Biggera Waters, nestled on the northern Gold Coast waterway, is a popular suburb for families and retirees alike — and with that desirability comes a real need to protect your biggest asset. This article breaks down a recent building insurance quote for a four-bedroom, three-bathroom free standing home in Biggera Waters (QLD 4216), comparing it against local, state, and national benchmarks to help you understand what's fair, what's expensive, and what you can do about it.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote came in at $2,427 per year (or $233/month) for building-only cover on a 244 sqm double brick home insured for $844,000. Our price rating for this quote is CHEAP, meaning it sits well below the average for the area.

To put that in perspective, the suburb average premium in Biggera Waters is $6,628/year — meaning this quote is roughly 63% cheaper than what most homeowners in the same postcode are paying. Even against the suburb's median of $5,287/year, the saving is substantial. For a homeowner who shops around and lands a quote like this, the annual saving compared to the suburb average could be well over $4,000 — money that stays in your pocket rather than going to an insurer.

That said, it's worth understanding why a quote might be this competitive. Insurers price risk based on a combination of property characteristics, claims history, and local risk factors. When a quote lands in the "cheap" category, it often means the property presents a lower-than-average risk profile — or that the insurer is particularly competitive for this type of home. Either way, it's a result worth celebrating, but also worth scrutinising to make sure the cover is adequate.

---

How Biggera Waters Compares

Biggera Waters is one of the pricier suburbs to insure in Queensland, and the data reflects that clearly. Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,427 |

| Biggera Waters 25th Percentile | $4,045 |

| Biggera Waters Median | $5,287 |

| Biggera Waters Average | $6,628 |

| Biggera Waters 75th Percentile | $8,728 |

| Gold Coast LGA Average | $5,494 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

Based on 41 quotes collected for the Biggera Waters area, premiums vary enormously — from around $4,045 at the lower end to $8,728 at the 75th percentile. This wide spread is typical of coastal Gold Coast suburbs, where flood zones, storm surge risk, and proximity to waterways can dramatically influence what insurers charge.

Interestingly, this quote even beats the national average of $2,965/year — a remarkable result for a Gold Coast property, where premiums tend to run hot. Queensland as a whole averages $4,547/year, reflecting the state's elevated exposure to cyclones, flooding, and severe storms. Landing below the national average in this context is genuinely impressive.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its competitive premium:

