Nestled in the heart of central Victoria, Bet Bet (VIC 3472) is a quiet rural locality in the Mount Alexander local government area. If you own a free standing home here, understanding what you should be paying for home and contents insurance is an important step toward protecting your asset — and your budget. In this article, we break down a real insurance quote for a 2-bedroom, 1-bathroom free standing home in Bet Bet, compare it against Victorian and national benchmarks, and offer practical tips to help local homeowners get the best value from their cover.

---

Is This Quote Fair?

The quote in question comes in at $2,652 per year (or $259/month) for combined home and contents insurance, with a building sum insured of $580,000 and contents valued at $30,000. Both the building and contents excess are set at $1,000.

Our pricing engine rates this quote as Fair — Around Average, and the numbers back that up. At $2,652 annually, this premium sits:

- Below the VIC state average of $3,000/yr

- Just under the VIC state median of $2,718/yr

- Well below the national average of $5,347/yr

- Slightly below the national median of $2,764/yr

In short, this is a reasonable premium — not a bargain, but not overpriced either. The policyholder is paying close to the middle of the road for Victoria, which is a solid outcome given the property's characteristics. There is still some room to potentially reduce costs by adjusting cover settings or shopping around, but there's no immediate cause for alarm.

---

How Bet Bet Compares

Without suburb-specific data available for Bet Bet, we can still draw meaningful comparisons using VIC state-level data and national benchmarks.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,652 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

| Mount Alexander LGA Average | $3,847 |

One figure that stands out is the Mount Alexander LGA average of $3,847/yr — significantly higher than this quote. That gap of nearly $1,200 per year suggests that either this property has favourable risk characteristics, or the insurer has priced it competitively relative to others in the region. Either way, it's a meaningful saving compared to what many neighbours in the LGA may be paying.

Compared to the national average of $5,347, the quote looks especially attractive — though it's worth noting that national averages are heavily influenced by high-risk areas in Queensland and Western Australia, particularly cyclone-prone coastal regions. Still, for a Victorian property, landing below both the state and LGA averages is a positive sign.

You can explore more localised pricing data for the area at the Bet Bet suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess risk and calculate the premium.

