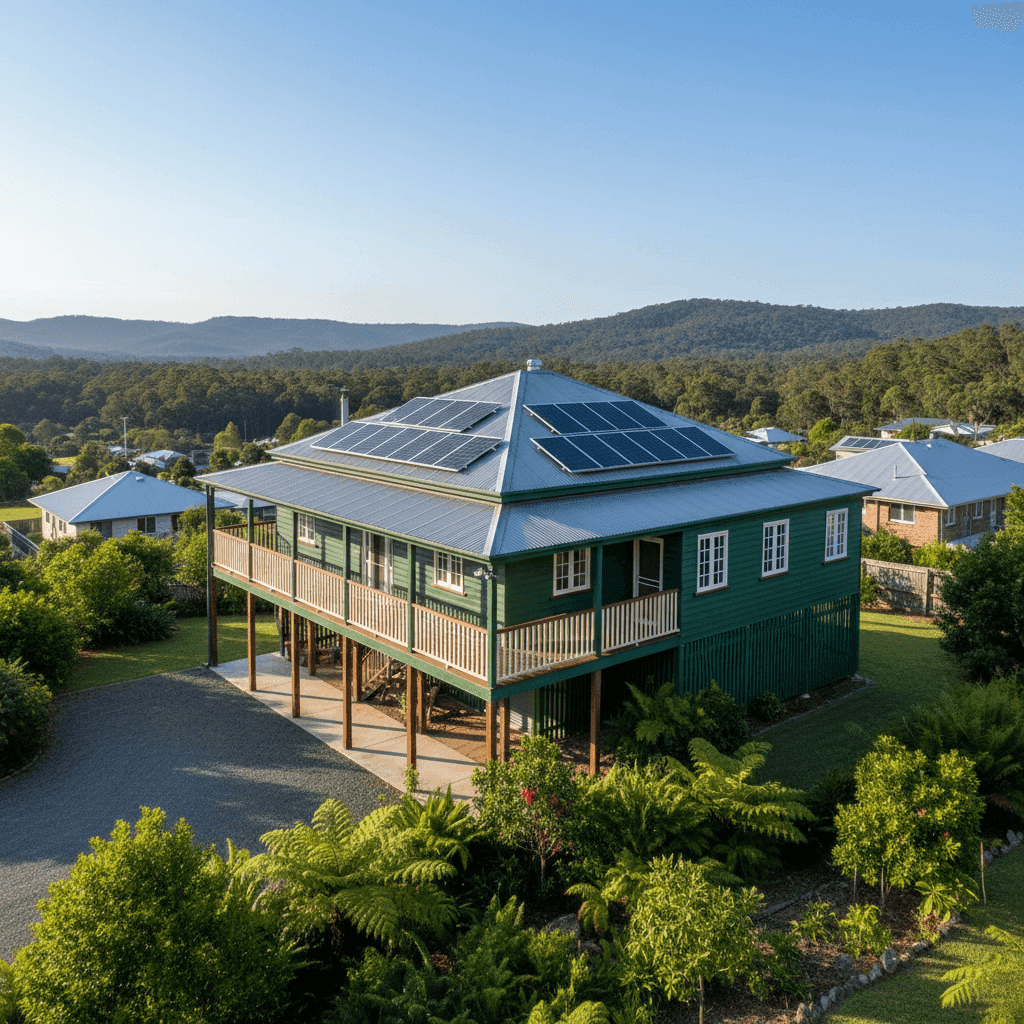

Tucked away in the hinterland behind Lismore, Blakebrook is a quiet semi-rural locality in the Northern Rivers region of New South Wales. It's the kind of place where character homes on generous blocks are the norm — and the 3-bedroom, free-standing weatherboard home we're analysing here fits that description perfectly. Built in 1945, elevated on stumps, and clad in classic weatherboard timber, this property carries a lot of charm — and, as we'll explore, some unique insurance considerations.

This article breaks down a real home and contents insurance quote for a property in Blakebrook (NSW 2480), compares it against state and national benchmarks, and offers practical tips for homeowners in the area.

---

Is This Quote Fair?

The annual premium for this property came in at $3,105 per year (or $291/month), covering a building sum insured of $550,000 and contents valued at $20,000, with a $2,000 excess on both building and contents.

Our pricing engine has rated this quote as CHEAP — below average for this type of property. That's genuinely good news for the homeowner.

