built in 1950 also raises questions for insurers around the condition of wiring, plumbing, and structural integrity. That said, many well-maintained heritage homes carry lower replacement costs than modern builds, which can offset some of that risk.

Elevated on Poles

The home sits elevated by at least 1 metre on poles — a classic Queenslander-influenced design common in flood-prone and hilly regions of regional NSW. Elevation is a significant flood-risk mitigant, and insurers often reward this with lower flood-related loading. In a region like the Bellingen Valley, where rivers can rise quickly, being up on stumps could meaningfully reduce your premium compared to a slab-on-ground home.

Steel/Colorbond Roof

A Colorbond steel roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in high-wind events. Compared to terracotta tiles or older fibrous cement sheeting, Colorbond tends to attract lower premiums and fewer maintenance concerns.

Solar Panels

The presence of solar panels adds a modest layer of complexity to building cover. Panels are typically covered under building insurance as a fixed structure, but their replacement cost needs to be factored into the sum insured. At $650,000, there should be adequate headroom here, but it's worth confirming with your insurer that solar is explicitly covered under your policy.

Ducted Climate Control

Ducted air conditioning is a fixed installation and is included in building cover. It also adds to the overall replacement value of the home, which is one reason a $650,000 sum insured is appropriate for a 130 sqm home with above-standard inclusions.

No Pool, No Cyclone Zone

The absence of a pool removes a common liability and premium driver. And while Bellingen sits in a region that can experience severe storms, it is not classified as a cyclone risk area, which avoids the significant premium loadings seen further north in Queensland and the NT.

---

Tips for Homeowners in Bellingen

1. Review your sum insured regularly Construction costs in regional NSW have risen sharply over the past few years. A $650,000 sum insured may be appropriate today, but it's worth reassessing annually — especially for a weatherboard home where labour and materials for authentic restoration can be expensive. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm flood and storm cover is included Bellingen sits in a valley and has a history of significant flood events. Make sure your policy explicitly includes flood cover — not just storm or rainwater damage. These are legally distinct definitions in Australian insurance policies, and some insurers still exclude flood as standard.

3. Document your solar panels and ducted system Keep records of the brand, model, installation date, and replacement cost of your solar panels and ducted climate control system. If you ever need to make a claim, having this documentation on hand will speed up the process and help ensure you're adequately compensated.

4. Consider whether a lower excess suits your situation The $2,000 building excess on this policy is what's keeping the premium down. If a $2,000 out-of-pocket expense would be a financial strain in the event of a claim, it may be worth requesting quotes with a lower excess — even if the annual premium increases slightly.

---

Compare Your Options with CoverClub

Whether you're insuring a heritage weatherboard in Bellingen or a modern brick home somewhere else in NSW, getting the right cover at the right price starts with comparing your options. CoverClub makes it easy to see what multiple insurers would charge for your specific property — so you're never paying more than you need to.

Get a building insurance quote today and see how your premium stacks up against your neighbours.