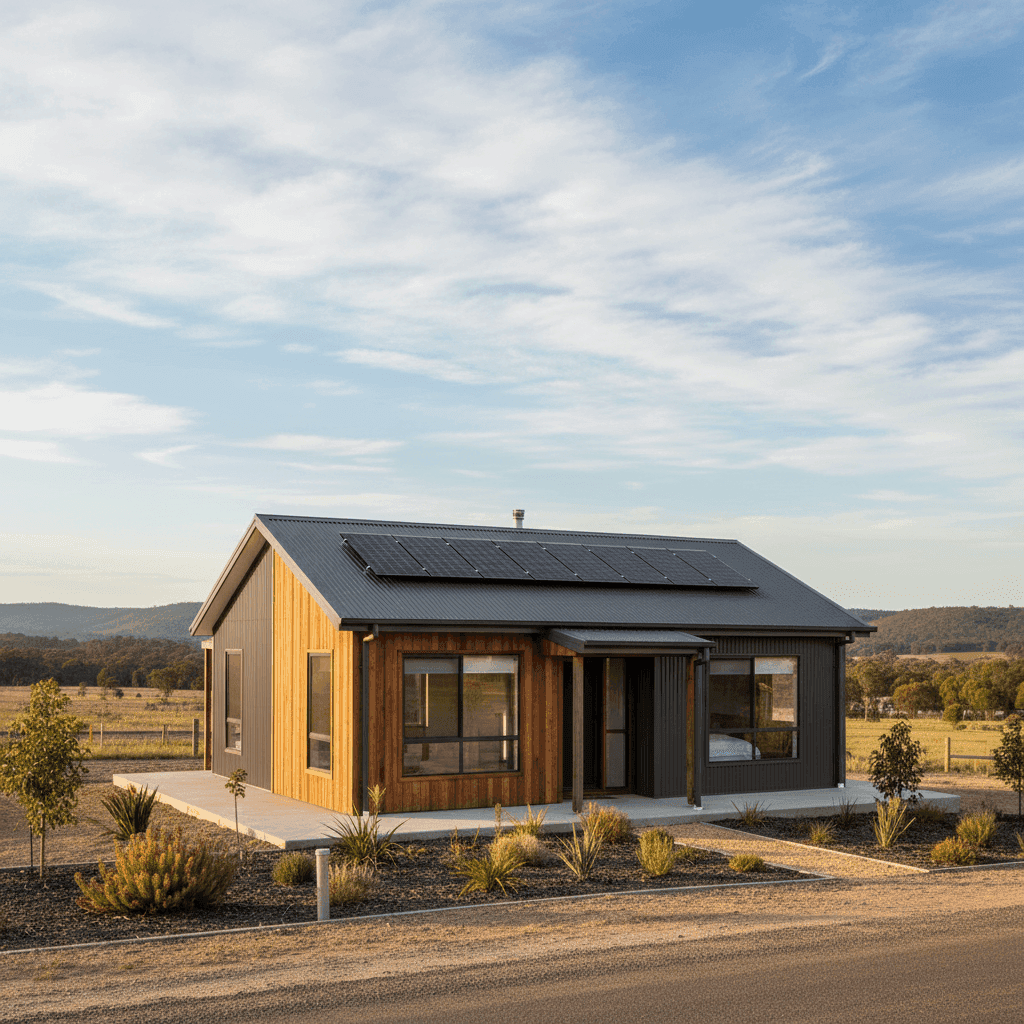

Steel/Colorbond Roof

A steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to older tiled or timber roofing. This likely contributes to a more competitive premium.

Slab Foundation

A concrete slab foundation is a stable, well-understood building type for insurers. It's less susceptible to movement and subsidence issues compared to older stumped or pier foundations, which can reduce risk in the eyes of underwriters.

Solar Panels

The property includes solar panels, which are an increasingly common feature across Australian homes. Most insurers cover solar panels as part of the building sum insured, though it's worth confirming this with your insurer. Some policies may require panels to be specifically listed, particularly if they are a high-value system.

Ducted Climate Control

Ducted climate control is classified as a fixed building feature and is typically included in the building sum insured. It adds to the replacement cost of the home, which is reflected in the $580,000 building sum insured — a figure that should be regularly reviewed to ensure it keeps pace with rising construction costs.

Above-Average Fittings Quality

The property's above-average fittings — think quality kitchen and bathroom fixtures, flooring, and finishes — contribute to a higher replacement cost. This is appropriately reflected in the building sum insured and is a key reason why underinsurance is a risk for well-appointed homes. Cutting corners on your sum insured to reduce your premium could leave you significantly out of pocket after a major claim.

Slight Elevation

At less than 1 metre of elevation, this property sits marginally above ground level. While this modest elevation offers minimal flood mitigation benefit, it's worth noting for properties in areas with any surface water risk.

Carpet Flooring

Carpet is a common flooring type but can be more vulnerable to water damage than hard flooring alternatives. This is worth keeping in mind if you're in an area with any history of localised flooding or burst pipe incidents.

---

Tips for Homeowners in Bet Bet

1. Review Your Building Sum Insured Annually

Construction costs in regional Victoria have risen sharply in recent years. The $580,000 sum insured may be appropriate today, but it's worth reassessing each year — ideally using a building cost calculator — to make sure you're not underinsured. Rebuilding costs in rural areas can be higher than expected due to transport and labour factors.

2. Confirm Solar Panel Coverage

With solar panels on the roof, double-check your policy wording to confirm they are explicitly covered under the building definition. Ask your insurer whether storm damage, hail, and electrical faults are included. If your system is a larger capacity installation, you may need to ensure the sum insured adequately accounts for replacement.

3. Consider Increasing Your Excess to Lower Your Premium

At $1,000, the current excess is fairly standard. If you have emergency savings available and rarely make small claims, raising your excess to $1,500 or $2,000 could reduce your annual premium meaningfully. Just make sure the saving justifies the increased out-of-pocket cost in a claim scenario.

4. Shop Around at Renewal Time

Even with a fair-rated premium, it pays to compare quotes before your policy renews. Insurers regularly reprice their books, and a competitor may offer equivalent cover at a lower rate — or better cover at the same price. Use a comparison platform like CoverClub to benchmark your renewal quote against the market each year.

---

Ready to Compare Home Insurance in Bet Bet?

Whether you're reviewing an existing policy or shopping for cover for the first time, CoverClub makes it easy to see how your quote stacks up. Compare home and contents insurance options tailored to your property and budget — get a quote today at CoverClub and make sure you're not paying more than you need to.