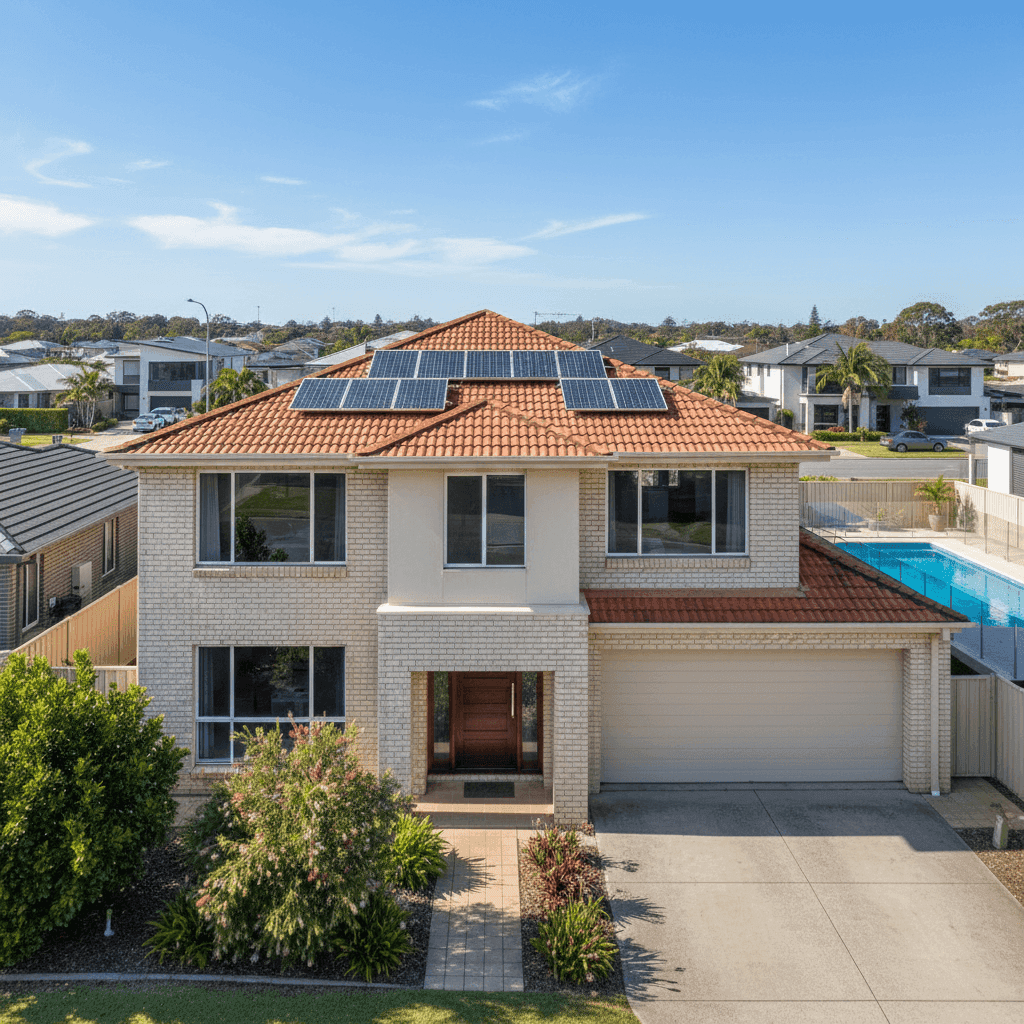

Double Brick Construction Double brick is one of the most resilient wall materials available. It performs well against wind, fire, and impact — all key risk factors insurers assess. Compared to weatherboard or fibre cement homes, double brick properties often attract lower premiums because they're simply harder to damage.

Tiled Roof Terracotta or concrete tiles are considered a durable roofing option. While they can crack under extreme hail, they generally outperform metal or fibreglass in longevity and weather resistance, which insurers tend to reward.

Slab Foundation A concrete slab foundation is straightforward to assess and generally low-risk from an insurer's perspective. It avoids the subsidence and termite-access concerns associated with raised or timber-framed stumped foundations.

No Cyclone Risk Classification Despite being on the Gold Coast, this property does not fall within a designated cyclone risk area. This is a significant premium driver in Queensland — properties further north in cyclone zones can see their premiums skyrocket. Avoiding that classification keeps costs down considerably.

Swimming Pool and Solar Panels A pool adds some liability exposure and can slightly increase premiums, while solar panels represent an additional asset that may or may not be covered under a standard building policy (worth checking the PDS carefully). In this case, neither appears to have pushed the premium into higher territory — but it's always wise to confirm both are explicitly covered.

Construction Year: 1985 A home built in 1985 is mature but not ancient. Properties from this era were built under solid construction standards and, with proper maintenance, present manageable risk. Insurers may apply age-related loading for older homes, but a well-maintained double brick home typically avoids the worst of these adjustments.

---

Tips for Homeowners in Biggera Waters

1. Don't Accept Your Renewal Without Comparing The spread of premiums in Biggera Waters — from $4,045 to $8,728 at the 75th percentile — shows just how much prices vary. If you're currently paying above the suburb median of $5,287, it's very likely you can do better. Get a fresh quote at CoverClub to see where you stand.

2. Review Your Sum Insured Annually Building costs in Queensland have risen sharply in recent years. A sum insured of $844,000 for a 244 sqm home works out to roughly $3,459/sqm — a reasonable figure for current rebuild costs, but worth revisiting each year. Being underinsured at claim time can be a costly mistake.

3. Check What's Actually Covered Building-only cover protects the structure but not your contents. For a home with timber/laminate flooring, quality fittings, solar panels, and a pool, it's worth considering whether a combined building and contents policy makes more sense. Also confirm that your pool and solar system are explicitly listed as covered structures.

4. Maintain Your Property to Protect Your Premium Insurers can reduce or deny claims if damage is linked to poor maintenance. Keep your tiled roof in good repair, clear gutters regularly (especially ahead of storm season), and ensure your pool fencing meets Queensland's strict safety regulations. A well-maintained home is a lower-risk home — and that can translate to better premiums at renewal.

---

Ready to Compare?

Whether you're looking to benchmark your current policy or find a better deal, CoverClub makes it easy to compare home insurance quotes across Australia's leading insurers. With data drawn from thousands of real quotes, you'll always know where you stand. Start your free quote today at CoverClub — it only takes a few minutes.