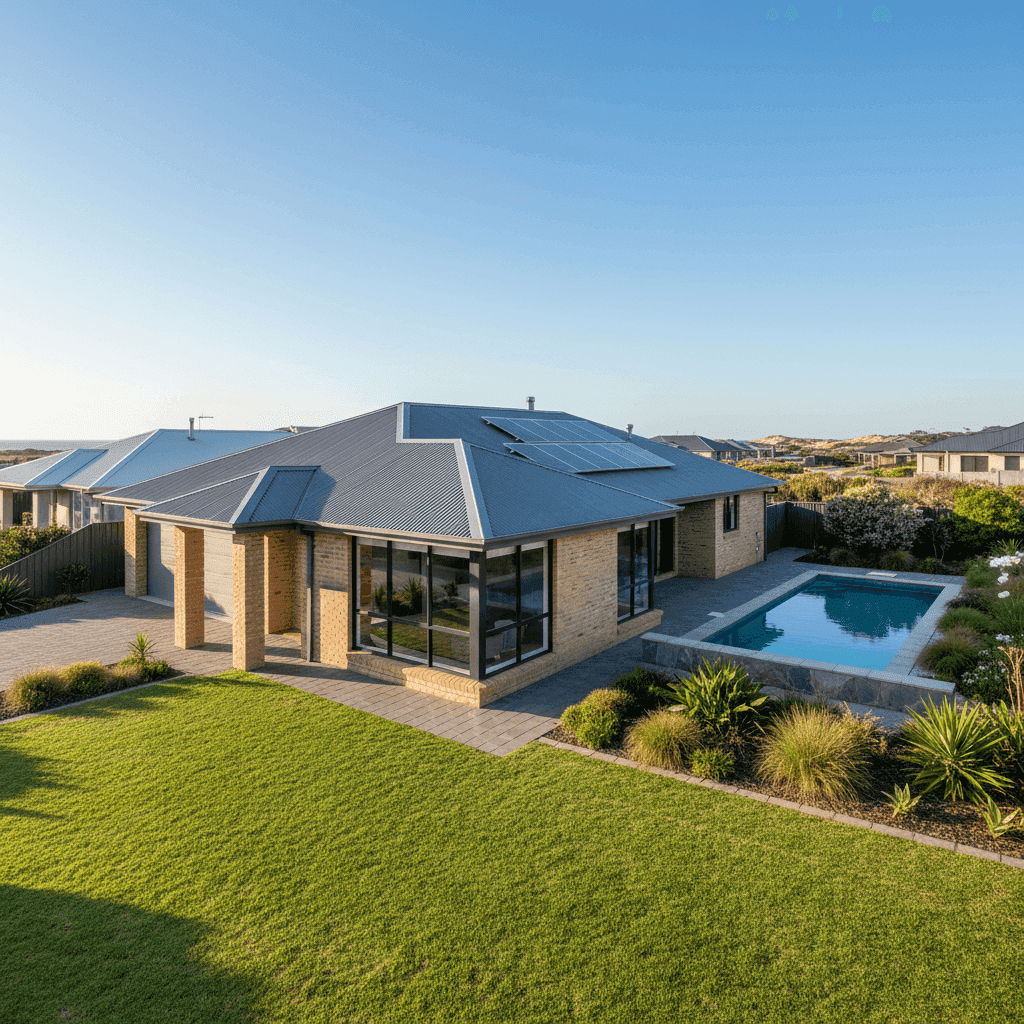

Blairgowrie is one of the Mornington Peninsula's most sought-after coastal communities — a place where relaxed beach living meets genuine property value. For owners of a free-standing home in this postcode, understanding what you should be paying for home and contents insurance is just as important as getting the right cover. This article breaks down a real quote for a 4-bedroom, 2-bathroom brick veneer home in Blairgowrie (VIC 3942), and puts the numbers in context so you can make a confident, informed decision.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote came in at $1,937 per year (or $186/month), covering $940,000 in building sum insured and $184,000 in contents — with a $2,000 excess on both building and contents claims.

Our price rating for this quote is FAIR (Around Average), and the data backs that up. The suburb average premium for Blairgowrie sits at $1,961/year, meaning this quote lands almost exactly on the local benchmark — just $24 below the average. It also falls comfortably within the middle of the market, sitting between the 25th percentile ($1,556/yr) and the 75th percentile ($2,351/yr) for this suburb.

In other words, you're not getting a bargain, but you're not being overcharged either. If you've received a similar quote, it's reasonable — though there's still room to explore whether a competing insurer might offer better value for the same level of cover.

