If you own a free standing home in Berwick, VIC 3806, you're likely well aware that home insurance is one of those non-negotiable costs of homeownership — but that doesn't mean you should pay more than necessary. In this article, we break down a real home and contents insurance quote for a four-bedroom property in Berwick, compare it against local and national benchmarks, and share practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,650 per year (or $259/month) for combined home and contents insurance, with a building sum insured of $1,000,000 and contents valued at $250,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the Berwick area.

To put that in context, the suburb average premium sits at $2,219 per year, and the median is even lower at $1,926 per year. This quote lands above the 75th percentile for Berwick, which is $2,574 — meaning it's pricier than roughly three-quarters of comparable quotes in the postcode.

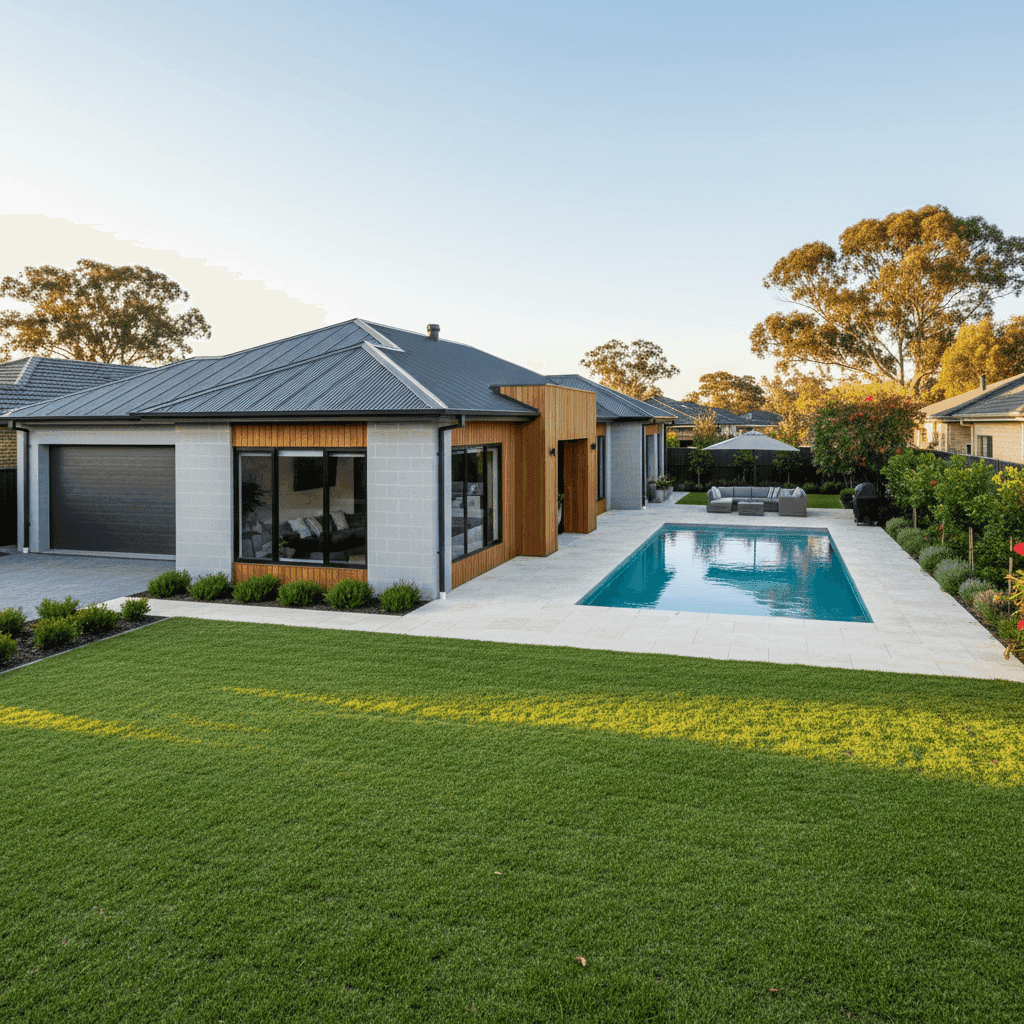

That said, it's worth noting that this is a well-appointed property. With 268 sqm of living space, three bathrooms, top-of-the-range fittings, a swimming pool, and ducted climate control, the risk profile and replacement cost are meaningfully higher than a more modest home. A $1,000,000 building sum insured is also on the higher end for the suburb, which will naturally push the premium up. So while the quote is above average, it's not necessarily unjustified given the property's characteristics.

