If you own a free standing home in Bombo, NSW 2533, you're likely no stranger to the charm of the South Coast — and the insurance market that comes with it. Situated in the Kiama local government area, Bombo sits just north of Kiama township along one of New South Wales' most scenic coastlines. That coastal position, combined with the age and style of many local homes, can have a meaningful impact on what you pay for building insurance. This article breaks down a real building-only insurance quote for a four-bedroom, three-bathroom free standing home in Bombo, and puts it in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,192 per year (or $215/month) for building-only cover on a home insured for $500,000, with a $5,000 building excess. Our price rating for this quote is CHEAP — below average — and the data backs that up convincingly.

The suburb average premium for Bombo sits at $4,448/year, meaning this quote is roughly 51% below what other homeowners in the same postcode are typically paying. Even compared to the suburb's 25th percentile (the cheapest quarter of quotes) at $3,554/year, this quote still comes in well under the mark.

It's worth noting that the suburb sample size is relatively small at six quotes, so the local averages should be interpreted with some caution — a few high-value or high-risk properties can skew the figures. That said, the gap between this quote and every local benchmark is substantial enough to be meaningful.

For homeowners wondering whether they're getting a fair deal, this quote represents genuinely strong value. Whether you're renewing or shopping around for the first time, it's a useful benchmark to keep in mind.

---

How Bombo Compares

Understanding where Bombo sits relative to broader markets helps put any individual quote into perspective. Here's how the numbers stack up:

| Benchmark | Premium |

|---|---|

| This Quote | $2,192/yr |

| Bombo Suburb Average | $4,448/yr |

| Bombo Suburb Median | $3,904/yr |

| Kiama LGA Average | $3,332/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/year is notably high — driven in large part by extreme weather-affected regions in northern and western NSW that push the mean upward significantly. The state median of $3,770/year is a more representative figure for typical NSW homeowners, and this quote still beats it comfortably.

At the national level, the average premium of $5,347/year reflects the wide diversity of risk profiles across Australia — from cyclone-prone Far North Queensland to bushfire-affected inland regions. The national median of $2,764/year is the closest benchmark to this quote, suggesting the property sits in a relatively favourable risk tier nationally.

The Bombo suburb stats show a median of $3,904/year, nearly double this quote — a strong indicator that this particular policy is priced very competitively for the area.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess its risk profile and price a policy accordingly.

