If you own a free standing home in Benaraby, QLD 4680, you've probably noticed that home insurance premiums in regional Queensland can vary dramatically. This article breaks down a real building-only insurance quote for a 3-bedroom, 2-bathroom brick veneer home in the area — and helps you understand whether what you're paying stacks up against the suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $9,359 per year (or $897/month) for building-only cover, with a $2,000 building excess and a sum insured of $770,000. Based on available market data, this premium is rated Expensive — above average for the area.

To put that in perspective, the suburb average for Benaraby sits at $4,638/year, and the median is even lower at $4,377/year. This quote is more than double the local median, which is a significant gap worth investigating before simply accepting the renewal or the first quote you receive.

That said, it's worth noting that the 75th percentile for the suburb reaches $6,129/year, meaning roughly 25% of quotes in the area do exceed that figure. At $9,359, this quote pushes well beyond even that upper band — suggesting there may be room to negotiate or shop around for a more competitive rate.

---

How Benaraby Compares

Understanding where Benaraby sits relative to broader benchmarks gives useful context for any homeowner trying to make sense of their premium.

| Benchmark | Average | Median |

|---|---|---|

| Benaraby (QLD 4680) | $4,638/yr | $4,377/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/year is actually quite close to the quote being analysed — which tells us that while this premium looks steep at the suburb level, it's broadly in line with what many Queenslanders are paying statewide. This is largely a reflection of Queensland's elevated risk profile, driven by flood, storm, and cyclone exposure across much of the state.

However, the Queensland median of $3,903/year is significantly lower than the state average, indicating that a small number of very high premiums are pulling the average upward. In other words, most Queensland homeowners are paying considerably less — so a premium approaching $9,400 warrants scrutiny.

At the national level, the average sits at $5,347/year and the median at $2,764/year, reinforcing that this quote is on the higher end of the spectrum by any measure.

You can explore local pricing trends on the Benaraby suburb stats page, compare against the broader Queensland insurance landscape, or view national home insurance benchmarks.

