If you own a free standing home in Black River, QLD 4818, you already know that insuring a property in North Queensland comes with its own set of challenges — and costs. This article breaks down a recent home and contents insurance quote for a three-bedroom weatherboard home in the suburb, puts the premium in context against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value on their cover.

---

Is This Quote Fair?

The quote in question comes in at $4,965 per year (or $487/month) for combined home and contents insurance, covering a building sum insured of $600,000 and contents valued at $89,000. The building excess is $2,000 and the contents excess is $600.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in perspective, the suburb average for Black River sits at $3,658/year, with a median of $3,621. That means this particular quote is running roughly $1,300 above the local average — a meaningful gap that warrants a closer look. Even at the 75th percentile for the suburb (i.e., among the more expensive quotes), the benchmark is $4,096/year, which is still nearly $870 less than this quote.

That said, several property-specific factors — which we'll explore below — help explain why this premium lands where it does.

---

How Black River Compares

Understanding your premium means looking beyond your own street. Here's how Black River stacks up at different geographic levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Black River (suburb) | $3,658/yr | $3,621/yr |

| Queensland (state) | $4,547/yr | $3,931/yr |

| Australia (national) | $2,965/yr | $2,716/yr |

| Townsville LGA | $7,258/yr | — |

A few things stand out here. First, Black River's suburb average of $3,658 is actually below the Queensland state average of $4,547 — suggesting that, within the broader North Queensland region, Black River is relatively more affordable than many surrounding areas. You can explore Queensland-wide insurance data to see how other postcodes in the state compare.

Second, both the suburb and state averages sit well above the national average of $2,965. This is consistent with the well-documented insurance affordability challenges across Queensland, particularly in cyclone-prone coastal and near-coastal regions. Nationally, the median premium is just $2,716 — less than half of what some Townsville LGA homeowners are paying. For a broader picture, the national home insurance statistics provide useful context.

Perhaps most striking is the Townsville LGA average of $7,258/year — nearly double the quote being analysed here. This suggests that while this quote is above average for Black River specifically, it is considerably more competitive when measured against the wider Townsville region.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium charged. Understanding these factors can help you make sense of your quote — and potentially identify areas to address.

Cyclone Risk Zone

This is the single biggest driver. Black River falls within a designated cyclone risk area, and insurers price this risk heavily. North Queensland is one of the most cyclone-exposed regions in Australia, and the cost of rebuilding after a major weather event is reflected in every premium in the area. This factor alone can add hundreds — or even thousands — of dollars to an annual premium compared with properties in southern states.

