If you own a free standing home in Belrose, NSW 2085, you're likely paying close attention to the rising cost of home insurance — and for good reason. Belrose sits in the Northern Beaches LGA, one of Sydney's most desirable and well-established suburban corridors. But desirability doesn't always translate to affordable premiums. This article breaks down a real home and contents insurance quote for a five-bedroom property in the area, benchmarks it against local, state, and national data, and offers practical advice for homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The quote in question comes to $3,190 per year (or $306/month) for combined home and contents insurance, covering a building sum insured of $898,000 and contents valued at $80,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the Belrose area.

To put that in context: the suburb average premium for Belrose is $2,027/year, and the median sits at $1,922/year. This quote comes in at roughly 57% above the suburb average and well above the 75th percentile of $2,849/year. In other words, only about one in four quotes in the area costs more than this one — which means there's a reasonable chance a comparable property could be insured for less.

That said, premium price alone doesn't tell the whole story. A higher sum insured ($898,000 for the building alone is substantial), a pool, solar panels, ducted climate control, and the property's age all contribute to a higher-than-average risk profile. We'll unpack those factors shortly.

---

How Belrose Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful things you can do as a homeowner. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $3,190/yr |

| Belrose suburb average | $2,027/yr |

| Belrose suburb median | $1,922/yr |

| Northern Beaches LGA average | $3,266/yr |

| NSW state median | $3,770/yr |

| National median | $2,764/yr |

A few things stand out here. While the quote looks expensive compared to the Belrose suburb average, it's actually below the NSW state median of $3,770/year and also below the Northern Beaches LGA average of $3,266/year. The NSW state average of $9,528/year is heavily skewed by high-risk regional areas — think flood zones and cyclone-prone coastal regions — so the median is a far more useful comparator.

Against the national median of $2,764/year, this quote is elevated, but not dramatically so given the size and features of the property.

You can explore more suburb-level data on the Belrose insurance stats page, compare it to the broader NSW insurance landscape, or view national home insurance benchmarks to see how your area tracks across Australia.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely pushing the premium above the suburb norm. Here's what insurers are paying attention to:

