Bexley is a well-established suburb in Sydney's inner south, sitting within the Bayside local government area. It's a mix of older character homes and newer builds, with tree-lined streets and easy access to the CBD. For owners of a free standing home in this suburb, understanding what drives your home insurance premium — and whether you're paying a fair price — can make a real difference to your household budget.

This article breaks down a recent building-only insurance quote for a five-bedroom, three-bathroom free standing home in Bexley, NSW 2207, and puts it in context against local, state and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium for this property is $4,637 per year (or $444 per month), covering the building only at a sum insured of $968,000 with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average.

To understand why, it helps to look at the numbers. The suburb average premium in Bexley sits at $1,800 per year, with a median of $1,245. This quote comes in at more than 2.5 times the suburb average and nearly four times the median — a significant gap that warrants a closer look.

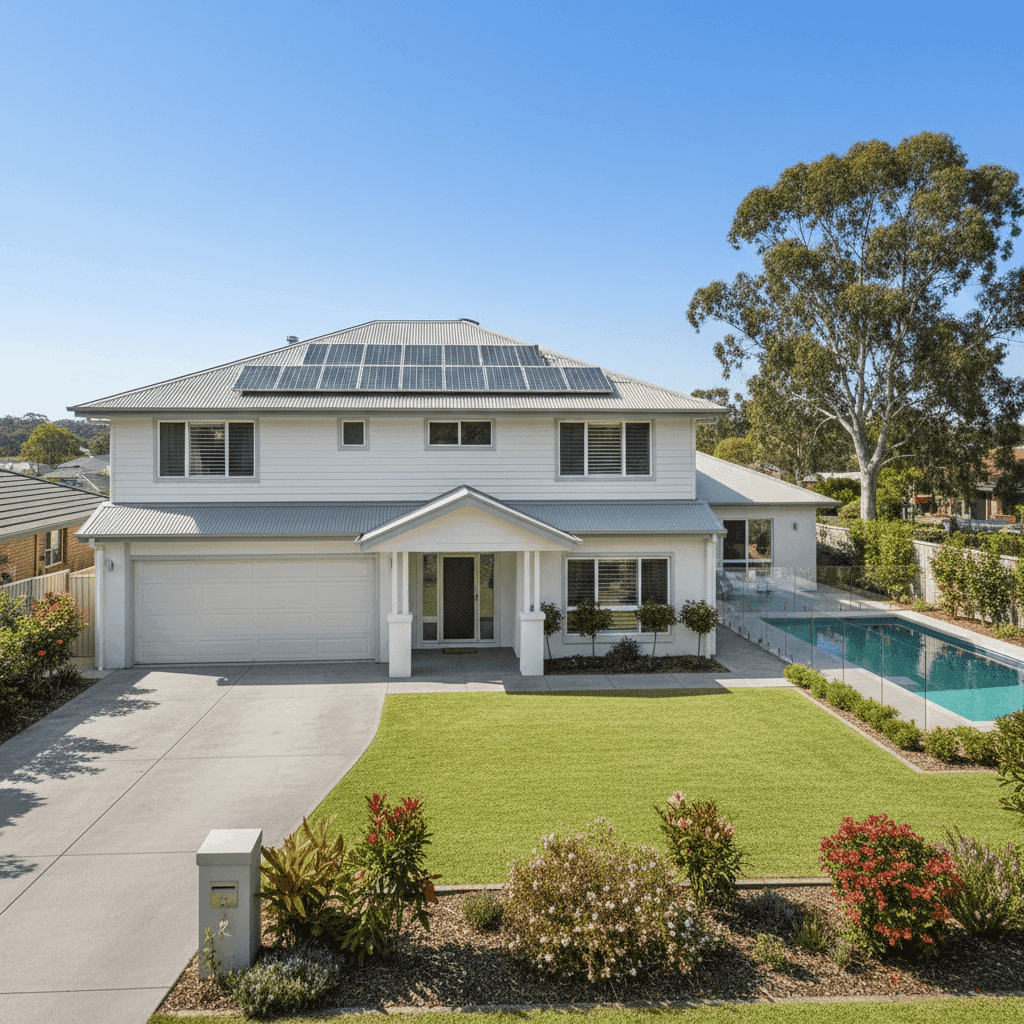

That said, price comparisons need to be made carefully. The suburb sample in our dataset is relatively small (14 quotes), which means the averages can shift considerably with just a handful of high or low outliers. It's also worth noting that this property has several features — a pool, solar panels, ducted climate control, a large 315 sqm building footprint, and fibro asbestos external walls — that can each push premiums upward. We'll unpack those shortly.

