If you own a free standing home in Boambee, NSW 2450, you're probably wondering whether your home insurance premium is competitive — or whether you're quietly paying too much. This article breaks down a real home and contents insurance quote for a four-bedroom, brick veneer property in Boambee, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value from your cover.

---

Is This Quote Fair?

The quote in question comes to $5,125 per year (or around $491 per month) for a combined home and contents policy. It covers a building sum insured of $1,019,000 and contents valued at $245,000, with a $1,000 excess applying to both building and contents claims.

Our independent price rating for this quote is FAIR — Around Average.

That assessment holds up well when you put it in context. The suburb average for home insurance in Boambee sits at $6,296 per year, meaning this quote comes in roughly $1,171 below the local average — a meaningful saving. Against the suburb median of $5,863, the quote is also favourably positioned, sitting comfortably below the midpoint of what other Boambee homeowners are paying.

In short, this isn't a bargain-basement price, but it's a solid result — particularly given the property's above-average fittings, pool, solar panels, and ducted climate control, all of which can push premiums upward.

---

How Boambee Compares

Understanding where Boambee sits in the broader insurance landscape is useful context for any homeowner in the area. Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,125 |

| Boambee Suburb Average | $6,296 |

| Boambee Suburb Median | $5,863 |

| Boambee 25th Percentile | $4,683 |

| Boambee 75th Percentile | $7,438 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

| Clarence Valley LGA Average | $31,244 |

A few things stand out here. First, the NSW state average of $9,528 is dramatically higher than this quote — though that figure is heavily skewed by high-risk and high-value properties across the state. The NSW median of $3,770 tells a more grounded story, reflecting that many NSW homeowners pay considerably less for more modest properties or lower cover levels.

The Clarence Valley LGA average of $31,244 is striking, and worth flagging. This figure is likely influenced by properties in flood-prone or high-risk zones within the broader LGA, which can attract significantly elevated premiums. Boambee itself, as a suburb of Coffs Harbour, tends to have a more moderate risk profile than some of its LGA neighbours, which helps explain why this quote lands well below that LGA average.

At the national level, the average premium of $5,347 is very close to this quote, while the national median of $2,764 reflects the large number of lower-value or less comprehensively insured properties across the country.

You can explore more local data on the Boambee suburb stats page, compare against NSW state-wide figures, or browse national home insurance benchmarks.