Size and Sum Insured

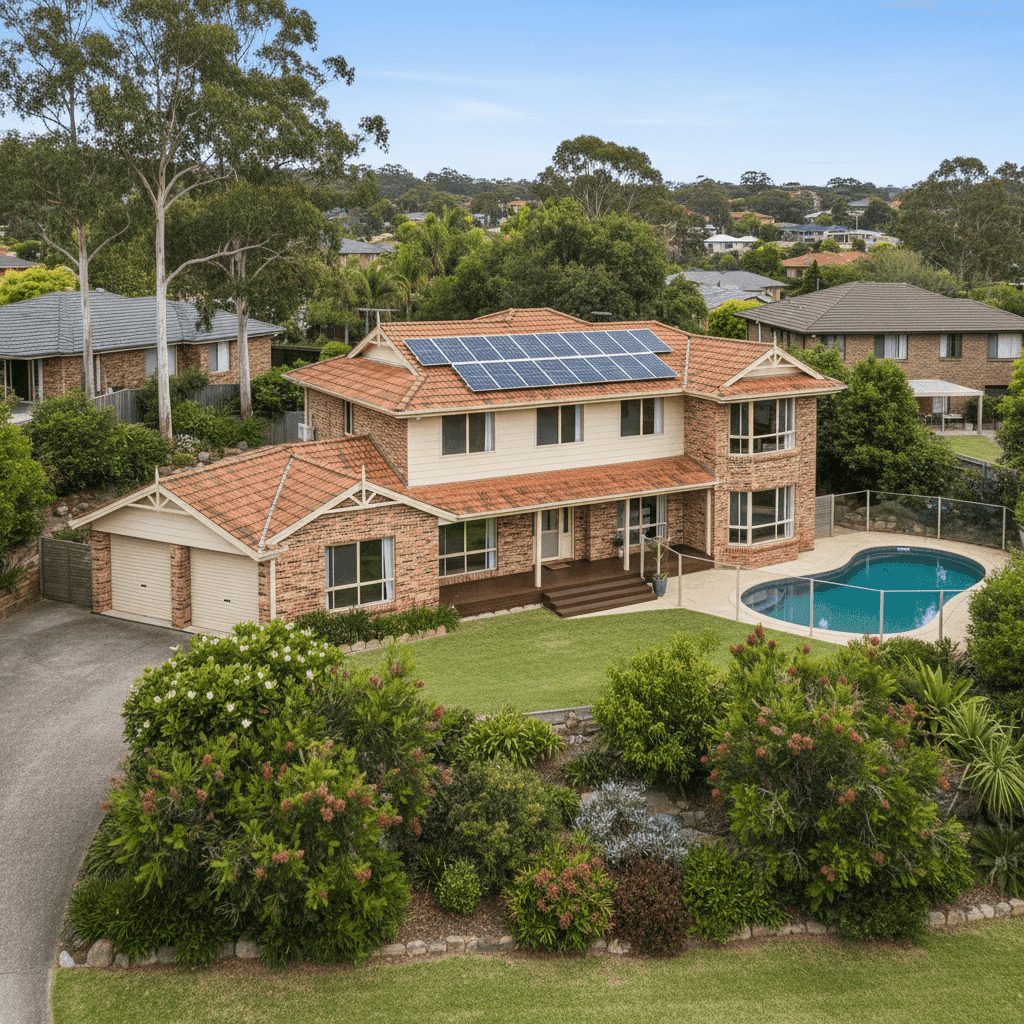

At 315 sqm with five bedrooms and three bathrooms, this is a large home. The building sum insured of $898,000 reflects the significant cost to rebuild — and insurers price accordingly. Larger homes cost more to reconstruct, and that risk is baked directly into your premium.

Construction Year and Materials

Built in 1975, this home is now over 50 years old. Older properties can carry higher premiums due to the increased likelihood of wear-and-tear claims, outdated wiring or plumbing, and the higher cost of sourcing period-appropriate materials for repairs. The brick veneer external walls and tiled roof are generally viewed favourably by insurers — both are durable and fire-resistant — but the stump foundation and timber/laminate flooring introduce some additional considerations around moisture, movement, and potential subsidence over time.

Pool

A swimming pool is a liability and maintenance consideration that most insurers factor into their pricing. Pools increase the risk of personal injury claims and can also be a source of property damage (leaks, structural issues). Expect this to add a modest but meaningful amount to your annual premium.

Solar Panels

Solar panel systems are now a standard feature on many Australian homes, but they do add to the replacement cost of the property. If panels are damaged in a storm or hailstorm — both realistic risks in Sydney — the insurer is on the hook for a potentially significant repair or replacement bill.

Ducted Climate Control

Ducted air conditioning systems are expensive to install and repair. Insurers account for this in their assessment of the property's overall replacement value and mechanical systems risk.

No Cyclone Risk

One factor working in this property's favour is that Belrose is not in a cyclone risk zone. This keeps the premium lower than it might otherwise be for comparable properties in northern Queensland or Western Australia.

---

Tips for Homeowners in Belrose

If you're looking to reduce your home insurance costs without compromising on cover, here are four practical steps worth considering:

- Review your sum insured annually. Building costs fluctuate, and being over-insured is a common — and costly — mistake. Use an independent building cost calculator to ensure your sum insured reflects current rebuild costs, not an inflated estimate. Equally, make sure you're not under-insured, which can be just as damaging at claim time.

- Bundle your building and contents cover. Most insurers offer a discount when you combine building and contents under a single policy. This quote already does that, but if you're currently holding separate policies, consolidating could save you a meaningful amount each year.

- Compare quotes before renewal. Loyalty doesn't always pay in insurance. Insurers frequently offer better rates to new customers than to existing ones. Set a reminder to shop around at least 30 days before your renewal date — CoverClub makes it easy to compare options for your address.

- Consider a higher excess. Increasing your excess from $1,000 to $2,000 or more can noticeably reduce your annual premium. This works best if you have a financial buffer to cover the higher out-of-pocket cost in the event of a claim, and you're primarily using insurance for major, catastrophic events rather than minor repairs.

---

Get a Better Deal on Home Insurance

Whether you're renewing soon or just curious about what else is out there, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub aggregates real quote data from across Australia to help homeowners make informed decisions — no jargon, no pressure.

Compare home insurance quotes for your property today at CoverClub and see how your current premium stacks up.