If you own a free standing home in Bentley Park, QLD 4869, you already know that insuring a property in Far North Queensland comes with its own set of considerations — cyclone season chief among them. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom weatherboard home in the suburb, and puts that premium under the microscope against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $4,785 per year (or $459 per month), covering both building and contents for a 235 sqm free standing home with a building sum insured of $985,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as Expensive — Above Average.

To put that in context: the average premium paid by homeowners in Bentley Park is $3,686 per year, and the suburb median sits at $3,541. That means this quote is running roughly $1,100 above the local average and about $1,244 above the median. It also sits above the suburb's 75th percentile of $4,276 — meaning it's more expensive than at least three-quarters of comparable quotes in the area.

That said, "expensive" is relative, and several property-specific factors help explain why this premium lands where it does. More on that shortly.

---

How Bentley Park Compares

Understanding your premium requires a bit of geographic context. Bentley Park sits within the Cairns Local Government Area, which carries an average premium of a staggering $12,404 per year — one of the highest in the country, driven almost entirely by cyclone risk. Against that LGA benchmark, a $4,785 premium actually looks quite reasonable.

Here's how the numbers stack up across different levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bentley Park (suburb) | $3,686/yr | $3,541/yr |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Cairns LGA | $12,404/yr | — |

A few things stand out here. Queensland's average premium of $9,129 is dramatically higher than its median of $3,903 — a sign that a subset of very high-risk properties (think beachfront or flood-prone areas) are pulling the average upward significantly. Bentley Park's own average of $3,686 is well below the QLD state average, suggesting it's a comparatively lower-risk pocket within the broader Cairns region.

Nationally, the average sits at $5,347, but again, the median of $2,764 tells a different story — most Australian homeowners are paying considerably less, with high-risk coastal and tropical areas skewing the figures upward.

You can explore full suburb-level data on the Bentley Park insurance stats page, or compare across the state on the Queensland insurance stats page. For a broader picture, the national stats page provides useful context.

---

Property Features That Affect Your Premium

Several characteristics of this particular home contribute to its above-average premium. Understanding these factors can help you make sense of the pricing — and potentially identify areas where you can negotiate or make changes.

Cyclone Risk Zone

This is the single biggest driver. Bentley Park falls within a designated cyclone risk area, which automatically triggers higher premiums from most insurers. Properties in Far North Queensland face a genuine and recurring threat from tropical cyclones, and insurers price that risk accordingly. There's no avoiding this factor — it's geographic — but it does mean shopping around is especially important, as insurers vary considerably in how they price cyclone exposure.

