If you own a free standing home in Berry Springs, NT 0838, you already know that insuring a property in the Northern Territory comes with its own set of considerations — from tropical weather patterns to the realities of living in a cyclone risk zone. This article breaks down a real home and contents insurance quote for a three-bedroom, three-bathroom property in Berry Springs, helping you understand whether the premium stacks up and what factors are driving the cost.

---

Is This Quote Fair?

The annual premium for this Berry Springs property comes in at $5,534 per year (or $530 per month), covering both building (sum insured: $800,000) and contents ($200,000), each with a $1,000 excess.

Our pricing model rates this quote as CHEAP — below average for the area. That's genuinely good news for the homeowner. Given the property's location in a designated cyclone risk zone and the relatively high building sum insured of $800,000, a sub-$5,600 annual premium represents solid value. Many comparable properties across the NT attract significantly higher premiums, particularly those with timber construction or elevated foundations that are more vulnerable to cyclone and flood damage.

For context, the NT state average premium sits at a steep $10,773 per year, meaning this quote is roughly 49% below the state average — a substantial saving. Even measured against the national average of $5,347 per year, this quote is only marginally above the country-wide figure, which is impressive given the elevated risk profile of NT properties generally.

---

How Berry Springs Compares

Understanding where your premium sits relative to broader benchmarks is key to evaluating any insurance quote. Here's how this property's premium measures up:

| Benchmark | Annual Premium |

|---|---|

| This Property | $5,534 |

| LGA (Litchfield) Average | $3,869 |

| NT State Median | $3,402 |

| NT State Average | $10,773 |

| National Median | $2,764 |

| National Average | $5,347 |

A few things stand out here. The NT state average of $10,773 is almost double the national average — a clear reflection of the elevated risk environment across much of the Territory, where cyclones, flooding, and extreme heat are genuine annual concerns rather than remote possibilities.

This quote sits above the Litchfield LGA average of $3,869 and the NT median of $3,402, which is expected given the higher-than-average sum insured values. A building insured for $800,000 and contents at $200,000 represent a total coverage of $1,000,000 — well above what many standard residential policies cover. Adjusting for that coverage level, the per-dollar cost of insurance here is very competitive.

No suburb-level data is currently available specifically for Berry Springs, but you can explore broader Berry Springs and NT 0838 insurance statistics as more data becomes available in our database.

---

Property Features That Affect Your Premium

Several characteristics of this property influence what insurers are willing to charge — for better and for worse.

