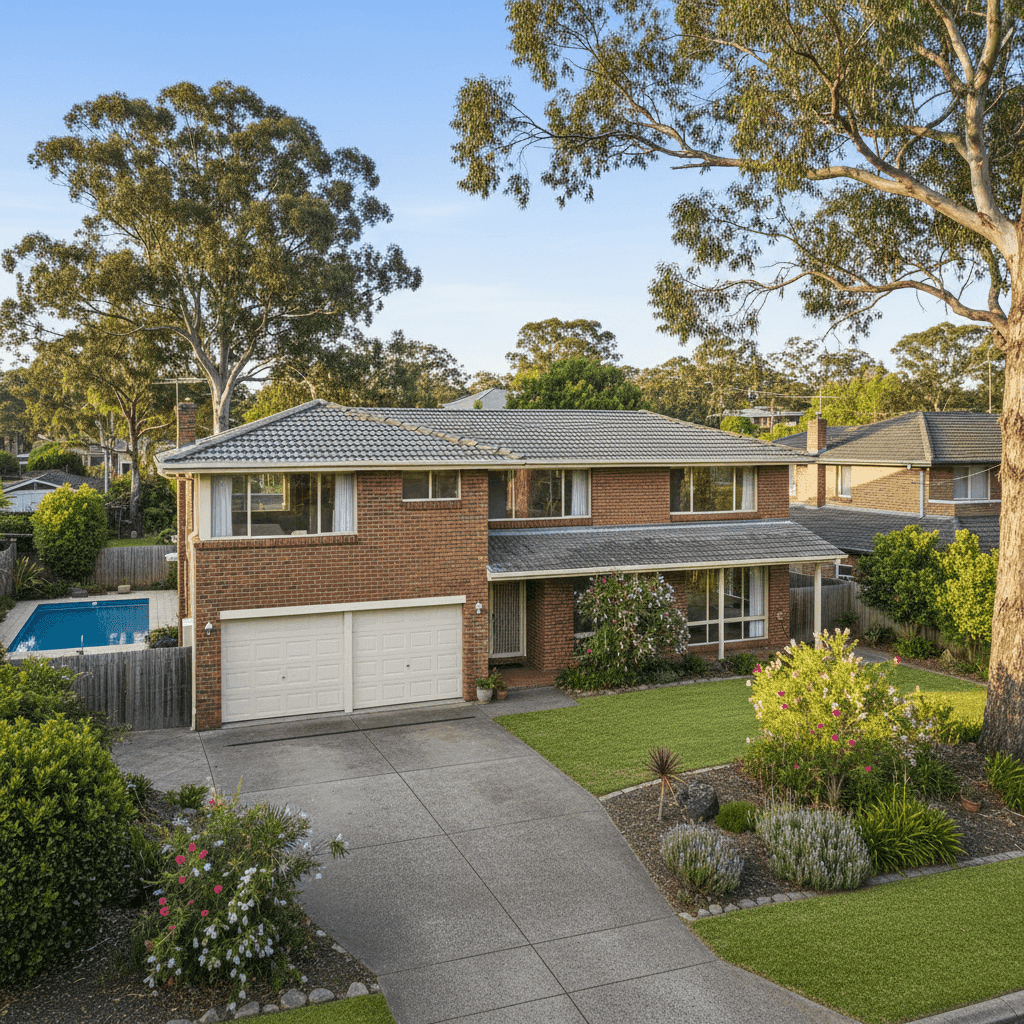

If you own a free standing home in Belrose, NSW 2085, you're likely no stranger to the realities of insuring a well-established suburban property on Sydney's Northern Beaches. With brick veneer construction, a concrete tile roof, timber flooring, and a backyard pool, homes like this carry a distinct risk profile — and that profile has a direct impact on what you pay each year for home and contents cover.

This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom property in Belrose, examining whether the premium is competitive, how it stacks up against local and national benchmarks, and what steps homeowners can take to manage their costs.

---

Is This Quote Fair?

The quote in question comes in at $2,886 per year (or $277 per month) for combined home and contents cover, with a building sum insured of $750,000 and contents valued at $100,000. Both the building and contents excess are set at $5,000.

Our analysis rates this quote as Expensive — Above Average.

To put that in context: the average premium paid by homeowners in Belrose currently sits at $2,027 per year, with a median of $1,922. This quote lands 42% above the suburb average and 50% above the median — a meaningful gap that's worth interrogating before renewing or accepting the policy.