Weatherboard Timber Construction

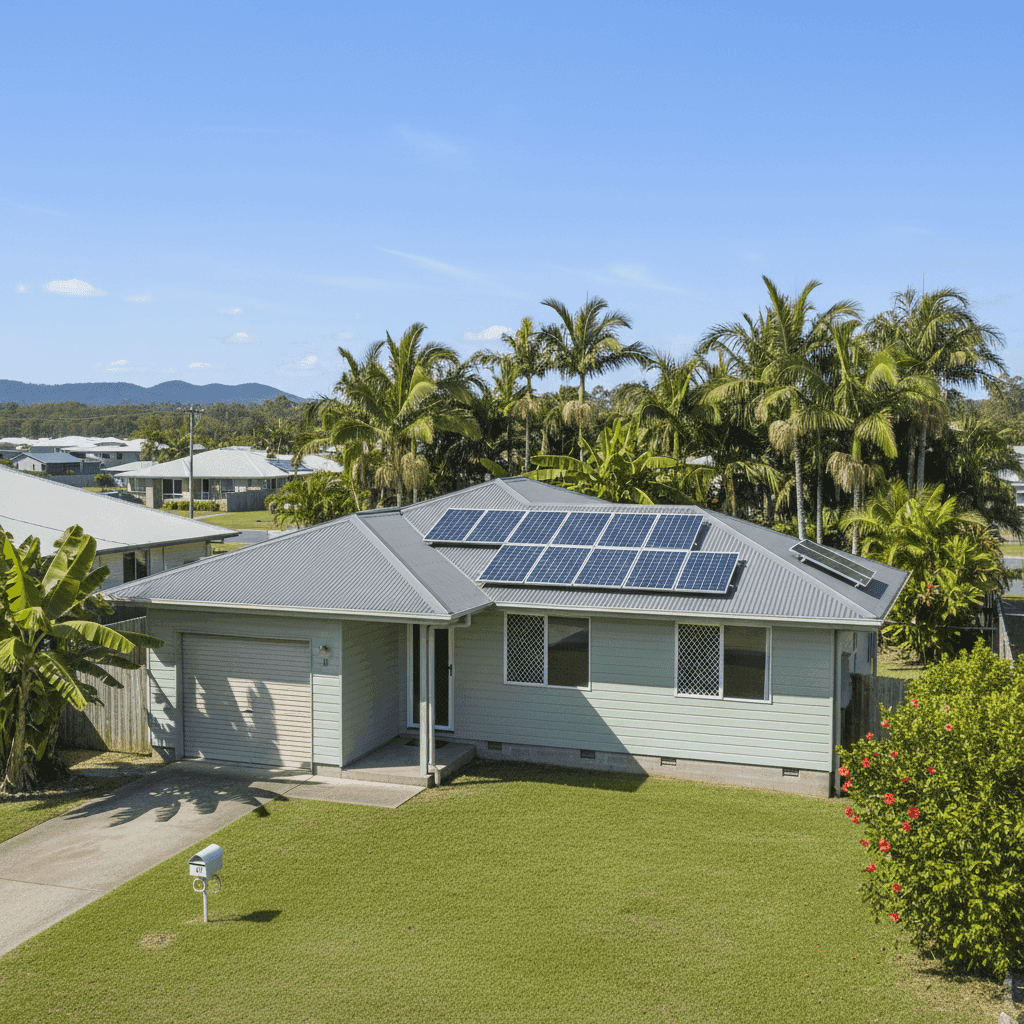

The external walls are weatherboard wood, which insurers generally consider higher risk than brick or rendered masonry. Timber-framed homes are more susceptible to fire, moisture damage, and wind-related structural damage — all of which are relevant concerns in a cyclone-prone region. This construction type typically attracts a loading on the base premium.

Roof Type: Steel/Colorbond

A Colorbond steel roof is actually viewed favourably by many insurers, particularly in cyclone zones, as it tends to perform better in high-wind events than tiled roofs. This may offer a modest offsetting benefit to the premium.

Age of Construction: 1980

At over 40 years old, this home pre-dates many modern building codes — including those introduced specifically to improve cyclone resilience. Older homes may require more extensive repairs or rebuilding to meet current standards, which can push up the sum insured and, in turn, the premium.

Solar Panels

The property has solar panels, which add to the overall replacement cost of the home. Insurers factor in the cost of reinstating solar systems when calculating building cover, so this will contribute modestly to the premium.

Building Size and Sum Insured

At 139 sqm with a building sum insured of $600,000, the per-square-metre replacement cost is approximately $4,317. In a cyclone-prone region with timber construction, this is not unreasonable — but it's worth periodically reviewing whether your sum insured accurately reflects current rebuild costs, neither over- nor under-insuring.

---

Tips for Homeowners in Black River

1. Compare Multiple Quotes — Every Year

Insurance premiums can vary significantly between providers for the same property. Even if you're happy with your current insurer, it pays to shop around at renewal time. Get a comparison quote through CoverClub to see what other providers are offering for your specific property.

2. Review Your Sum Insured Carefully

With construction costs having risen sharply in recent years, many homeowners are either over-insured (paying more than necessary) or under-insured (at risk of a shortfall after a claim). Use a building cost calculator or speak with a quantity surveyor to confirm your sum insured is accurate for a 1980-built weatherboard home in your area.

3. Consider a Higher Excess to Lower Your Premium

The building excess on this quote is $2,000. Opting for a higher voluntary excess — say, $2,500 or $3,000 — can reduce your annual premium, provided you're comfortable covering that amount out of pocket in the event of a claim. This strategy works best for homeowners with a solid emergency fund.

4. Ask About Cyclone Mitigation Discounts

Some insurers offer discounts for homes that have undergone cyclone-proofing upgrades, such as roof tie-down improvements, cyclone shutters, or compliance with newer wind-resistance standards. If you've made any improvements to the property since 1980, it's worth raising this with your insurer — it could result in meaningful savings.

---

Ready to See What You Could Be Paying?

Whether you think your current premium is too high or you simply want peace of mind that you're getting fair value, comparing quotes is the smartest first step. CoverClub makes it easy to benchmark your home insurance against real data from properties like yours across Black River and Queensland. Start your free comparison at CoverClub and find out what a competitive quote looks like for your home.