If you own a free standing home in Belmore, NSW 2192, you're probably curious about whether you're paying a fair price for home and contents insurance — or leaving money on the table. This article breaks down a real quote for a four-bedroom, two-bathroom property in the suburb, compares it against local, state, and national benchmarks, and offers practical advice to help you get better value on your cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,911 per year (or $187/month), covering both building (sum insured: $627,000) and contents ($50,000). Based on CoverClub's pricing data, this quote is rated Expensive — above average for the Belmore area.

To put that in perspective, the suburb average premium sits at $1,342/year, and the median is even lower at $1,303/year. That means this quote is roughly $569 above the local average — a meaningful gap worth investigating before simply accepting the renewal or binding the policy.

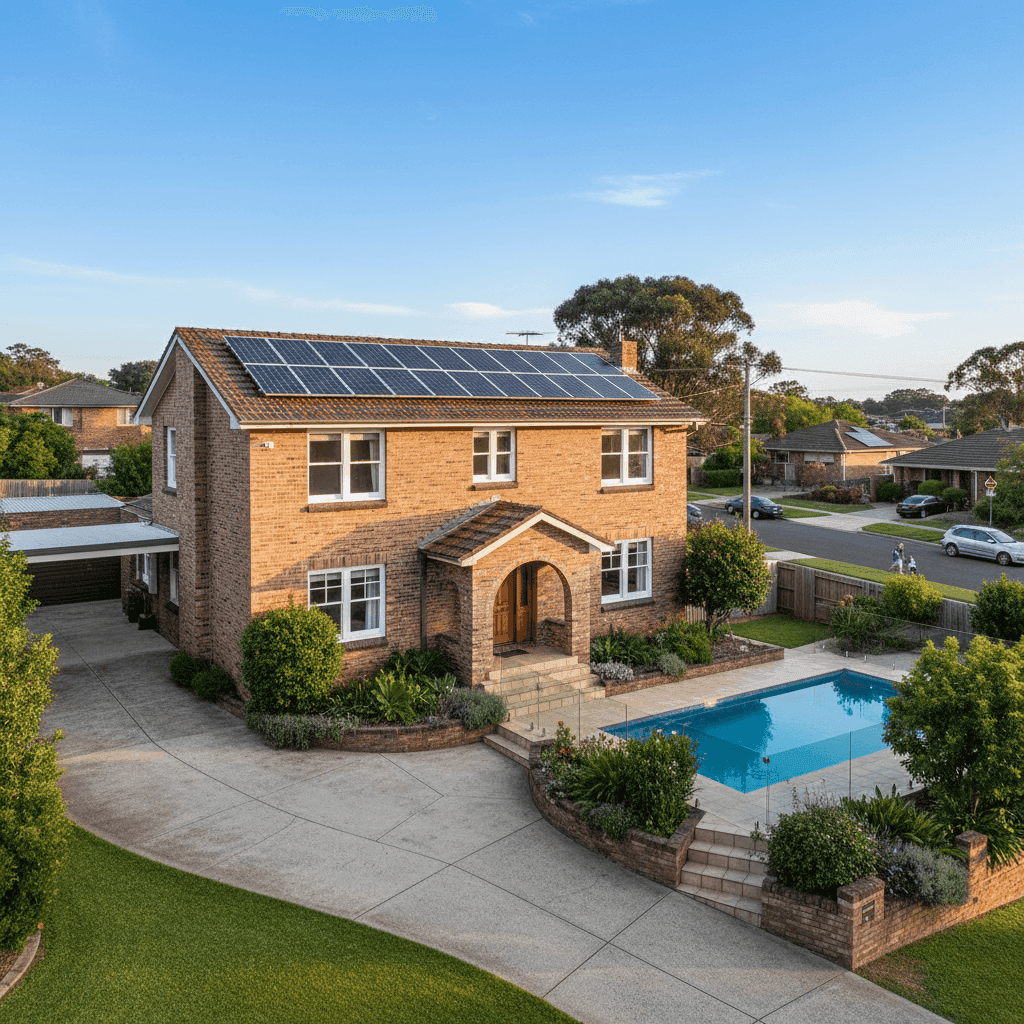

That said, "expensive" doesn't automatically mean wrong. The building sum insured of $627,000 is substantial, and the property has several features — a swimming pool, solar panels, and ducted climate control — that insurers typically load premiums for. The higher building excess of $2,000 may also suggest the insurer has priced in some risk, while the relatively low contents excess of $600 reflects the modest $50,000 contents value.