✅ Factors Likely Keeping the Premium Down

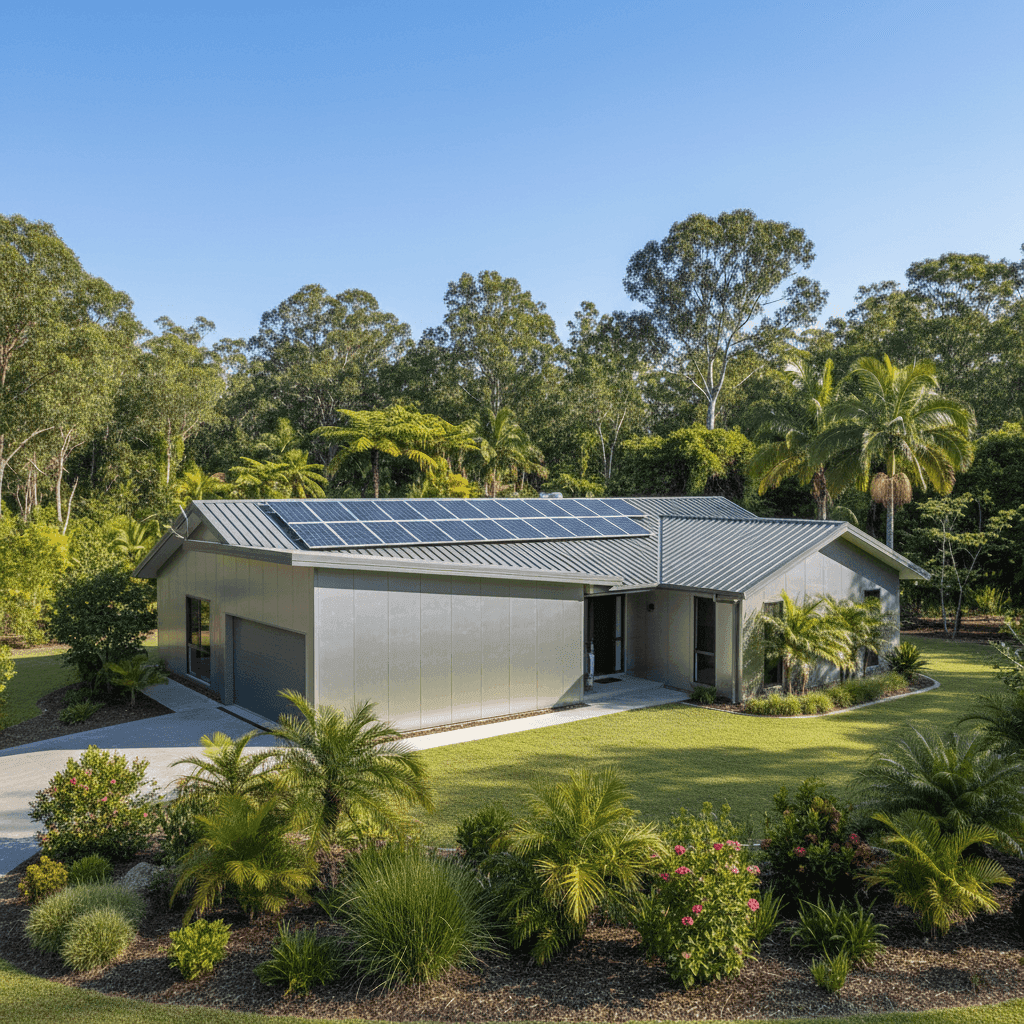

- Aluminium external walls are a strong positive from an insurer's perspective. Unlike timber, aluminium doesn't rot, isn't susceptible to termite damage (a serious concern in the NT), and performs reasonably well in high-wind events. This material choice likely contributes to the below-average rating.

- Steel/Colorbond roof is another favourable feature. Colorbond is widely regarded as one of the most cyclone-resilient roofing materials available in Australia, and insurers recognise this. It's durable, fire-resistant, and purpose-built for harsh Australian conditions.

- Concrete slab foundation provides structural stability and reduces the risk of underfloor flooding and pest ingress compared to raised or timber-framed stumped foundations.

- Tile flooring is durable and easy to replace, which lowers the cost of contents and building claims related to water damage.

- Built in 2009, the property benefits from construction standards that incorporate more modern cyclone-resilience requirements — particularly relevant for NT homes built after the lessons learned from Cyclone Tracy.

- Solar panels are present on the roof. While these can add a small amount of complexity to claims (panels need to be insured and may be at risk during severe weather), many insurers now accommodate them as standard.

⚠️ Factors That Add Risk

- Cyclone risk area is the single biggest risk factor for this property. Berry Springs is located in a region where tropical cyclones are a genuine seasonal threat. Insurers price this risk accordingly, and it's the primary reason NT premiums are so much higher than the national average.

- 169 sqm building size at an $800,000 sum insured implies a relatively high per-square-metre rebuild cost — around $4,730/sqm. This is on the higher end and may reflect quality fittings, remote location build costs, or both. It's worth periodically reviewing your sum insured to ensure it reflects current construction costs without over-insuring.

---

Tips for Homeowners in Berry Springs

1. Review Your Sum Insured Annually

Construction costs in the NT — particularly in more remote areas like Berry Springs — can shift significantly year to year. Make sure your $800,000 building sum insured keeps pace with actual rebuild costs. Underinsurance is a common and costly mistake; overinsurance means you're paying more than you need to.

2. Prepare a Cyclone Season Checklist

Insurers may reduce claim payouts if damage results from inadequate maintenance. Before each wet season, inspect your Colorbond roof for loose fixings, clear gutters, trim overhanging trees, and ensure your solar panel mounts are secure. Proactive maintenance can also support a smoother claims process if the worst happens.

3. Itemise High-Value Contents

With $200,000 in contents cover, it's worth maintaining a detailed home inventory — including photos and receipts for high-value items like electronics, jewellery, and appliances. This makes claims faster and reduces the risk of disputes over valuations.

4. Compare Quotes Before Renewal

Even a below-average premium can potentially be improved upon. Insurance markets shift, and the quote you received last year may not reflect today's competitive landscape. Use a comparison tool like CoverClub to benchmark your renewal offer before automatically rolling over your policy.

---

Find a Better Deal with CoverClub

Whether you're a first-time buyer or a long-term Berry Springs resident, comparing home and contents insurance quotes is one of the simplest ways to protect your finances. CoverClub makes it easy to see how your current premium stacks up against the market — and to find a policy that genuinely fits your property and budget. Get a quote today and see what you could be saving.