If you own a free standing home in Beverley, WA 6304, you've probably noticed that home insurance in regional Western Australia can feel like a bit of a moving target. Premiums vary widely depending on your property's construction, location risk profile, and the level of cover you choose. In this article, we break down a real home and contents insurance quote for a 3-bedroom, 2-bathroom property in Beverley — and put it in context against what others in the suburb, across WA, and nationally are paying.

---

Is This Quote Fair?

The quote in question comes in at $4,941 per year (or $476/month) for combined home and contents cover, with a building sum insured of $550,000 and contents valued at $50,000. The building excess is $3,000, and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average, which is a reasonable result worth unpacking.

Based on 27 quotes collected for Beverley (6304), the suburb's average annual premium sits at $6,518, with a median of $5,315. This particular quote falls comfortably below both benchmarks — and sits between the 25th percentile ($4,429/yr) and the 75th percentile ($6,123/yr). In practical terms, that means this homeowner is paying less than roughly half of their neighbours for comparable cover, which is a solid outcome.

That said, "fair" doesn't mean "the best available." There may still be room to sharpen the premium further, particularly given some of the property's favourable characteristics (more on those below).

---

How Beverley Compares

One of the most striking aspects of this quote is just how much more Beverley residents pay compared to broader benchmarks:

| Benchmark | Average Premium |

|---|---|

| Beverley (6304) suburb average | $6,518/yr |

| Beverley (6304) suburb median | $5,315/yr |

| LGA (Beverley) average | $4,359/yr |

| WA state average | $2,144/yr |

| WA state median | $1,944/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

The gap between Beverley's suburb average ($6,518) and the WA state average of $2,144 is substantial — Beverley homeowners are paying roughly three times more than the typical Western Australian. Compared to the national average of $2,965, the difference is still more than double.

This premium loading reflects the realities of insuring property in a regional inland location. Factors like distance from fire services, bushfire exposure in the Wheatbelt region, and the cost of sourcing tradespeople and materials for repairs in a remote area all contribute to elevated base rates. Insurers price these risks into their models, and regional WA communities like Beverley tend to bear that cost.

The LGA average of $4,359 is notably lower than the suburb average of $6,518, which suggests there's meaningful variation even within the Beverley local government area — likely driven by differences in property type, construction materials, and individual risk profiles.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how they stack up:

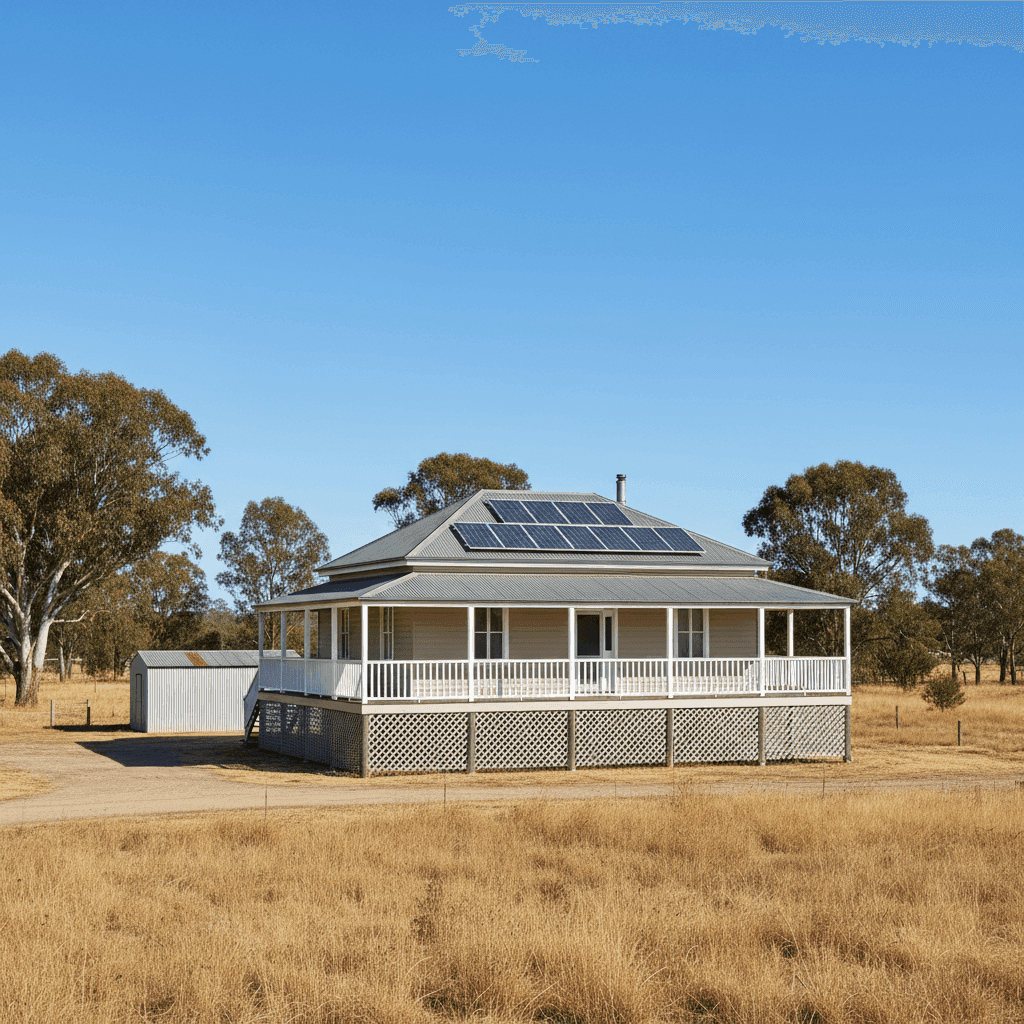

Weatherboard timber external walls are a significant rating factor. Timber-framed homes are considered higher risk for fire and more susceptible to weather-related damage than brick or rendered masonry. In a region like the Wheatbelt, where bushfire risk is a real consideration, this construction type typically attracts a premium loading compared to brick veneer or double brick homes.

Steel/Colorbond roofing is generally viewed favourably by insurers. Colorbond is durable, low-maintenance, and performs well in high-wind and hail events. It's a common and practical choice in regional WA and tends not to add material cost to a premium.

Stump foundations (elevated by at least 1 metre) add complexity to the risk profile. On one hand, elevation can reduce flood and moisture damage risk. On the other, elevated homes can be more vulnerable to wind uplift and may cost more to repair due to access requirements. Insurers treat this differently depending on the specific policy wording.

Solar panels are increasingly common and most insurers now include them under building cover, though it's worth confirming this is the case with your specific policy. They add to the overall replacement cost of the structure, which is reflected in the $550,000 sum insured.

Ducted climate control is classified as a building fixture and is typically covered under the building component of a home and contents policy. Like solar panels, it contributes to the overall rebuild cost.

Vinyl flooring is a practical and cost-effective choice that doesn't meaningfully inflate the contents or building sum insured, and it's relatively straightforward to replace in the event of a claim.

No pool, no cyclone risk area — both of these work in the homeowner's favour. Pool liability adds complexity and cost, and the absence of a cyclone risk designation (common in northern WA) keeps the premium from being pushed into a higher bracket.

The property was built in 2019, which is a positive signal for insurers. Newer builds comply with modern construction standards, are less likely to have ageing electrical or plumbing systems, and generally present a lower claims risk than older homes.

---

Tips for Homeowners in Beverley

1. Review your sum insured annually With construction costs rising across Australia, it's easy for your building sum insured to fall behind the actual cost of rebuilding. A $550,000 sum insured may be appropriate today, but it's worth checking against current building cost estimates each year — particularly for a timber-framed home where material and labour costs in a regional area can be significant.

2. Consider your excess strategy This policy carries a $3,000 building excess and a $1,000 contents excess. Opting for a higher excess is one of the most effective ways to reduce your annual premium, but make sure the excess amount is one you could genuinely cover out of pocket in the event of a claim. Revisit this balance each renewal.

3. Compare quotes at every renewal The insurance market in regional WA is competitive, and premiums can shift meaningfully from year to year. Don't let your policy auto-renew without running a comparison first. Even a "fair" quote can become an expensive one if you haven't checked what else is available.

4. Protect your timber exterior Beyond insurance, maintaining your weatherboard walls — keeping paint sealed, repairing any rot or damage promptly, and ensuring gutters are clear — can help reduce the likelihood of a claim and may support a better claims outcome if something does go wrong. Some insurers also reward proactive maintenance with more favourable terms at renewal.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing an existing policy or insuring a new property, it pays to see what the market has to offer. CoverClub makes it easy to compare home and contents insurance quotes for properties across Beverley and the broader WA region — so you can make an informed decision rather than simply accepting whatever lands in your inbox at renewal time. Start your comparison today and find out if you're getting the best deal available for your home.