Bongaree is a relaxed coastal suburb sitting on Bribie Island in South East Queensland — a popular spot for families and retirees drawn to its waterfront lifestyle and relatively affordable property prices. But how much should you expect to pay for home and contents insurance on a free standing home here? This article breaks down a real quote for a three-bedroom, two-bathroom brick veneer home in Bongaree (postcode 4507), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,524 per year (or roughly $247 per month) for combined home and contents cover, with a building sum insured of $395,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a meaningful finding, because Bongaree is not typically known for bargain insurance premiums. Sitting in coastal Queensland, properties in this postcode are exposed to a range of weather-related risks that insurers price carefully. To land a quote well below the suburb average is a genuinely positive outcome for this homeowner.

To put it plainly: if you're paying around $2,524 for home and contents cover on a property like this in Bongaree, you're doing better than most of your neighbours.

---

How Bongaree Compares

The numbers tell a striking story when you line this quote up against the available benchmarks.

| Benchmark | Premium |

|---|---|

| This quote | $2,524/yr |

| Suburb 25th percentile | $3,489/yr |

| Bongaree suburb average | $7,453/yr |

| Bongaree suburb median | $7,503/yr |

| LGA (Sunshine Coast) average | $7,249/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

A few things stand out immediately. The suburb average of $7,453 per year is nearly three times the cost of this quote — a remarkable gap. Even the cheapest quarter of quotes in Bongaree (the 25th percentile) sits at $3,489, which is still $965 more expensive than this result. The wide spread between the 25th percentile ($3,489) and the 75th percentile ($12,137) tells you just how variable insurance pricing can be in this area — factors like flood zones, proximity to water, and individual insurer risk models can push premiums dramatically higher.

Compared to the Queensland state average of $4,547, this quote is about 44% cheaper. It also sits below the national average of $2,965 and very close to the national median of $2,716 — which is impressive given that coastal Queensland properties typically attract a loading compared to homes in lower-risk inland areas.

The sample size for Bongaree is 42 quotes, giving us a solid basis for comparison.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an insurance pricing perspective.