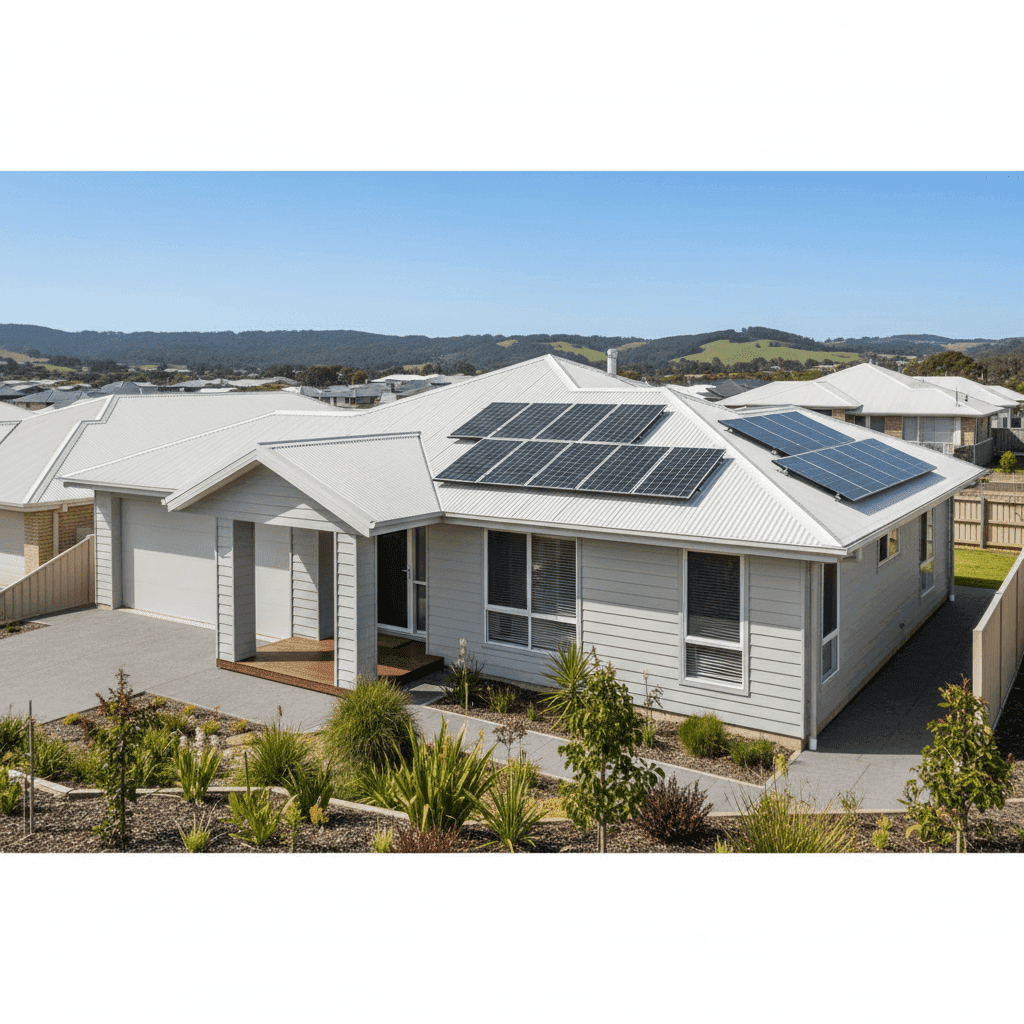

Hardiplank/Hardiflex Cladding The external walls are clad in Hardiplank Hardiflex, a fibre cement product that is widely used across Australia. Insurers generally view fibre cement cladding favourably — it's non-combustible, durable, and resistant to rot and pests. This can work in the homeowner's favour compared to properties with timber weatherboard exteriors.

Steel/Colorbond Roof A Colorbond steel roof is another positive risk signal. It's fire-resistant, long-lasting, and holds up well in coastal conditions where salt air can accelerate corrosion in lesser materials. Insurers typically price Colorbond roofs more competitively than older tile or fibro roofing.

Slab Foundation A concrete slab foundation is considered low-risk by most insurers. It's structurally stable and not susceptible to the subsidence or pest issues that can affect older suspended timber floors.

Construction Year: 1985 At roughly 40 years old, the property is well past its new-build phase but not so old as to trigger significant concerns about outdated wiring, plumbing, or structural integrity — provided it has been reasonably maintained. Homes from this era built on slab with fibre cement cladding tend to age well.

Solar Panels The presence of solar panels adds some complexity to a building insurance policy. Panels are typically covered as part of the building sum insured, but it's worth confirming with your insurer that the panels and inverter are explicitly included in your cover. Some policies treat them as a separate item.

Ducted Climate Control Ducted air conditioning systems are a fixed building feature and should be captured within the building sum insured. Given the replacement cost of a full ducted system can run into the tens of thousands, homeowners should ensure their $500,000 sum insured adequately accounts for this.

No Pool, No Cyclone Risk Zone The absence of a pool removes a common liability and maintenance concern that can elevate premiums. Bombo is also not classified as a cyclone risk area, which keeps wind-event loadings lower than properties in northern Australia.

---

Tips for Homeowners in Bombo

1. Review your sum insured regularly Construction costs have risen sharply in recent years. A $500,000 sum insured on a 214 sqm home in regional NSW is worth stress-testing against current rebuild cost estimates. Underinsurance is one of the most common — and costly — mistakes homeowners make. Consider using a building cost calculator or speaking with a quantity surveyor.

2. Confirm solar panels are covered If your policy doesn't explicitly list solar panels as a covered item, ask your insurer to clarify. Some policies include them automatically; others require an endorsement. Given the value of a typical solar system, it's a gap worth closing.

3. Shop around at renewal The fact that this quote is well below the suburb average suggests that pricing varies significantly between insurers for homes in this area. Loyalty doesn't always pay — comparing quotes at renewal can surface meaningfully better deals. Get a quote at CoverClub to see how your current premium stacks up.

4. Understand your excess This policy carries a $5,000 building excess, which is on the higher end. A higher excess typically reduces your annual premium, but it means you'll need to fund the first $5,000 of any claim yourself. Make sure this aligns with your financial comfort level — if you'd struggle to cover that out of pocket, it may be worth exploring policies with a lower excess, even if the annual premium is slightly higher.

---

Compare Your Home Insurance Today

Whether you're a long-time Bombo local or new to the South Coast, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare building and contents insurance quotes from multiple insurers in one place — so you can see at a glance whether you're getting a competitive rate. Start your comparison at CoverClub and find out what your home should really cost to insure.