Bidwill is a quiet residential suburb in the Gympie region of Queensland, and like many communities across the Sunshine State, homeowners here face a wide range of insurance costs depending on their property's characteristics and location. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Bidwill (QLD 4650) — and puts that number in context so you can judge whether your own policy is working hard enough for you.

---

Is This Quote Fair?

The annual premium for this property came in at $3,046 per year (or $285 per month), covering a building sum insured of $500,000 and contents valued at $97,000, each with a $500 excess. Our pricing engine rates this quote as CHEAP — below average for the area.

That's genuinely good news for this homeowner. In a state where insurance costs have been climbing sharply in recent years, landing below the average benchmark is a meaningful win. The "cheap" rating doesn't suggest the cover is thin or inadequate — it simply means the premium is competitive relative to comparable properties and risk profiles. For a combined home and contents policy with solid sum insured figures, $3,046 per year represents real value.

That said, "cheap" is always relative. It's worth understanding why this property attracts a lower-than-average premium, and whether that pricing will hold at renewal or shift as insurers recalibrate their risk models.

---

How Bidwill Compares

To understand whether $3,046 is genuinely competitive, it helps to look at the broader landscape. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $3,046/yr |

| QLD state median | $3,903/yr |

| QLD state average | $9,129/yr |

| LGA (Gympie) average | $5,581/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

A few things stand out immediately. The Queensland state average of $9,129 per year is extraordinarily high — a figure heavily skewed by properties in cyclone-prone coastal and far-north Queensland regions, where insurers price in significant catastrophe risk. The median of $3,903 is a more useful comparison for most homeowners, and this quote sits comfortably below it.

Compared to the Gympie LGA average of $5,581 per year, the $3,046 quote is nearly 45% cheaper — a substantial difference that reflects the relatively benign risk profile of this particular property. Against the national median of $2,764, the quote is only modestly higher, which is impressive given that Queensland properties generally attract higher premiums than the national norm due to weather-related risks.

The takeaway: this is a genuinely competitive quote, not just by local standards but nationally.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — every feature of a home feeds into the risk calculation. Here's how the characteristics of this Bidwill property likely influenced the premium:

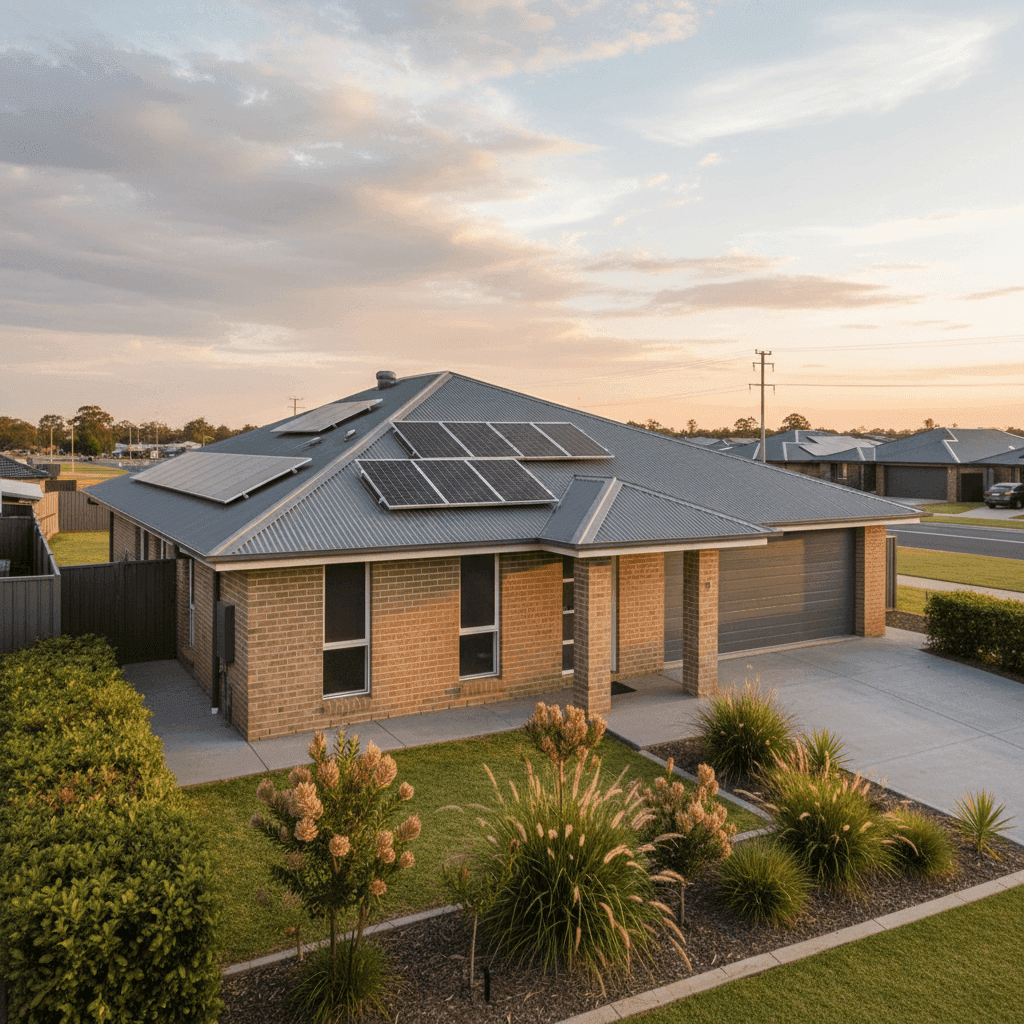

Brick Veneer Walls Brick veneer is one of the more favoured construction types among insurers. It offers solid fire resistance and structural durability without the full cost of double-brick construction. Compared to timber-framed or weatherboard homes, brick veneer typically attracts lower premiums.

Steel / Colorbond Roof Colorbond steel roofing is highly regarded for its resilience in Australian conditions — resistant to fire, rot, and corrosion. Insurers generally view it favourably, and it's a common choice in regional Queensland for good reason.

Concrete Slab Foundation A slab foundation reduces the risk of subsidence and pest-related structural damage compared to raised or timber-stumped foundations. This is another feature that tends to work in a homeowner's favour at premium time.

Construction Year: 1988 Homes built in the late 1980s sit in an interesting middle ground. They're old enough that some wear is expected, but they were built under reasonably modern building codes. At 214 sqm, this is a well-sized home, and the building sum insured of $500,000 appears appropriate for full replacement in today's construction market.

Solar Panels Solar panels add value to a property but also introduce a small additional risk — they need to be covered for damage from storms, hail, or electrical faults. Most comprehensive home policies include solar panels under the building cover, which is worth confirming with your insurer.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and are typically covered under building insurance. Their presence can marginally increase the sum insured required, but they don't dramatically shift premiums on their own.

No Pool, No Cyclone Zone The absence of a swimming pool removes a liability and maintenance risk that some insurers price in. More significantly, Bidwill falls outside designated cyclone risk areas — a major factor in keeping this premium well below the Queensland state average.

Tile Flooring & Standard Fittings Tile flooring is durable and relatively inexpensive to repair or replace compared to timber or high-end stone finishes. Standard fittings across the home keep the contents and building replacement costs predictable, which insurers tend to reward with more competitive pricing.

---

Tips for Homeowners in Bidwill

Even with a competitive quote in hand, there's always room to optimise your cover and your costs.

1. Review Your Sum Insured Annually Construction costs in regional Queensland have risen significantly in recent years. A $500,000 building sum insured may be appropriate today, but it's worth checking against current building cost calculators each year at renewal to avoid being underinsured. Your insurer won't automatically adjust for inflation unless you have an indexed policy.

2. Don't Underestimate Your Contents At $97,000, the contents value in this quote is reasonable for a three-bedroom home — but it's easy to undercount. Go room by room and include whitegoods, electronics, furniture, clothing, and outdoor equipment. Many homeowners discover they're underinsured for contents only after a claim.

3. Confirm Solar Panel Coverage With solar panels on the roof, check your policy documents carefully. Confirm that your panels are covered for physical damage (storm, hail, impact) and that any associated inverter or battery storage system is also included. Some policies treat these as separate items.

4. Compare at Every Renewal A "cheap" rating today doesn't guarantee the same result next year. Insurers adjust their pricing models regularly, and loyalty doesn't always pay. Use a comparison platform like CoverClub at each renewal to make sure you're still getting a competitive rate — it only takes a few minutes and could save you hundreds.

---

Ready to Compare Your Options?

Whether you're a Bidwill local or considering a move to the Gympie region, it pays to know exactly what you should be paying for home and contents insurance. CoverClub makes it easy to compare real quotes from multiple insurers in minutes — no jargon, no pressure, just clear pricing you can act on.

Get a home insurance quote at CoverClub and see how your current policy stacks up.