If you own a free standing home in Bindoon, WA 6502, understanding what you should be paying for home and contents insurance is one of the smartest financial checks you can make. Nestled in the Toodyay Local Government Area about 80 kilometres north-east of Perth, Bindoon is a semi-rural community with a relaxed lifestyle — but that doesn't mean your insurance needs are any less important. This article breaks down a real quote for a five-bedroom, two-bathroom home in the area and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium in question comes in at $1,627 per year (or $159 per month) for combined home and contents cover, with a building sum insured of $769,000 and contents valued at $76,000. According to CoverClub's pricing data, this quote is rated CHEAP — meaning it sits below the average for comparable properties.

That's genuinely good news. A below-average premium on a policy covering nearly $850,000 worth of assets suggests the insurer has assessed the risk profile of this property favourably. Whether you're a long-time Bindoon resident or recently settled in the area, locking in a competitive rate like this — while ensuring the cover is adequate — is exactly what savvy homeowners should aim for.

That said, "cheap" doesn't always mean "best." It's worth periodically reviewing what's included in the policy, particularly around events like bushfire, storm damage, and accidental loss — all of which are relevant in regional WA.

---

How Bindoon Compares

Here's how this quote stacks up against the broader market:

| Benchmark | Premium |

|---|---|

| This Quote | $1,627/yr |

| LGA (Toodyay) Average | $2,178/yr |

| WA State Average | $2,144/yr |

| WA State Median | $1,944/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

The numbers tell a clear story. This quote is:

- $517 below the Toodyay LGA average (a saving of ~24%)

- $517 below the WA state average

- $317 below the WA state median

- A remarkable $1,338 below the national average — nearly half the price

It's worth noting that no suburb-level comparison data is currently available specifically for Bindoon 6502, but the LGA and state figures give a solid frame of reference. You can explore more detailed pricing trends on the Bindoon suburb stats page, the WA state insurance stats page, or compare against national home insurance averages.

The fact that this premium sits well below both the LGA and state averages — despite covering a large five-bedroom home — suggests a combination of favourable property characteristics and a competitive insurer assessment.