---

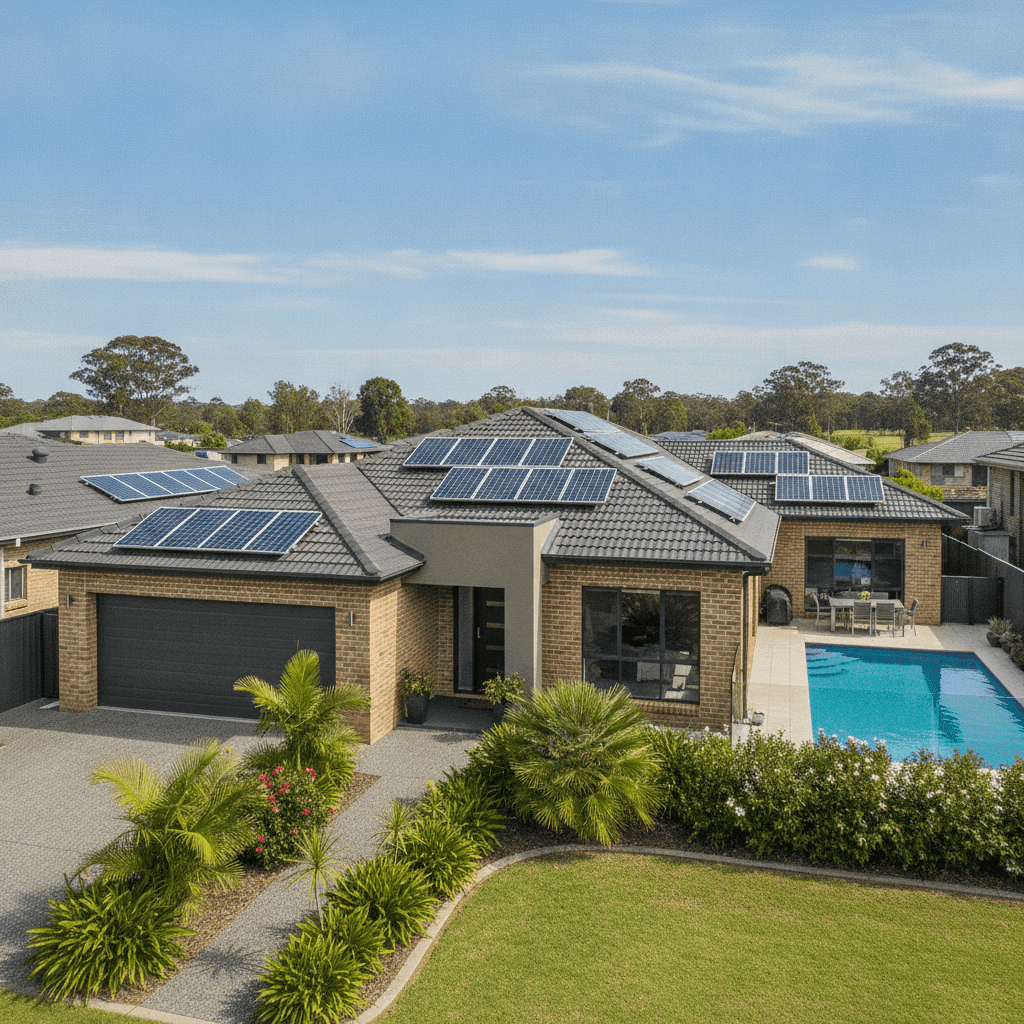

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding these factors can help you make sense of your premium — and potentially negotiate a better rate.

Brick Veneer Construction & Tiled Roof Brick veneer walls and a tiled roof are generally viewed favourably by insurers. Both materials offer solid fire resistance and durability, which can translate to lower premiums compared to properties with timber cladding or metal roofing. The slab foundation also adds structural stability, reducing the risk of subsidence-related claims.

Above-Average Fittings Quality The property's above-average fittings — think quality kitchen appliances, premium fixtures, and higher-end finishes — increase the cost to rebuild or repair, which is reflected in the $1,019,000 building sum insured. Insurers price accordingly, so it's important that your sum insured genuinely reflects replacement costs rather than market value.

Swimming Pool A pool adds liability exposure and increases the complexity of a rebuild, both of which contribute to a higher premium. Pools can also be a source of claims in storm or hail events, particularly in coastal NSW.

Solar Panels Solar panels are increasingly common on Australian rooftops, but they do add to the replacement cost of a property and can be damaged in storms or hail. Ensuring your policy explicitly covers solar panels — and that your sum insured accounts for their value — is essential.

Ducted Climate Control Ducted air conditioning systems are expensive to replace and can be affected by storm damage, power surges, or mechanical failure. Their inclusion in the building sum insured is appropriate and contributes to the overall premium.

No Cyclone Risk Boambee falls outside designated cyclone risk zones, which is a meaningful premium advantage. Properties in northern Queensland or parts of WA can pay significantly more due to cyclone loading. This property avoids that surcharge entirely.

---

Tips for Homeowners in Boambee

1. Review Your Sum Insured Annually Construction costs in NSW have risen sharply in recent years. A sum insured that was accurate in 2022 may now underinsure your home. Use a building replacement cost calculator or ask your insurer to reassess — being underinsured at claim time can be a costly mistake.

2. Check That Solar Panels and the Pool Are Explicitly Covered Not all standard home insurance policies automatically cover solar panel systems or pool equipment to their full value. Read your Product Disclosure Statement carefully and confirm that these features are included and adequately valued in your policy.

3. Compare Quotes Before Renewal Our data shows a wide spread of premiums in Boambee — from around $4,683 at the 25th percentile to $7,438 at the 75th. That's a gap of nearly $2,800 per year for comparable properties. Shopping around at renewal time is one of the simplest ways to avoid drifting into the upper end of that range.

4. Consider Your Excess Level A $1,000 excess is fairly standard, but increasing your excess can meaningfully reduce your annual premium. If you have the financial buffer to cover a higher out-of-pocket amount in the event of a claim, raising your excess to $2,000 or more could trim your premium without significantly changing your risk exposure.

---

Compare Home Insurance Quotes in Boambee

Whether you're reviewing an existing policy or shopping for cover on a new property, it pays to see what the market is offering. At CoverClub, you can compare home and contents insurance quotes tailored to your property in Boambee and across Australia. Get a quote today and see how your premium stacks up.