---

How Belmore Compares

Understanding where Belmore sits in the broader insurance landscape is useful context when evaluating any quote. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Belmore (NSW 2192) | $1,342/yr | $1,303/yr |

| Canterbury-Bankstown LGA | $1,910/yr | — |

| NSW State | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, Belmore is significantly cheaper than the NSW state average — by more than $2,400/year on average. This reflects the suburb's relatively low exposure to catastrophic natural hazards like cyclones, bushfires, and major flooding compared to other parts of the state.

Second, this particular quote of $1,911 actually aligns closely with the Canterbury-Bankstown LGA average of $1,910/year — suggesting it may be more representative of the broader local government area than the suburb-level sample (which is based on 18 quotes). It's worth checking the Belmore suburb stats page to see how the quote distribution looks across the postcode, and comparing against NSW state-wide data or the national overview for broader context.

The 25th percentile for Belmore is $891/year — meaning a quarter of quotes in the suburb come in under that figure. If you're paying nearly $1,911, there's a real possibility that shopping around could yield significant savings.

---

Property Features That Affect Your Premium

Insurers don't price every home the same way. The specific characteristics of this property play a meaningful role in how the premium is calculated.

Double brick construction is generally viewed favourably by insurers. It offers strong structural integrity, good fire resistance, and durability — factors that can reduce the likelihood of major claims. Compared to weatherboard or cladding homes, double brick properties often attract more competitive premiums.

Concrete tile roofing is similarly well-regarded. It's durable, fire-resistant, and less susceptible to storm damage than corrugated iron or older terracotta tiles. Combined with a slab foundation, this home has a solid structural profile that insurers tend to reward.

The swimming pool is a notable premium driver. Pools increase liability risk — particularly for third-party injury — and also add to the cost of reinstatement if the property is damaged. Most insurers factor pool ownership into their pricing models.

Solar panels are increasingly common in Australian suburbs, but they do add complexity to a home insurance policy. Panels can be damaged by hail, storms, or fire, and their replacement cost is non-trivial. Insurers typically include them in the building sum insured, but it's worth confirming this is the case with your specific policy.

Ducted climate control systems are another feature that can nudge premiums upward. These systems are expensive to repair or replace, and damage to ductwork — particularly in the event of a fire or storm — can be a significant component of a building claim.

Timber and laminate flooring can be a double-edged sword. While visually appealing and common in homes of this era (built 1999), timber flooring is more susceptible to water damage than tiles, which can influence how insurers assess internal damage claims.

The property's slight elevation (less than 1 metre) and the fact that it's not in a cyclone risk area are both positive factors that help keep the premium from climbing even higher.

---

Tips for Homeowners in Belmore

1. Compare multiple quotes before renewing The spread between the 25th percentile ($891) and 75th percentile ($1,686) in Belmore is wide — nearly $800 per year. That tells you there's real variation in the market. Don't assume your renewal price is the best available. Use a comparison tool like CoverClub to benchmark your quote against live alternatives.

2. Review your sum insured carefully A building sum insured of $627,000 for a 153 sqm home in Belmore is on the higher end. Make sure your sum insured reflects the actual cost to rebuild — not the market value of the property. Overinsuring drives up premiums unnecessarily, while underinsuring can leave you exposed at claim time. A quantity surveyor or online rebuild calculator can help you land on the right figure.

3. Consider a higher excess to reduce your premium The building excess on this policy is $2,000, which is already moderate. If you're financially comfortable covering a larger out-of-pocket cost in the event of a claim, opting for a higher excess (say, $2,500–$5,000) can meaningfully reduce your annual premium. Just make sure the saving justifies the trade-off.

4. Ask about discounts for home security and safety features Many insurers offer discounts for homes with monitored alarm systems, deadlocks, and security cameras. Given that this is a well-built double brick home with solid features, it's worth asking your insurer whether any additional security upgrades could unlock a lower rate.

---

Ready to Find a Better Deal?

Whether this quote is the right fit depends on your full policy details, not just the premium. But if you're paying above the local average, it's absolutely worth exploring your options. At CoverClub, you can compare home and contents insurance quotes tailored to your property in Belmore — quickly, transparently, and without the sales pressure. It only takes a few minutes, and the savings could be well worth it.