If you own a free standing home in Bennett Springs, WA 6063, you've probably wondered whether the premium sitting in your inbox is a fair deal or whether you're leaving money on the table. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom property in the suburb — and puts the numbers into context using suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $1,703 per year (or roughly $162 per month) for combined home and contents cover, with a building sum insured of $600,000 and contents valued at $180,000. The building excess is $2,500, and the contents excess is $500.

Our pricing analysis rates this quote as Expensive — above average for the Bennett Springs area.

To understand why, it helps to look at what other homeowners nearby are paying. The suburb average premium in Bennett Springs sits at $1,136 per year, with a median of just $914. This quote comes in at nearly 50% above the suburb average and almost double the median — a meaningful gap worth investigating before you simply accept the renewal.

That said, context matters. The quote isn't wildly out of step with the suburb's upper range: the 75th percentile for Bennett Springs is $1,537 per year, so this premium sits only modestly above the top quartile. In other words, it's on the expensive side, but not dramatically so — and the property's specific features (more on those below) do justify some of the loading.

---

How Bennett Springs Compares

Zooming out beyond the suburb paints an interesting picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bennett Springs (suburb) | $1,136/yr | $914/yr |

| Swan LGA | $4,057/yr | — |

| Western Australia | $2,811/yr | $2,127/yr |

| National | $5,347/yr | $2,764/yr |

Compared to the Western Australian state average of $2,811, this quote is actually well below what WA homeowners pay on average — nearly 40% cheaper. And against the national average of $5,347, the premium looks positively affordable.

The Swan LGA average of $4,057 per year is particularly striking — it suggests that parts of the broader Swan local government area carry significantly higher risk profiles, which makes Bennett Springs a relatively cost-effective suburb to insure within its own council boundaries.

So the picture is nuanced: this quote is above average for Bennett Springs specifically, but below average for WA as a whole. Whether that makes it "fair" depends on your individual property's risk factors — and there are several worth discussing here.

---

Property Features That Affect Your Premium

Several characteristics of this property influence what insurers charge, and understanding them helps you assess whether the premium is justified.