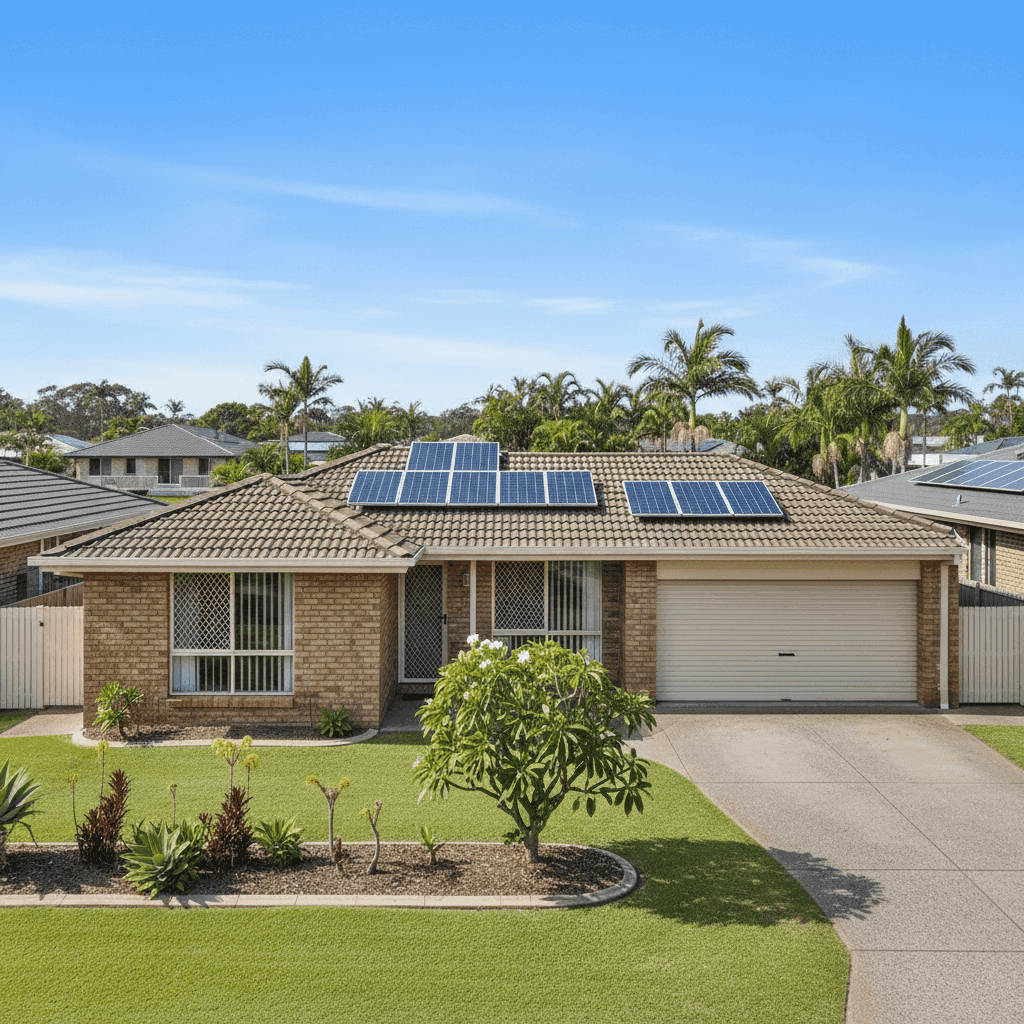

Brick veneer construction is generally viewed positively by insurers. While not as robust as full double brick, brick veneer walls offer good resistance to fire and moderate wind events, and they're far more insurer-friendly than timber weatherboard or fibre cement cladding — both common in older coastal Queensland homes.

Tiled roof is another tick in the right column. Concrete or terracotta tiles are durable and perform well in most weather conditions. They're less susceptible to hail damage than corrugated iron or Colorbond in many scenarios, and insurers typically regard them as a lower-risk roofing material.

Slab foundation is standard for homes of this era in Queensland and presents no particular risk flags. Similarly, tile flooring throughout is practical in a coastal climate and reduces the risk of water damage claims compared to timber or laminate floors.

The home was built in 1995, placing it in a relatively modern bracket. Homes from this period generally comply with building codes that introduced improved cyclone and storm-resistance standards — a relevant consideration for Queensland properties, even in areas not classified as cyclone risk zones.

Speaking of which: this property is not in a designated cyclone risk area, which removes one of the most significant premium drivers for Queensland coastal homes. That alone likely explains a meaningful portion of the savings compared to the suburb average.

Solar panels are present on this property. While solar adds some replacement value to the home, most modern home insurance policies cover rooftop solar as part of the building sum insured — so it's worth confirming your policy explicitly includes them. Ducted climate control is similarly worth checking, as this is a significant fixed asset that should be captured in your building sum insured.

The standard fittings quality designation keeps the rebuild cost estimate grounded. Homes with premium finishes — stone benchtops, custom cabinetry, imported tiles — cost more to rebuild and therefore attract higher premiums. A standard-fit home at 139 sqm is straightforward to price.

---

Tips for Homeowners in Bongaree

1. Review your building sum insured regularly At $395,000, the building sum insured needs to reflect the true cost of rebuilding your home from scratch — not its market value. Construction costs have risen significantly in recent years across Queensland. Use a building cost calculator or ask your insurer to review the figure annually to avoid being underinsured.

2. Confirm solar panels and ducted systems are covered Check your policy schedule to ensure rooftop solar panels and your ducted air conditioning system are explicitly included under the building definition. Some policies require these to be listed separately or have sub-limits that may not fully cover replacement costs.

3. Shop around — the spread in Bongaree is enormous With a 75th percentile of $12,137 and a 25th percentile of $3,489, the range of quotes in this suburb is extraordinary. Sticking with your current insurer at renewal without comparing alternatives could cost you thousands. Get a fresh quote at CoverClub to see where you stand.

4. Consider your contents sum insured carefully $50,000 in contents cover is a common starting point, but it's worth doing a room-by-room estimate of your belongings. Electronics, appliances, furniture, clothing, and tools can add up quickly. Underinsuring your contents is one of the most common mistakes homeowners make — and one of the most costly at claim time.

---

Compare Your Own Quote

Whether you own a similar home in Bongaree or elsewhere in Queensland, it pays to know what the market looks like. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly how your current premium stacks up. Start comparing at CoverClub and find out if you're getting a fair deal — or paying more than you should be.