---

How Blairgowrie Compares

To truly appreciate what this quote means, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This Quote | $1,937/yr |

| Blairgowrie Suburb Average | $1,961/yr |

| Blairgowrie Suburb Median | $1,774/yr |

| Mornington Peninsula LGA Average | $2,652/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, Blairgowrie premiums are significantly lower than the Victorian state average — this quote is roughly 35% cheaper than what the typical Victorian homeowner pays. That's a meaningful difference, and it reflects the relatively lower risk profile of the Mornington Peninsula compared to, say, flood-prone or bushfire-exposed parts of regional Victoria.

Second, the national average of $5,347/year might raise eyebrows — but it's heavily influenced by high-risk regions in Queensland, Western Australia, and the Northern Territory, where cyclone, flood, and storm exposure drives premiums sky-high. Blairgowrie is not a cyclone risk area, which is one reason local premiums remain comparatively modest.

Interestingly, this quote also comes in well below the Mornington Peninsula LGA average of $2,652/year, suggesting that Blairgowrie specifically may benefit from more favourable risk characteristics within the broader peninsula region.

You can explore more localised data on the Blairgowrie suburb stats page, compare it against all of Victoria, or see how it stacks up nationally.

> Note: The suburb sample size for this analysis is 14 quotes, so while the data is directionally useful, a larger sample would provide even greater confidence in the benchmarks.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a combination of structural, locational, and lifestyle factors. Here's how the specific features of this property likely influence the premium:

Brick Veneer Walls & Colorbond Roof

Brick veneer is one of the most common and well-regarded construction types in Australian suburbia. It offers solid fire resistance and durability, which insurers generally view favourably. Paired with a steel Colorbond roof — known for its longevity, wind resistance, and low maintenance — this home presents a relatively low structural risk profile. These are positive factors that help keep premiums in check.

Slab Foundation

A concrete slab foundation is standard for homes of this era and is generally considered stable and low-risk. It eliminates the underfloor moisture and pest concerns sometimes associated with older raised foundations, which can be a minor positive in the eyes of underwriters.

Timber & Laminate Flooring

Timber and laminate flooring can be more expensive to replace than carpet, which may contribute slightly to the overall contents or building valuation. It's worth ensuring your sum insured accurately reflects the cost of reinstating these finishes.

Swimming Pool

A pool adds value to the property but also introduces additional liability considerations. Most insurers factor pool ownership into their risk assessment, particularly around public liability cover. Ensure your policy includes adequate liability protection — this is especially relevant if the property is used as a holiday rental, which is common in Blairgowrie.

Solar Panels

Solar panels are increasingly common across Victoria, and most home insurance policies cover them as a fixed fixture of the building. However, it's worth confirming with your insurer that your panels are explicitly included under the building sum insured and that the $940,000 figure accounts for their replacement cost.

Ducted Climate Control

Ducted heating and cooling systems are a meaningful fixed asset. Like solar panels, they should be captured within your building sum insured. Given the coastal climate of the Mornington Peninsula — warm summers and cool winters — this system adds real value and replacement cost to the property.

Construction Year: 1989

At around 35 years old, this home is well past its initial build phase but not yet at the age where significant structural concerns typically arise. Insurers may note the age when assessing risk for things like plumbing and electrical systems, so keeping maintenance records up to date is a sensible precaution.

---

Tips for Homeowners in Blairgowrie

Whether you're a permanent resident or use your Mornington Peninsula home as a holiday escape, here are four practical ways to get the most out of your home insurance:

- Review your sum insured annually. Building costs have risen sharply in recent years. A home insured at $940,000 today may cost significantly more to rebuild in two or three years' time. Use a building cost calculator or speak with a local builder to ensure you're not underinsured — this is one of the most common and costly mistakes homeowners make.

- Clarify your holiday rental status. Blairgowrie is a popular short-stay destination, and many homeowners list their property on platforms like Airbnb or Stayz. Standard home insurance policies often exclude or limit cover when a property is rented to paying guests. If you rent your home out — even occasionally — speak to your insurer about landlord or short-stay endorsements.

- Check your pool and liability cover. With a swimming pool on the property, public liability cover is particularly important. Confirm the liability limit on your policy (typically $10–$20 million) and ensure it covers incidents involving guests or visitors around the pool area.

- Compare quotes before your renewal date. This quote is rated as fair, but "fair" doesn't mean you can't do better. The insurance market is competitive, and premiums can vary significantly between providers for identical cover. Set a reminder to compare quotes at least 30 days before your renewal — it takes minutes and could save you hundreds.

---

Compare Home Insurance Quotes in Blairgowrie

Whether you're reviewing an existing policy or shopping for cover on a new purchase, CoverClub makes it easy to see what multiple insurers would charge for your specific property. Our tools are built for Australian homeowners, with suburb-level data and transparent comparisons.