---

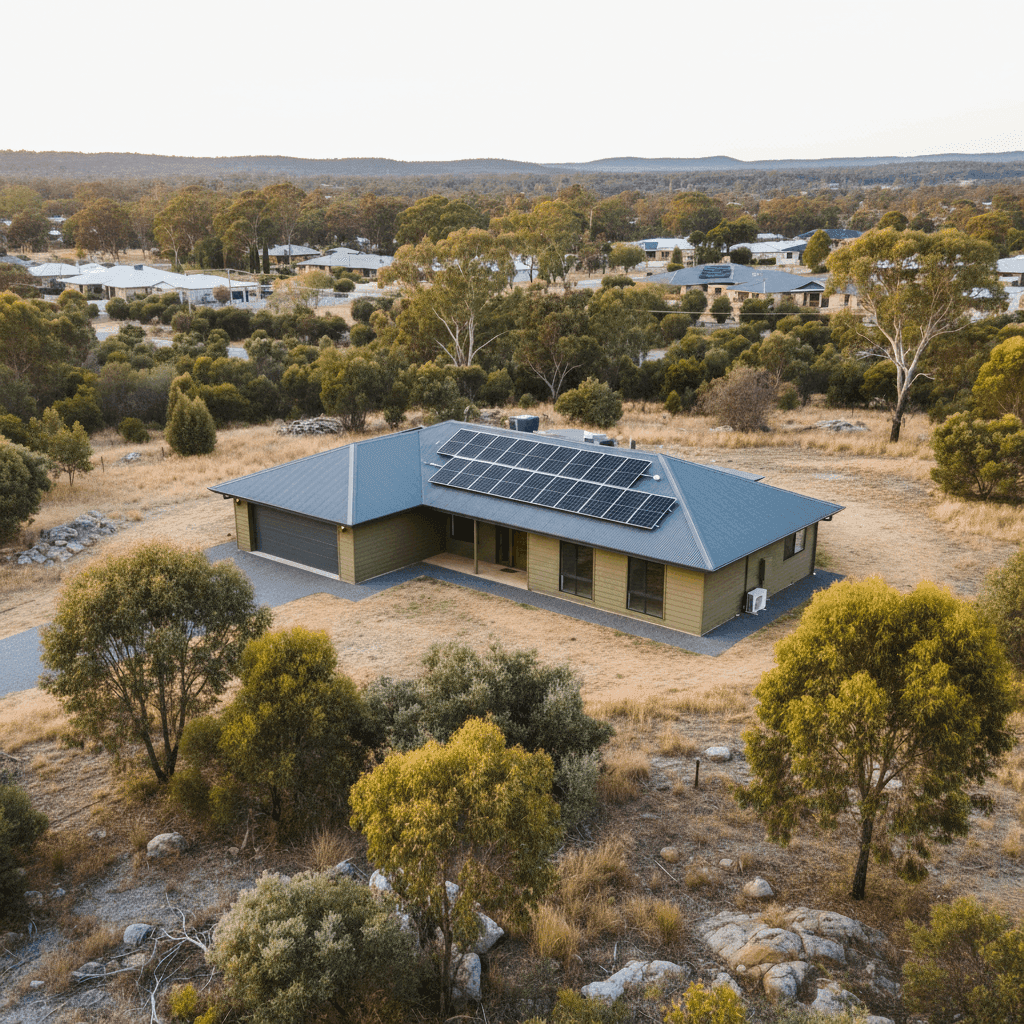

Property Features That Affect Your Premium

Several features of this particular property play a meaningful role in how insurers calculate risk and, ultimately, the premium charged.

Weatherboard Wood Exterior

Timber weatherboard is one of the more common wall materials in older Australian homes, and this property — built in 1989 — is no exception. Insurers can view timber cladding as a slightly elevated fire risk compared to brick veneer or double brick, particularly in bushfire-prone regions. However, the premium here suggests this risk has been priced reasonably.

Steel / Colorbond Roof

A Colorbond steel roof is generally viewed positively by insurers. It's durable, low-maintenance, and performs well in high-wind and storm conditions. Compared to older tile roofs, Colorbond tends to attract fewer claims for storm-related damage, which can contribute to a more competitive premium.

Slab Foundation

A concrete slab foundation is structurally sound and typically well-regarded by underwriters. It reduces the risk of subsidence-related claims and is standard for homes in WA's climate.

Solar Panels

The presence of solar panels adds value to the property but also introduces a specific consideration: are they covered under the building sum insured? Most policies include permanently fixed solar panels as part of the building, but it's worth confirming this with your insurer. Given the investment involved, you'll want to ensure your $769,000 building sum insured accounts for their replacement cost.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and typically forms part of the building sum insured. In WA's hot climate, this is an important inclusion — and one that can be expensive to replace if damaged by a power surge or storm event.

No Pool, Vinyl Flooring, Standard Fittings

The absence of a pool removes a common liability risk factor. Vinyl flooring and standard-grade fittings are straightforward for insurers to assess and replace, which keeps claims costs — and therefore premiums — more predictable.

---

Tips for Homeowners in Bindoon

1. Review Your Building Sum Insured Annually

With a building sum insured of $769,000, it's essential to ensure this figure keeps pace with rising construction costs. Building costs in regional WA have climbed significantly in recent years. An underinsured property can leave you seriously out of pocket after a major claim — even if your premium looks great on paper.

2. Check Your Bushfire Preparedness

Bindoon and the surrounding Toodyay LGA sit in an area with genuine bushfire exposure. Ensure your policy clearly covers bushfire damage, and consider whether your excess ($2,000 for building) is manageable in a worst-case scenario. Maintaining a defensible space around your home and following DFES guidelines can also reduce your risk profile over time.

3. Confirm Solar Panel Coverage

As mentioned above, clarify with your insurer exactly how your solar panels are covered — both for physical damage and for any liability associated with the system. Some policies may require a separate endorsement or have specific conditions around inverter damage.

4. Consider Your Contents Excess

The contents excess on this policy is $600 — relatively modest. However, it's worth reviewing whether your $76,000 contents valuation is accurate and up to date. A home contents calculator can help you avoid being underinsured on everything from furniture and electronics to clothing and appliances.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing your existing policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against real data from homeowners across WA and Australia. Get a home insurance quote today and find out if you're getting the deal you deserve.