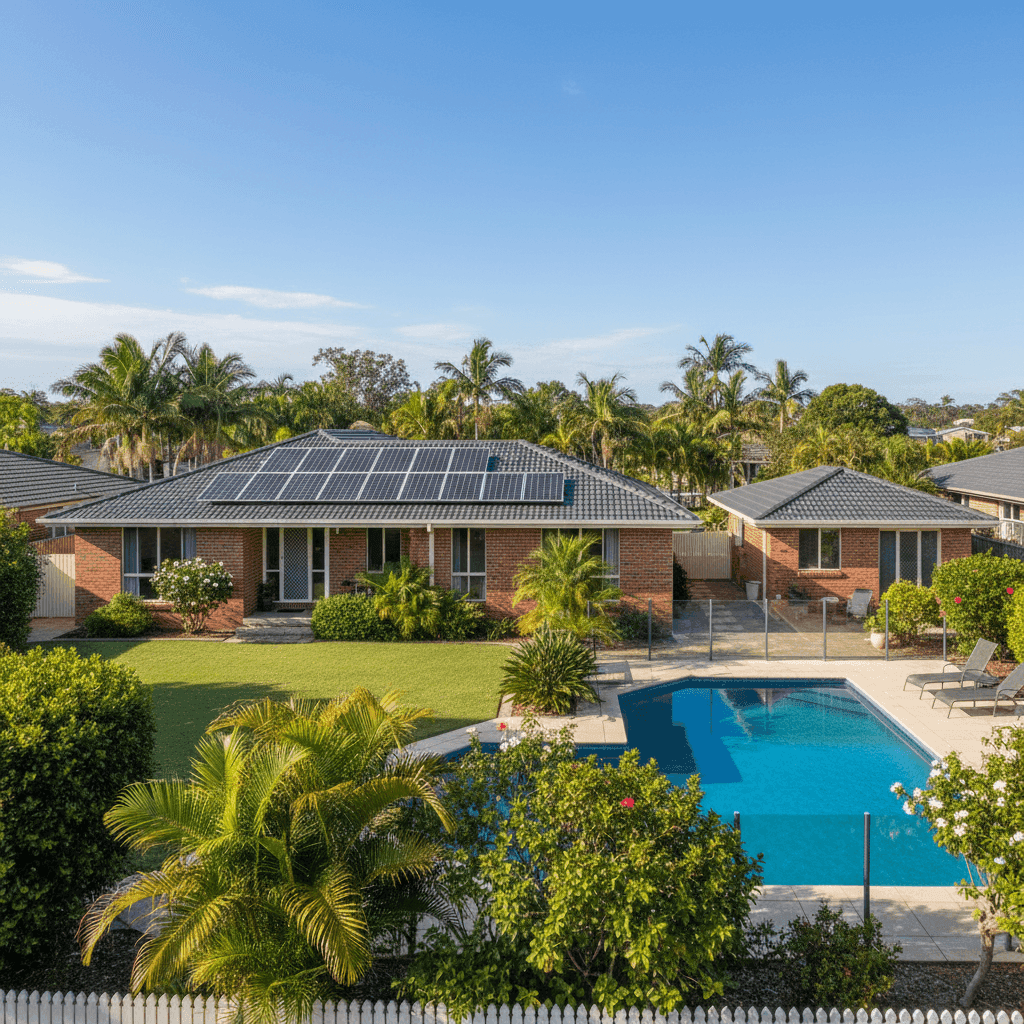

A five-bedroom free standing home in Benowa, QLD 4217 sits squarely in one of the Gold Coast's most sought-after residential pockets. With generous land, quality construction, and lifestyle features like a pool, solar panels, and a granny flat, properties here represent a significant financial asset — and protecting that asset with the right building insurance is essential. This article breaks down a recent building-only insurance quote for exactly this type of property, examines whether the premium stacks up against local and national benchmarks, and offers practical guidance for Benowa homeowners looking to get the best value from their cover.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,343 per year (or $235/month), with a $1,000 building excess. Based on CoverClub's pricing data, this quote is rated CHEAP — sitting below the suburb average, which is a strong result for a property of this size and specification.

To put that in perspective: the suburb average premium for Benowa is $5,081 per year, and the suburb median sits at $3,419 per year. This quote comes in well beneath even the 25th percentile of quotes collected in the area ($2,785/yr), meaning it's cheaper than at least 75% of comparable quotes in the postcode. That's a genuinely competitive outcome.

It's worth noting that "cheap" in insurance doesn't automatically mean "better" — policy inclusions, sub-limits, and exclusions vary significantly between insurers. But from a pure premium standpoint, this quote represents excellent value relative to the local market.

