Bongaree is a laid-back coastal suburb sitting on Bribie Island in South East Queensland — and like much of the region, home insurance here can be anything but straightforward. This article takes a close look at a real home and contents insurance quote for a two-bedroom, two-bathroom free standing home in Bongaree (postcode 4507), breaking down what the numbers mean and how they stack up against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $4,195 per year (or $411 per month), covering a building sum insured of $400,000 and contents valued at $20,000. The building excess is $2,000 and the contents excess is $1,000.

Our pricing engine rates this quote as Fair — Around Average, and the data backs that up. At $4,195, this premium sits comfortably between the suburb's 25th percentile ($3,489/yr) and the 75th percentile ($12,137/yr), placing it in the middle of the pack for Bongaree. It's notably below the suburb average of $7,453 and the suburb median of $7,503 — which is a meaningful saving.

That said, "fair" doesn't necessarily mean "the best available." It means the quote is in a reasonable range given the property's characteristics and location. There may still be room to do better with the right insurer.

---

How Bongaree Compares

To put this quote in context, here's how Bongaree premiums compare across different geographic levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bongaree (4507) | $7,453/yr | $7,503/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out immediately. Bongaree's average premium is more than double the national average — a stark reminder that location plays an enormous role in insurance pricing. Even compared to the broader Queensland average of $4,547, Bongaree sits significantly higher.

The Sunshine Coast LGA average of $7,249 per year also reflects the elevated risk profile of coastal properties in this region. Proximity to the water, the nature of Bribie Island's geography, and the general exposure of coastal Queensland all contribute to higher base premiums across the board.

At $4,195, this particular quote is actually well below both the suburb average and the LGA average, which suggests the property's specific features are working in the owner's favour. You can explore the full breakdown of Bongaree insurance statistics, compare against Queensland-wide data, or see how the region tracks against national benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some favourably, others less so.