---

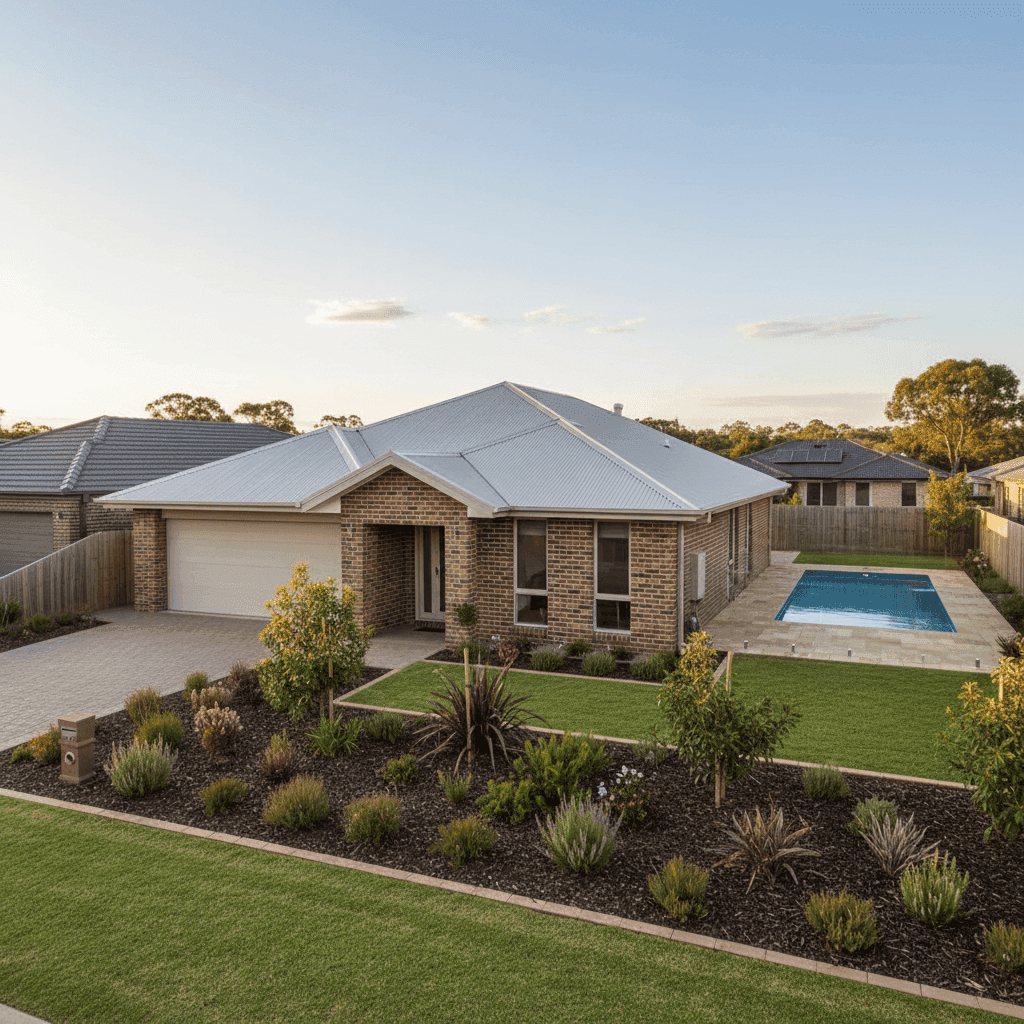

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — both positively and negatively.

Construction Materials

The home features brick veneer external walls and a steel/Colorbond roof, which are generally well-regarded by insurers. Brick veneer offers solid fire resistance, while Colorbond roofing is durable, lightweight, and performs well in high-wind conditions. These materials typically attract more favourable premiums compared to weatherboard or older tile roofs.

Slab Foundation & Vinyl Flooring

Built on a concrete slab with vinyl flooring, this property has a relatively straightforward risk profile from a structural standpoint. Slab foundations are common in Queensland and don't carry the elevated flood or moisture risk associated with raised or timber subfloor construction.

Swimming Pool

The presence of a pool is a notable factor. Pools introduce additional liability exposure — for example, risks associated with accidental drowning or injury — and can add to the overall premium cost. Insurers assess pool-related liability as part of the broader property risk.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset within the home. As a building-only policy, the insured sum needs to account for the cost of replacing this system as part of the structure, which can contribute to a higher sum insured and, in turn, a higher premium.

Sum Insured

At $770,000, the sum insured is substantial for a 139 sqm home built in 2000 with standard fittings. It's worth reviewing whether this figure accurately reflects the current rebuilding cost — not the market value — of the property. Overinsuring can unnecessarily inflate your premium, while underinsuring leaves you exposed. A quantity surveyor or online building cost calculator can help you arrive at an accurate figure.

Year Built & Fittings

The home was constructed in 2000, placing it in a relatively modern bracket. Combined with standard fittings quality, this generally works in the homeowner's favour, as newer builds with standard finishes are typically less expensive to repair or rebuild than older homes with premium materials.

---

Tips for Homeowners in Benaraby

1. Shop Around and Compare Multiple Quotes

The most effective way to reduce your premium is to compare offers from multiple insurers. A quote that's more than double the local median is a strong signal that alternatives exist. Use a comparison platform like CoverClub to see a range of options side by side.

2. Review Your Sum Insured

Make sure your $770,000 sum insured reflects the actual cost to rebuild your home, not its sale price or land value. If your sum insured is higher than necessary, you may be paying a premium you don't need to. Conversely, if it's too low, you risk being underinsured at claim time.

3. Consider Increasing Your Excess

A $2,000 building excess is moderate. In many cases, opting for a higher voluntary excess — say $2,500 or $3,000 — can meaningfully reduce your annual premium. Just ensure you can comfortably cover the excess amount if you need to make a claim.

4. Ask About Discounts

Many insurers offer discounts for security features such as deadbolts, alarm systems, or monitored security. If your home has these features, make sure they're noted in your policy. Some insurers also reward loyalty or multi-policy holders, so it's worth asking what's available.

---

Ready to Find a Better Rate?

If your current home insurance quote isn't measuring up, you don't have to accept it. CoverClub makes it easy for Australian homeowners to compare building and contents insurance quotes in minutes. Whether you're in Benaraby or anywhere else across the country, get a quote today and see how much you could save.