---

How Benowa Compares

Understanding where Benowa sits in the broader insurance landscape helps homeowners make more informed decisions. Here's how the numbers stack up:

| Benchmark | Premium |

|---|---|

| This Quote | $2,343/yr |

| Benowa Suburb Average | $5,081/yr |

| Benowa Suburb Median | $3,419/yr |

| Gold Coast LGA Average | $8,161/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 71 quotes collected in the Benowa area. View full [QLD insurance stats](https://coverclub.com.au/stats/QLD) or [national stats](https://coverclub.com.au/stats/national).)

A few things stand out here. The Gold Coast LGA average of $8,161/yr is notably high — driven in part by the significant proportion of coastal and flood-prone properties across the broader region. Benowa itself, being an inland suburb, tends to attract more moderate premiums. The QLD state average of $9,129/yr is heavily skewed by high-risk areas in Far North Queensland, cyclone-prone coastal zones, and flood-affected regions further west and north — so comparing purely to the state figure can be misleading for a Benowa homeowner.

Against the national median of $2,764/yr, this quote is actually slightly below — a solid result for a 315 sqm home with a pool, granny flat, and solar panels, all of which can add complexity (and cost) to a policy.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers price the risk. Here's what's likely working in this homeowner's favour — and what to keep an eye on.

Construction Type: Brick Veneer on Slab with Tiled Roof

Brick veneer walls and a tiled roof are among the most insurer-friendly combinations in Australia. Both materials are considered durable and fire-resistant, and they're widely used in Queensland suburban construction. A concrete slab foundation further reduces risk of subsidence or pest-related structural damage. Compared to properties with timber frames, fibro cladding, or corrugated iron roofing, this construction profile typically attracts lower premiums.

Age of Construction: 1996

Built in 1996, this home is approaching 30 years old — an age at which insurers may start factoring in the likelihood of ageing plumbing, electrical systems, or roofing. However, a well-maintained 1990s brick veneer home in Queensland is generally still considered low-to-moderate risk, and the construction standards of that era were solid.

Pool

A swimming pool increases the replacement cost of the property and introduces some liability considerations. Insurers typically factor pool reinstatement into the sum insured calculation, so it's important the $700,000 building sum insured adequately accounts for this.

Solar Panels

Solar panels are a growing consideration for insurers. They add to the replacement value of the building and can be a source of claims if damaged by hail or storms. Some policies cover solar panels automatically under building cover; others require them to be specifically listed. Homeowners should confirm their policy wording on this point.

Granny Flat

A secondary dwelling on the property adds significant value — and complexity. The $700,000 sum insured should reflect the full rebuild cost of both the main dwelling and the granny flat. Underinsurance is a common and costly mistake, so it's worth having both structures independently valued.

No Cyclone Risk

Benowa is not classified as a cyclone risk area, which meaningfully reduces premium loading compared to coastal and northern Queensland properties. This is one of the key reasons Benowa premiums tend to be more moderate than the Gold Coast LGA average.

Timber and Laminate Flooring

Timber and laminate floors can be more susceptible to water damage than tiles, which may have a minor influence on how insurers assess internal damage risk. This is more relevant for contents cover, but can occasionally factor into building assessments as well.

---

Tips for Homeowners in Benowa

1. Double-check your sum insured covers everything With a pool, granny flat, solar panels, and 315 sqm of living space, the rebuild cost of this property is substantial. The $700,000 sum insured may be appropriate, but it's worth getting an independent building valuation — or using an online calculator — to confirm you're not underinsured. Many Australians discover they're underinsured only at claim time, which can be financially devastating.

2. Confirm solar panel coverage in your policy Ask your insurer specifically whether solar panels are covered under the building policy, and whether there are any sub-limits. Some policies cap solar panel replacement at a set dollar amount, which may not reflect current market replacement costs.

3. Review your policy annually Building costs in Queensland have risen significantly in recent years due to supply chain pressures and labour shortages in the construction sector. A sum insured that was accurate two or three years ago may no longer reflect the true cost to rebuild. Make it a habit to reassess your coverage each renewal period.

4. Consider the value of a higher excess This policy carries a $1,000 excess, which is fairly standard. If you're comfortable self-insuring smaller claims, opting for a higher excess (e.g. $2,000–$2,500) can reduce your annual premium further — a useful lever if you're looking to cut costs without sacrificing core coverage.

---

Compare Your Own Quote

Whether you're a Benowa local or elsewhere on the Gold Coast, it pays to see how your current premium stacks up against the market. CoverClub aggregates real quote data from across Australia to help homeowners make smarter insurance decisions. Get a quote today at CoverClub and find out if you're paying a fair price — or if there's room to do better.