✅ Factors Working in Your Favour

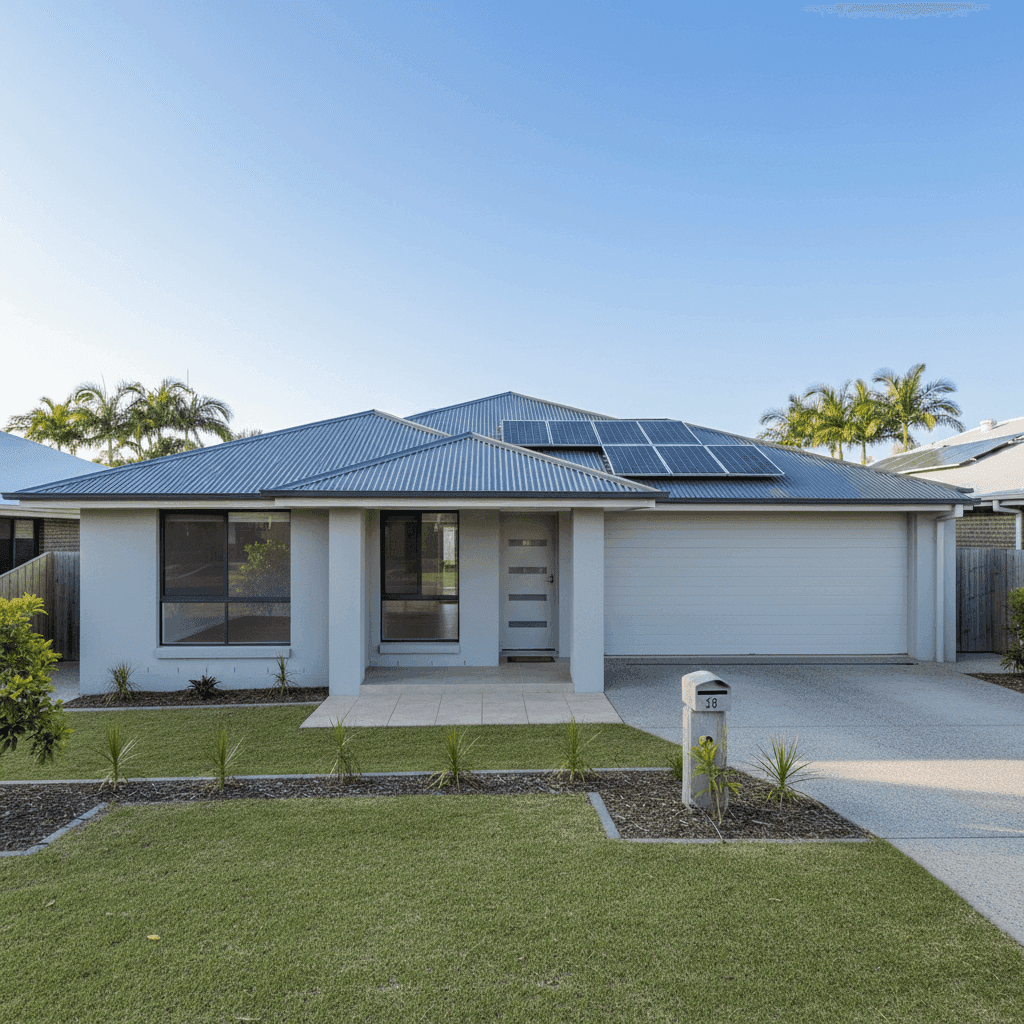

Modern construction (2022): A home built in 2022 benefits from current building codes, which are significantly more stringent than those of earlier decades. Newer builds tend to be more structurally sound, better insulated, and constructed with materials that meet modern safety standards — all of which insurers view positively.

Hebel external walls: Autoclaved aerated concrete (AAC) panels like Hebel are lightweight, fire-resistant, and durable. Compared to older brick veneer or weatherboard construction, Hebel is generally well-regarded by insurers for its resilience.

Steel/Colorbond roof: Colorbond roofing is a popular choice in Queensland for good reason — it's lightweight, resistant to corrosion, and performs well in high-wind conditions. Insurers tend to price this roof type favourably compared to terracotta or concrete tiles.

Slab foundation: A concrete slab is a stable and low-maintenance foundation type that carries minimal risk of subsidence or pest intrusion compared to raised timber stumps.

No pool: Pools add liability exposure and maintenance complexity. Not having one keeps the risk profile simpler.

Tiles flooring: Tiles are durable, water-resistant, and straightforward to replace — a practical choice in a coastal Queensland climate.

⚠️ Factors That May Increase Costs

Coastal location on Bribie Island: Despite not being in a designated cyclone risk zone, Bongaree's island location means exposure to coastal weather events, storm surge risk, and salt air — all of which can influence premiums.

Solar panels: While solar panels are a great sustainability investment, they do add to the replacement cost of the roof and introduce some additional risk (electrical systems, panel damage). This can nudge premiums slightly upward.

Building sum insured of $400,000: For a 105 sqm home, this is a reasonable sum insured, but it's worth periodically reviewing whether this figure accurately reflects current rebuild costs, which have risen sharply in recent years.

---

Tips for Homeowners in Bongaree

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps to make sure you're getting the right cover at the right price.

1. Don't anchor to the suburb average — shop around. With a suburb average of $7,453, it's easy to assume $4,195 is a great deal and stop there. But premiums vary significantly between insurers for the same property. Getting multiple quotes through a platform like CoverClub takes minutes and can reveal meaningful differences.

2. Review your building sum insured annually. Construction costs in Queensland have risen considerably since 2022. Even for a relatively new home, it's worth reassessing whether your $400,000 sum insured still covers a full rebuild — including demolition, debris removal, and professional fees. Underinsurance is one of the most common and costly mistakes homeowners make.

3. Consider your excess settings carefully. A $2,000 building excess is on the higher end. While a higher excess reduces your annual premium, it also means a larger out-of-pocket cost when you do need to claim. Make sure the trade-off makes sense for your financial situation.

4. Maintain your solar panels and roof. Insurers expect homes to be well-maintained. Keeping your Colorbond roof and solar panel system in good condition — including regular inspections and prompt repair of any damage — not only protects your home but helps ensure claims aren't disputed on maintenance grounds.

---

Compare Your Options with CoverClub

Whether this quote is your first or your fifth, it pays to compare. CoverClub makes it easy to see how your premium stacks up and find competitive home and contents insurance tailored to your property. Get a quote today and see what's available for your Bongaree home — you might be surprised by what's out there.