---

How Bexley Compares

Here's how this quote stacks up across different geographic benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bexley (NSW 2207) | $1,800/yr | $1,245/yr |

| Bayside LGA (NSW) | $2,954/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528 is notably high — driven largely by properties in flood-prone, bushfire-affected or cyclone-risk regions that attract very steep premiums. This quote of $4,637 is actually below the NSW state average, which provides some reassurance.

When compared to the national average of $5,347, this quote sits just under — again, not unreasonable in absolute terms. However, against the Bexley suburb average and median, the gap is harder to ignore. The 75th percentile for the suburb is $2,451, meaning this quote is above even the most expensive quarter of local properties in our dataset.

The Bayside LGA average of $2,954 also sits well below this quote, suggesting that even within the broader local government area, this premium is on the higher end.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a higher-than-average premium:

Fibro Asbestos External Walls

This is arguably the most significant premium driver. Homes with fibro asbestos cladding are treated as higher risk by most insurers because repairs and rebuilds must comply with strict asbestos handling regulations. Licensed removal and disposal adds substantial cost to any claim involving the external walls, and insurers price this in accordingly.

Building Size and Sum Insured

At 315 sqm and a sum insured of $968,000, this is a large home with a high rebuild value. Premium is directly correlated with the cost to rebuild — a bigger sum insured means a bigger potential payout, and that's reflected in the price.

Swimming Pool

Pools increase the insurable value of a property and introduce additional liability considerations. They also add to the complexity and cost of a rebuild, which insurers factor into their calculations.

Solar Panels

Solar systems are now a standard feature on many Australian homes, but they do add to the replacement cost of a property. A ducted climate control system adds further to the building's complexity and value.

Stump Foundation

Homes on stumps (also called pier and beam foundations) can be more susceptible to movement, subsidence and moisture-related damage than slab foundations. Some insurers view this as a slightly elevated risk, particularly in older builds — though this property was constructed in 2014, which is reassuring.

Colorbond Steel Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant and low-maintenance compared to terracotta or concrete tiles, and this may help moderate the premium to some degree.

---

Tips for Homeowners in Bexley

1. Get multiple quotes and compare carefully With a premium this far above the suburb median, it's well worth shopping around. Different insurers assess risk differently — particularly for properties with asbestos materials — and the spread between quotes can be significant. Use CoverClub to compare quotes side by side.

2. Review your sum insured regularly A sum insured of $968,000 is substantial. Make sure this figure reflects the actual cost to rebuild your home (not its market value), including demolition, asbestos removal, and current construction costs in Sydney. Over-insuring pushes your premium up unnecessarily, while under-insuring leaves you exposed at claim time.

3. Ask about asbestos-specific policy conditions Not all policies handle asbestos the same way. Some may exclude certain asbestos-related costs or impose sub-limits on removal. Before committing to a policy, read the Product Disclosure Statement (PDS) carefully or ask your insurer directly how asbestos is treated in the event of a claim.

4. Consider your excess strategy This quote carries a $1,000 building excess. Opting for a higher voluntary excess — say, $2,500 or $5,000 — can meaningfully reduce your annual premium. If your property is well-maintained and you're unlikely to make small claims, a higher excess may be a smart trade-off.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, it pays to know what you're actually getting for your money. CoverClub makes it easy to compare home insurance quotes across multiple providers, so you can see at a glance whether your current premium is competitive — or whether there's a better deal waiting.

Get a home insurance quote for your Bexley property today and see how your options stack up.