---

How Berwick Compares

One of the most useful ways to assess any insurance quote is to zoom out and look at the broader picture. Here's how Berwick stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Berwick (3806) | $2,219/yr | $1,926/yr |

| Casey LGA | $2,142/yr | — |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

(Based on [Berwick suburb data](https://coverclub.com.au/stats/VIC/3806/berwick) from 148 quotes, [Victoria state data](https://coverclub.com.au/stats/VIC), and [national benchmarks](https://coverclub.com.au/stats/national).)

A few things stand out here. First, Berwick is actually a relatively affordable suburb to insure compared to the Victorian state average — homeowners here pay roughly $780 less per year on average than the typical Victorian. Nationally, the contrast is even more striking, with the national average premium sitting at $5,347 — more than double Berwick's suburb average. This is largely driven by high-risk areas in Queensland and northern Australia where cyclone, flood, and storm exposure pushes premiums sky-high.

The good news for Berwick residents is that the suburb sits in a non-cyclone risk area, which is a meaningful factor in keeping premiums relatively contained. At the LGA level, the City of Casey average of $2,142 per year is broadly in line with the Berwick suburb figure, suggesting consistent pricing across the local government area.

---

Property Features That Affect Your Premium

Not all homes are priced the same, and insurers look at a range of property characteristics when calculating your premium. Here's how the features of this particular home come into play:

- Hebel external walls: Hebel (autoclaved aerated concrete) panels are a popular modern cladding choice in Victoria. They offer good fire resistance and durability, which insurers generally view favourably compared to timber weatherboard. This can work in your favour at premium time.

- Steel/Colorbond roof: Colorbond is widely regarded as a low-maintenance, resilient roofing material. It performs well in storms and doesn't carry the same fire risk as some other materials. Insurers typically rate it positively.

- Concrete slab foundation: A slab foundation is considered stable and low-risk in most Victorian conditions, reducing concerns around subsidence or movement.

- Tiled flooring: Tiles are durable and straightforward to replace, and don't carry the same moisture or fire sensitivity as carpet or timber. This is generally a neutral-to-positive factor.

- Top-of-the-range fittings: This is where costs can climb. High-end fixtures, appliances, and finishes mean a higher cost to rebuild or replace — and insurers price accordingly. With top-of-the-range fittings across a 268 sqm home with three bathrooms, the replacement cost is genuinely elevated.

- Swimming pool: Pools add to the insured value of the property and introduce some additional liability considerations, which contributes to a higher premium.

- Ducted climate control: A full ducted system is a significant asset to insure, adding to both the building value and the complexity of any claim.

- No solar panels: Interestingly, this property doesn't have solar panels, which removes one potential source of complexity (solar systems can occasionally complicate roof claims).

Taken together, this is a high-specification home, and the $1,000,000 building sum insured reflects that. Homeowners with premium finishes and additional features like pools and ducted systems should expect their premiums to sit above the suburb median.

---

Tips for Homeowners in Berwick

Whether you're reviewing your current policy or shopping around for the first time, here are four practical steps to make sure you're getting the best value:

- Review your sum insured annually. Construction costs have risen significantly in recent years, and your building sum insured should reflect current rebuild costs — not just the market value of your home. Use a building cost calculator or speak with a quantity surveyor to make sure you're not underinsured. At the same time, being significantly over-insured on contents can unnecessarily inflate your premium.

- Compare multiple quotes. The spread between the 25th percentile ($1,467/yr) and 75th percentile ($2,574/yr) in Berwick shows there's real variation in what insurers charge for similar properties. Shopping around — or using a comparison platform like CoverClub — can surface meaningfully cheaper options without sacrificing cover quality.

- Consider your excess level. Both excesses on this quote are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can reduce your annual premium noticeably. This is a sensible strategy if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

- Check what's included for your pool and outdoor assets. Pools, pool equipment, and outdoor entertaining areas can sometimes be excluded or have sub-limits under standard policies. Make sure your policy explicitly covers these assets, particularly for storm damage or accidental damage scenarios — both relevant risks in suburban Melbourne.

---

Ready to Compare?

Whether this quote is right for your situation depends on your specific property, risk appetite, and budget. The best way to know if you're getting a fair deal is to compare. At CoverClub, you can run your own quote for your Berwick home and see how it stacks up against the market. It takes just a few minutes and could save you hundreds of dollars a year.

Explore more Berwick home insurance data, browse Victoria-wide stats, or check out national home insurance benchmarks to keep building your knowledge.