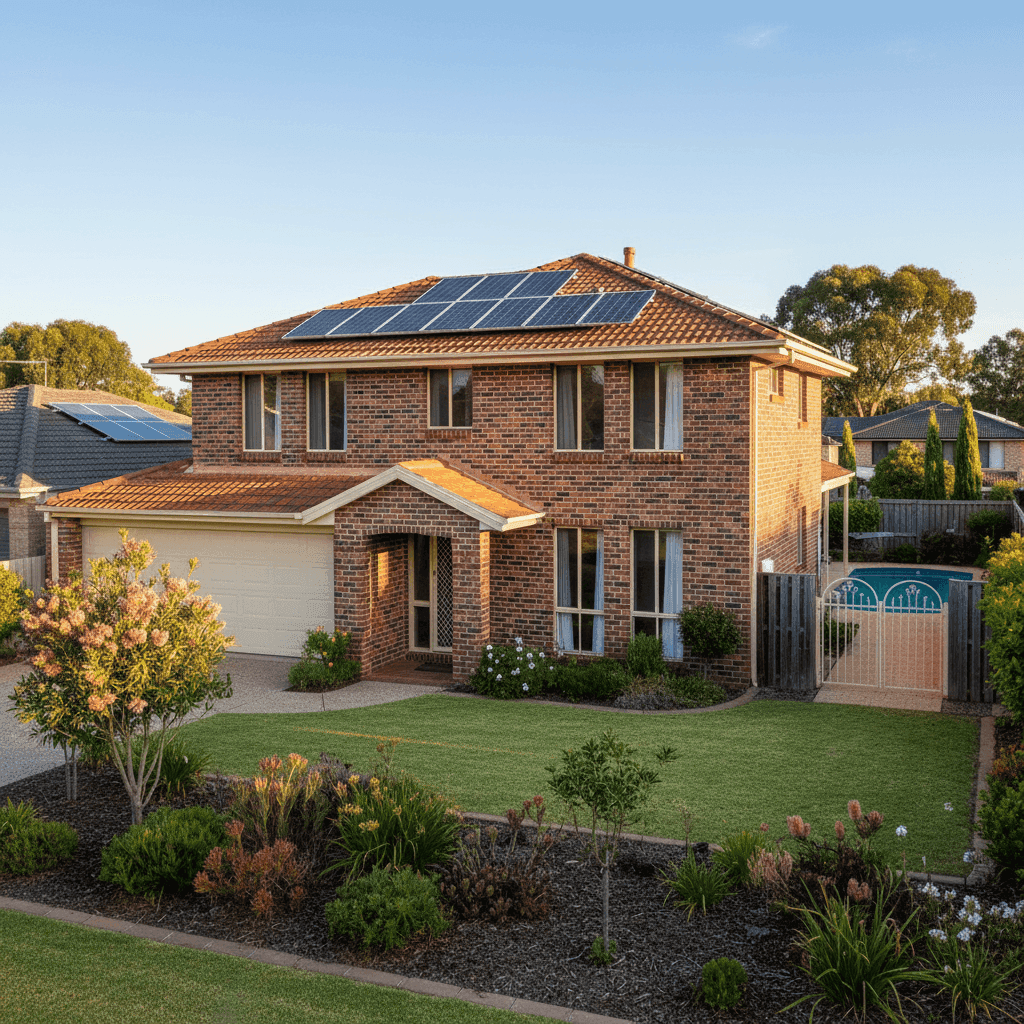

Double brick construction is generally viewed favourably by insurers. Brick homes are more resistant to fire, wind, and general wear than timber-framed alternatives, which can reduce premiums. However, double brick can also be more expensive to repair or rebuild after an event, which may partially offset that benefit at higher sums insured.

Tiled roof on a slab foundation is a solid, low-risk combination for Perth's climate. Tiles are durable and perform well in the heat, while slab foundations are straightforward to assess for structural integrity. Both features tend to support competitive pricing.

The $600,000 building sum insured is meaningful. For a 214 sqm home built in 1997, this reflects current rebuild costs in Perth's elevated construction market — labour and materials have increased sharply in recent years. A higher sum insured directly increases the premium, and underinsuring to save money can be a costly mistake if you ever need to make a claim.

The swimming pool adds liability and property risk. Pools require specific coverage for the structure itself, associated equipment (pumps, filtration), and public liability — all of which contribute to a higher base premium.

Solar panels are another factor. Panels are an asset worth protecting but also represent an additional replacement cost for insurers. Some policies include them automatically under building cover; others require specific endorsement. It's worth confirming exactly how your policy treats the panels.

Ducted climate control adds to the contents and building value, and systems like these can be expensive to repair or replace. Their presence supports a higher sum insured and, by extension, a higher premium.

---

Tips for Homeowners in Bennett Springs

1. Shop around before renewing The gap between the suburb's median ($914) and this quote ($1,703) is significant. Even if your property's features justify some loading, there's enough variance in the market to make comparison shopping worthwhile. Use CoverClub's quote comparison tool to see what multiple insurers would charge for the same property.

2. Review your sum insured annually Perth's construction costs have risen considerably. Make sure your $600,000 building sum insured reflects current rebuild costs — not the figure you set three years ago. Many insurers offer a sum insured calculator, or you can use a quantity surveyor's estimate for greater accuracy.

3. Ask about excess trade-offs The building excess on this policy is $2,500 — relatively high. Increasing your excess is one of the most effective ways to reduce your annual premium, but the $2,500 level already provides some discount. If cash flow allows, consider whether a higher excess (say, $5,000) could bring the premium down to a more competitive level.

4. Check your pool and solar panel coverage explicitly Don't assume these are covered. Ask your insurer directly: Is the pool shell covered? What about the pump and filtration equipment? Are solar panels included under building cover, and is there any exclusion for mechanical or electrical breakdown? Getting clarity now avoids nasty surprises at claim time.

---

Compare Your Home Insurance Quote Today

Whether you're renewing your policy or shopping for the first time, it pays to know where your premium stands relative to the market. CoverClub makes it easy to benchmark your quote against real data from homeowners in your suburb and across Australia.

Get a home insurance quote at CoverClub and see how your premium stacks up — in minutes, for free.