Weatherboard Timber Construction

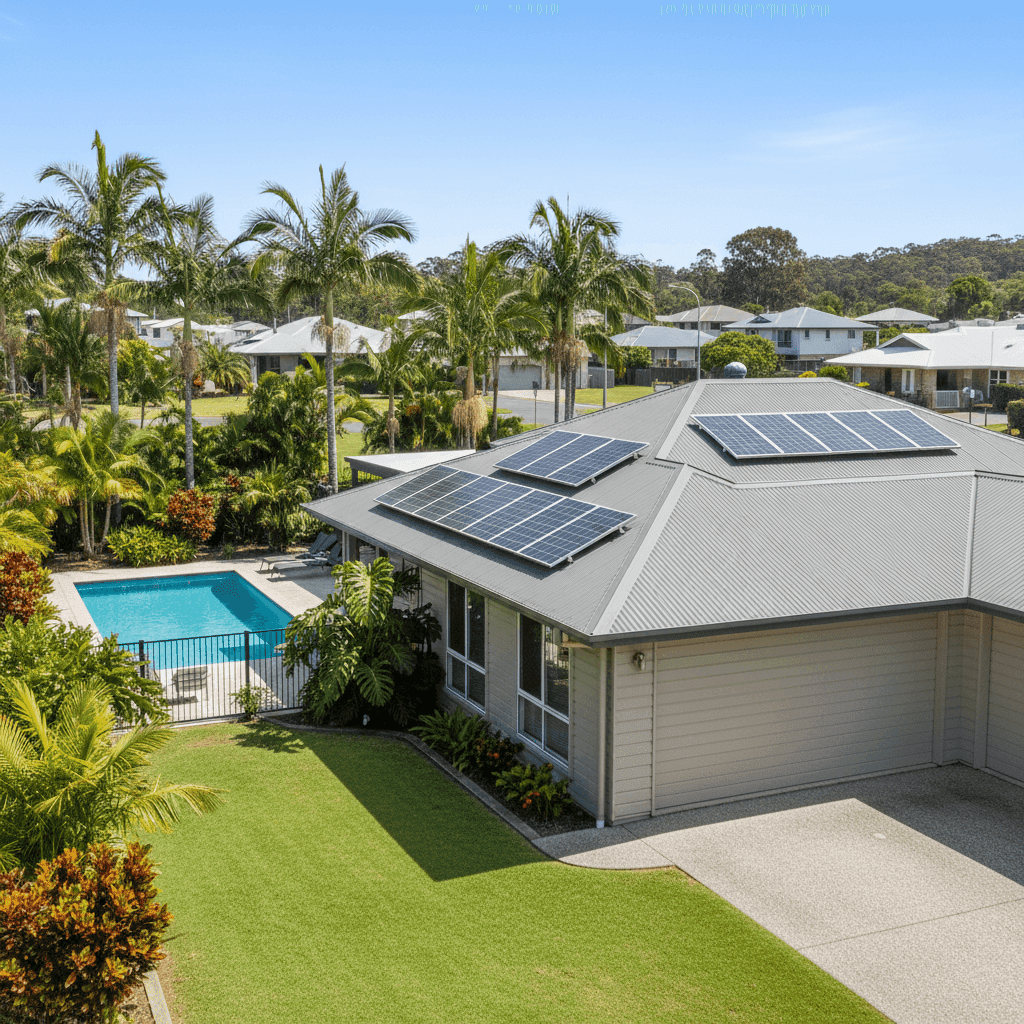

Weatherboard wood external walls are generally considered a higher-risk construction type compared to brick or rendered masonry. Timber is more susceptible to damage from high winds, moisture ingress, and fire — all of which are relevant in a tropical climate like Cairns. This construction type will push premiums higher with most insurers.

Swimming Pool

A pool adds both asset value and liability exposure to a property. Insurers factor in the cost of pool repairs or replacement, as well as the potential for accidental damage claims. It's a modest but real contributor to the overall premium.

Solar Panels

With $985,000 in building sum insured, the solar panel system is likely factored into the replacement cost. Solar panels can be damaged in hailstorms or cyclones, and their replacement cost is significant. Ensuring your sum insured accurately reflects the value of your solar system is important.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace, and in a tropical climate they work hard year-round. This adds to the overall building replacement cost and can influence the premium.

Building Sum Insured

At $985,000, the building sum insured is substantial for a 235 sqm home — though in a post-pandemic construction environment where building costs have surged, this may well reflect accurate replacement costs. Overinsuring can push premiums up unnecessarily, so it's worth getting a professional building valuation to confirm this figure is appropriate.

---

Tips for Homeowners in Bentley Park

1. Shop Around — Especially in Cyclone Zones

Insurers price cyclone risk very differently. Some use postcode-based models, others use more granular geographic data. A quote that's expensive with one insurer may be significantly cheaper with another for the exact same property. Use a comparison tool like CoverClub to get multiple quotes side by side.

2. Review Your Sum Insured Carefully

With building costs having risen sharply in recent years, it's tempting to set a high sum insured "just in case." But overinsuring means you're paying a higher premium than necessary. Consider commissioning a professional building replacement cost assessment to make sure your $985,000 sum insured is accurate — not inflated.

3. Ask About Cyclone Mitigation Discounts

Some insurers offer premium discounts for homes that have been cyclone-hardened — things like cyclone shutters, reinforced roofing, or compliance with updated building codes. A Colorbond steel roof (as this property has) is already a positive signal, but additional mitigation measures may unlock further savings.

4. Consider Your Excess Strategy

Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess — say, $2,500 or $5,000 — can meaningfully reduce your annual premium. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, this can be a smart way to lower ongoing costs.

---

Ready to Compare?

Whether you're renewing your current policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Head to CoverClub to get a tailored home and contents insurance quote for your Bentley Park property — and see how your premium stacks up against your neighbours.