That said, it's not wildly out of range. The 75th percentile for Belrose premiums is $2,849 per year, meaning roughly 25% of comparable quotes in the area come in at a similar level or higher. So while this isn't the most competitive price on the market, it's not an outlier either — particularly for a property of this size (214 sqm) with a pool and ducted climate control adding to the insured risk.

You can explore the full range of premiums for this postcode at our Belrose suburb stats page.

---

How Belrose Compares

Understanding where Belrose sits within the broader insurance landscape helps frame whether a premium like this is genuinely high or simply reflective of the local market.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Belrose (2085) | $2,027/yr | $1,922/yr |

| Northern Beaches LGA | $3,266/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Belrose is actually quite affordable relative to the broader Northern Beaches LGA average of $3,266 — suggesting that this particular suburb benefits from lower flood, bushfire, or storm risk compared to some of its coastal or escarpment neighbours.

Second, the NSW state average of $9,528 is dramatically elevated, largely driven by high-risk postcodes in regional and coastal NSW where cyclone, flood, and storm surge exposure push premiums into the tens of thousands. The median of $3,770 is a more useful comparison for metropolitan homeowners.

At a national level, the median sits at $2,764 — meaning this Belrose quote of $2,886 is marginally above the national midpoint, but not dramatically so.

Browse NSW home insurance statistics or national benchmarks to see how your own property compares.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the above-average premium. Understanding these factors can help you have a more informed conversation with insurers.

Brick Veneer Walls & Concrete Roof Brick veneer is one of the more common construction types across Sydney's older suburbs, and it's generally viewed favourably by insurers for its fire resistance and durability. The concrete tile roof is similarly robust. However, the age of the property — built in 1973 — means the underlying structure is over 50 years old. Older homes can carry higher rebuild costs due to non-standard materials, potential asbestos remediation, and the need to meet current building codes upon reconstruction.

Slab Foundation & Timber/Laminate Flooring A concrete slab foundation is generally considered low-risk from a subsidence perspective. However, the timber and laminate flooring throughout the home adds to the contents and internal fitout value, contributing to the overall rebuild cost estimate.

Swimming Pool A backyard pool increases liability exposure and adds to the overall insured value of the property. Most insurers factor pool inclusion into the building sum insured, and some apply additional loading for liability risk.

Ducted Climate Control Ducted air conditioning systems are expensive to repair or replace, and their inclusion in the building sum insured is appropriate — but it does push the replacement cost higher, which flows through to the premium.

Building Sum Insured: $750,000 At 214 sqm, a building sum insured of $750,000 equates to roughly $3,505 per square metre. This is within a reasonable range for Sydney construction costs in 2025–26, particularly for a home requiring full compliance with current building standards upon a total loss. Underinsurance is a genuine risk in this market, so it's worth having a quantity surveyor assess your rebuild cost if you haven't done so recently.

---

Tips for Homeowners in Belrose

1. Shop around at renewal time The single most effective way to reduce your premium is to compare quotes from multiple insurers before your policy renews. The gap between the cheapest and most expensive quotes in Belrose can exceed $1,600 per year for comparable cover. Use CoverClub's free quote comparison tool to see what's available for your specific property.

2. Review your sum insured carefully Both overinsurance and underinsurance carry risks. If your building sum insured is set significantly higher than your actual rebuild cost, you're paying more than necessary. Conversely, if it's too low, you may face a shortfall after a major claim. Consider engaging a professional building estimator or using an online calculator to validate your figure.

3. Consider your excess strategically This quote carries a $5,000 excess on both building and contents — which is on the higher end. A higher excess typically reduces your annual premium, but it means a larger out-of-pocket cost at claim time. If you have the financial buffer to absorb a $5,000 expense, this can be a sound strategy. If not, it may be worth exploring policies with a lower excess, even if the annual premium is slightly higher.

4. Ask about discounts for security and safety features Many insurers offer premium discounts for homes with monitored alarm systems, deadbolts, and smoke detectors. If your Belrose home has these features and they're not already reflected in your quote, it's worth flagging them with your insurer or broker.

---

Ready to Find a Better Rate?

Whether you're renewing your current policy or insuring a new property, comparing quotes is the fastest way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up and find competitive options tailored to your property.