To put it in context:

- The NSW state average premium is $9,528/yr — this quote is 69% cheaper

- The NSW state median is $3,770/yr — this quote sits $665 below the median

- The national average is $5,347/yr — again, this quote comes in well under

- The national median is $2,764/yr — this quote is slightly above the national median, which is expected given the older construction and elevated build style

So while the quote isn't the absolute cheapest on the market, it represents solid value — particularly for a pre-war weatherboard home in a regional NSW location. Homeowners in this area should feel reasonably confident they're not being overcharged.

---

How Blakebrook Compares

One of the most striking data points here is the Ballina LGA average premium of $23,241/yr. Blakebrook falls within the Ballina LGA, and that figure reflects just how heavily flood and weather risk weighs on insurance pricing across the broader region — particularly following the devastating 2022 Northern Rivers flood events.

The fact that this particular quote lands at $3,105 — less than 14% of the LGA average — is remarkable. It likely reflects a combination of the property's specific elevation (more on that below), its distance from major waterways, and the insurer's individual risk assessment.

For broader context, you can explore Blakebrook's suburb-level insurance stats, compare against NSW state averages, or view national home insurance benchmarks to see how your own situation stacks up.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on how insurers calculate risk and, ultimately, what you pay.

Elevated on Stumps

This is arguably the single most important factor keeping this premium competitive. The home is elevated by at least one metre on stumps, which significantly reduces flood inundation risk. In a region like the Northern Rivers — which has experienced catastrophic flooding — elevation can be the difference between a manageable premium and an eye-watering one. Insurers reward this feature, and rightly so.

Weatherboard Timber Construction

Weatherboard homes are beloved for their character but can attract higher premiums due to their susceptibility to fire, rot, and general wear. Timber-framed, timber-clad homes are typically more expensive to repair or rebuild than brick veneer or double-brick equivalents. The $550,000 building sum insured reflects the cost of rebuilding a quality older home — not just its market value.

Age of Construction (1945)

An 80-year-old home brings charm and craftsmanship, but also ageing plumbing, wiring, and structural elements that insurers factor into their risk models. Older homes can be more costly to repair due to non-standard materials and construction methods.

Timber/Laminate Flooring

Timber flooring is a valued feature but can be expensive to replace, particularly in an older home where original boards may be difficult to source or match.

Solar Panels

The property has solar panels installed, which adds modest replacement value to the building sum insured. It's worth confirming with your insurer that solar panels are explicitly covered under your policy — not all standard policies include them automatically.

Ducted Climate Control

A ducted climate control system is another fixed asset that should be covered under the building policy. Again, verify this is captured in your sum insured and not excluded.

No Pool, No Cyclone Risk Zone

The absence of a pool removes a common source of liability and maintenance claims. And while the Northern Rivers region can experience severe storms, Blakebrook is not classified as a cyclone risk area, which keeps premiums lower than coastal Queensland equivalents.

---

Tips for Homeowners in Blakebrook

1. Don't Underinsure Your Weatherboard Home

Rebuilding costs for older timber homes consistently exceed expectations. Materials, trades, and demolition costs have all risen sharply in recent years. Review your $550,000 sum insured annually and use a building cost calculator to ensure it reflects current rebuild costs — not the price you paid for the property.

2. Document Your Elevation

If your home is elevated on stumps, make sure your insurer has this on record. Some insurers offer explicit discounts for elevated properties in flood-prone regions. If you're not sure whether your elevation has been factored in, ask directly — it could save you hundreds of dollars a year.

3. Confirm Solar and Climate Control Coverage

Solar panels and ducted systems are significant assets. Check your Product Disclosure Statement (PDS) to confirm they're covered under your building policy, and that their replacement value is included in your sum insured. If they're not, request an endorsement or consider a policy that explicitly covers them.

4. Compare Quotes at Renewal

Given the wide spread of premiums across the Ballina LGA — from under $3,200 to well over $23,000 — it's clear that insurers price this area very differently. What seems like a fair premium today may not be competitive next year. Set a reminder to compare quotes at CoverClub before your renewal date each year.

---

Ready to Compare Your Own Quote?

Whether you're a Blakebrook local or anywhere else in Australia, CoverClub makes it easy to see how your home insurance premium stacks up. Enter your address, get an indicative quote, and instantly compare it against suburb, state, and national averages — so you always know if you're getting a fair deal.